If you intend to rely on mortgage borrowing for a part of the financing of your buy-to-let (BTL) property investment, a grasp of BTL mortgage lenders’ deposit requirements is crucial. This guide delves into the nuances of BTL mortgage-related deposits, exploring how much you need, the factors influencing these requirements, alternative financing options and planning for your investment journey.

08/04/2025By Pauzible Team · Editorial Team

If you intend to rely on mortgage borrowing for a part of the financing of your buy-to-let (BTL) property investment, a grasp of BTL mortgage lenders’ deposit requirements is crucial. This guide delves into the nuances of BTL mortgage-related deposits, exploring how much you need, the factors influencing these requirements, alternative financing options and planning for your investment journey.

Introduction to BTL Mortgage Deposits

The cornerstone of a successful BTL investment reliant in part on mortgage borrowing begins with understanding lenders’ deposit requirements. A deposit is an investor's own initial contribution towards the purchase price of a property, with the remainder of the purchase price being financed by a mortgage. In the domain of BTL investments, the deposit is not just a financial requirement, but also a reflection of your commitment and financial stability in the eyes of lenders.

Minimum Deposit Requirements

The minimum deposit required for BTL mortgages is typically 25% of the property's purchase price. However, this percentage is not fixed and it can vary based on factors such as the lender's policies and the borrower's financial situation. While a 25% deposit may be a good starting point for aspiring landlords to estimate as their likely initial investment (excluding stamp duty and purchase costs), they should be aware that lenders may ask for a higher deposit, perhaps even up to 40%, depending on affordability assessment. This is discussed further below.

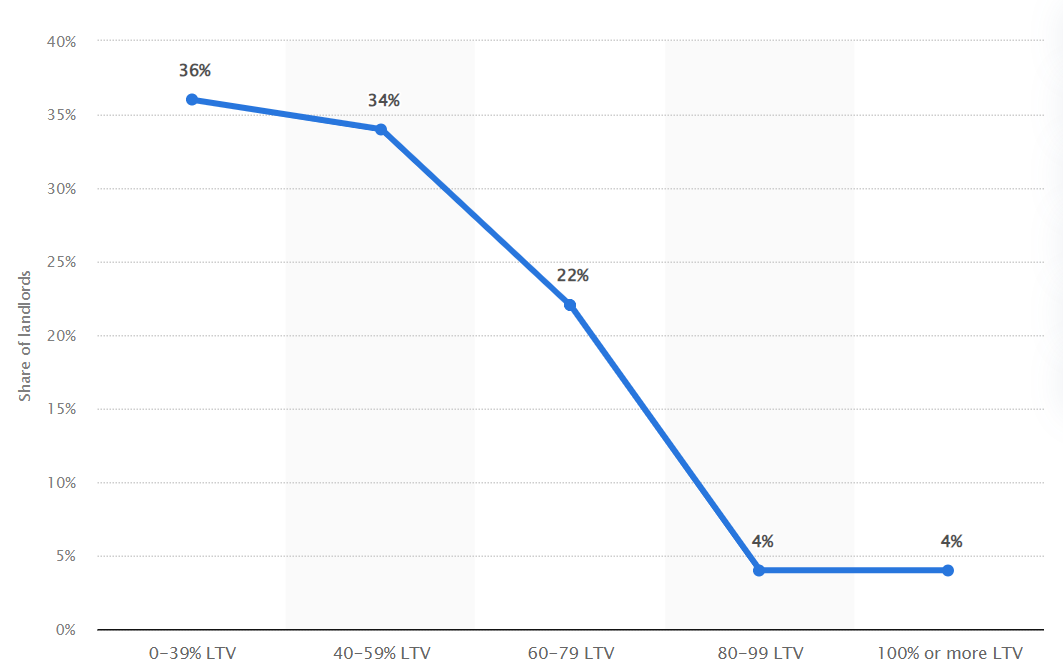

Distribution of buy-to-let landlords in the United Kingdom (UK) in 2nd Quarter 2023, by portfolio loan-to-value ratio

Source: Statista

Factors Influencing Deposit Requirements

When applying for a mortgage, as well as understanding other terms, such as the interest rate, it is helpful to understand the factors that can influence the deposit percentage. Knowing what lenders look for can improve your chances of securing a favourable mortgage deal. Here are some things to keep in mind in this connection:

- Affordability Assessment:Subject to a minimum deposit of about 25%, most lenders might want to see a larger deposit, depending on their affordability assessment of your particular case. For example, suppose the purchase price of your property is £300,000 and the annual rent you can realistically expect to receive from it is £18,000. Broadly, a potential lender might want to see that the annual amount of interest payments on your borrowing at a “stressed” interest rate does not exceed 80% of the annual rental income, or in this case £14,400 (80% of £18,000). Suppose further that the stressed annual interest rate is 8%, comprising the offered mortgage interest rate of 5% plus a stress factor of 3%. Annual interest payments of £14,400 at a stressed interest rate of 8% indicate a loan amount of £180,000. Thus, in this example, the lender might want to see a deposit of £120,000, i.e. the balance of the property purchase price of £300,000 over and above the £180,000 mortgage loan amount. The minimum deposit would thus be 40% of the property purchase price.

In addition, the lender will usually want to see that the borrower has a personal annual income of at least around £25,000 and a satisfactory credit report.

- Loan-to-Value (LTV) Ratio: The LTV ratio measures the outstanding mortgage balance as a percentage of the current market value of the property. While a lower LTV ratio means a higher deposit, it can also secure a more favourable mortgage interest rate. Usually, the cheapest interest rates are available on loans with an LTV ratio of 60% or less, i.e. where the deposit is 40% or more. In mid-2023, approximately 36 percent of UK landlords had an LTV ratio of below 39 percent, i.e. a deposit of 61% or more, while another 36 percent reported an LTV ratio of between 40 and 59 percent, i.e. a deposit of 41% to 60%. In other words, a substantial portion of landlords with mortgage debt held significant equity in their property.

- Investment Experience and Portfolio Size: If you have a proven track record as an investor with a diversified portfolio, you may be more likely to secure better mortgage terms. By highlighting your investment experience and portfolio size, you might be able to demonstrate to lenders that you are a low risk borrower and potentially secure a lower deposit requirement.

The BTL mortgage market is diverse and competitive, and deposit requirements can vary between lenders. While some may adhere to more demanding affordability assessments, subject to a minimum deposit of 25% deposit, others may offer more flexible terms based on the investor's financial health and the property's earning potential. Research and comparison are key in selecting a lender whose requirements and terms align with your own investment needs.

Alternative Financing Options

If you are an investor looking for alternative financing options, there are also several other routes you can explore:

- **Limited Company BTL Mortgages:** By structuring your investments through a limited company, you may be able to benefit from different deposit requirements, as well as the ability to deduct 100% of your mortgage interest costs for tax calculation purposes. However, the interest rate you pay may be slightly higher.

- **Specialist Lenders:** If you are facing unique or challenging financial situation, specialist lenders might be the solution you are looking for. These lenders may offer lower deposit options, albeit with higher interest rates, which reflect the increased risk involved.

Exploring alternative financing options can open new avenues for investors, particularly those facing hurdles with traditional lending criteria. From limited company structures to specialist lenders, the landscape offers a spectrum of possibilities, each with nuances in deposit requirements, interest rates and financial implications. Depending on your circumstances, these alternatives may warrant investigation, perhaps with an expert financial advisor, to optimise your financing requirements, including your deposit.

Planning Your Financial Journey

Embarking on a BTL investment is a journey that demands careful financial planning. Understanding the landscape of mortgage deposits, from minimum requirements to other factors influencing these requirements and the exploration of alternative financing options lay the groundwork for informed decision-making. By planning your finances carefully and exploring the options available, possibly with the help of a financial advisor, you can potentially position yourself to navigate the BTL financing market with insight and confidence.

FAQs:

Q. Can I buy a BTL property with a small deposit in the UK?

A: Typically, BTL mortgage lenders require a minimum deposit of 25% of the property's market price, unless their affordability assessment indicates a higher minimum deposit percentage. However, some specialist lenders may be able to offer mortgages with lower deposit requirements, albeit usually at higher interest rates to offset their increased risk.

Q. What happens if I don't have the minimum deposit for a BTL mortgage?

A: If you are unable to meet the minimum deposit requirement for a traditional BTL mortgage, there are several strategies you can explore:

- **Alternative Financing Options:** Look into mortgages offered by specialist lenders, who may have different criteria and accept lower deposits, but almost certainly at higher interest rates.

- **Raise Additional Capital:** Consider ways to increase your savings or secure additional funds by perhaps partnering with another investor.

- **Delay Your Investment Plans:** It might be worth postponing your investment until you can save a larger deposit.

Q. Can I use a gifted deposit for a BTL property?

A: Some lenders might accept gifted deposits for BTL properties, but they will require documentation verifying the gift's origin. The donor must also usually confirm in writing that the gift is non-repayable and that they will have no interest in the property. Lenders may also require proof of the donor's identity and their relationship to you to deal with money laundering concerns and requirements. Regardless of the deposit gift, the lender will still want to conduct an affordability assessment and borrower credit check, and expect the borrower to have a certain minimum level of personal annual income, usually around £25,000.

References:

1. Buy-To-Let Mortgage Deposits | online mortgage advisor | Updated on : 15 Mar 2024

The Pauzible Team consists of finance professionals and property market specialists dedicated to reinventing home ownership and BTL financing. With deep expertise across UK real estate and innovative financial products like Equity Partnership Agreements, we provide landlords and homeowners with the insights they need to unlock equity, navigate market volatility, and build sustainable wealth through property. Our mission is to make complex property finance simpler, quicker, and more accessible for everyone.

Ready to see what Pauzible could unlock?

Explore how accessing equity from your BTL property could support your business investment plans.

No obligation. Just a clear view of what might be possible.