Learn how to buy and sell a house at auction in the UK. Discover the auction process, costs, and tips for success in our comprehensive guide.

08/04/2025By Pauzible Team · Editorial Team

Buying a house at auction can be an exciting way to buy a property. It can also be a bit confusing and intimidating if you are new to the process. A property auction is a public sale in which the property is sold to the highest bidder. Auctions can be held in person, online or a combination of both. During the auction, potential buyers place bids on properties they are interested in. The auctioneer announces each property and invites buyers to place their bids. Bidders compete against one another by offering a higher price. Once the highest price is reached, the auctioneer will pound the gavel down, signifying the end of the auction.

Various types of properties can be sold at auction, including residential homes, commercial buildings and land. Properties at auction can range from well-maintained properties to those that require significant repairs. There can be various reasons a property is put up for auction. Sellers often choose auctions when they require a speedy transaction. This could be due to financial pressures or the need for a quick sale due to a job relocation. Houses that are hard to value due to unique features are also usually auctioned. This has nothing to do with financial or relocation reasons but is simply a strategic move to maximise the sale price. Auctioning is also the preferred method by banks and financial institutions for selling repossessed properties. It is also common with probate sales where estates need to be settled efficiently. The two main reasons sellers choose auctions are the need to sell quickly and have competitive bidding.

The Auction Process for Buyers

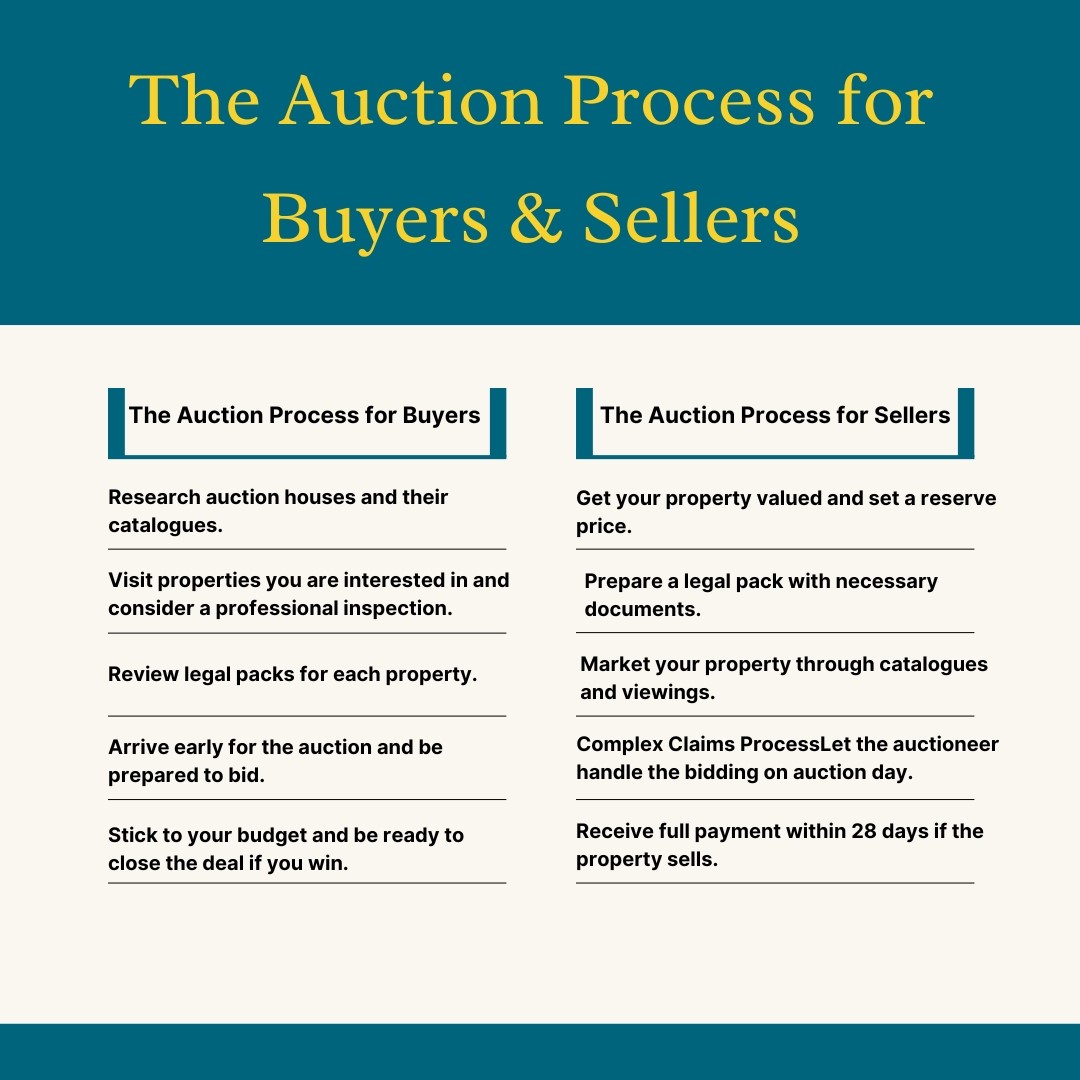

The first step in preparing for an auction is to explore auction houses and study their catalogues. The catalogues provide comprehensive lists of properties for sale. Visit the properties you are interested in and consider showing them to a builder or surveyor to ensure that there are no hidden issues. Don't forget to review a legal pack for each property you want. This pack contains crucial information such as the official copy of the register of title, lease and local authority search results.

On the day of the auction, it is all about being prepared and staying focused. Arrive early or log in early if it is an online auction. Pay close attention to the auctioneer's announcements and be ready to raise your hand or click the bid button when the property you are interested in comes up. Remember to stick to your budget and not get carried away. If you are the highest bidder, you will need to pay a 10% deposit immediately and sign a contract committing to the purchase. You will then have 28 days to pay the remaining 90% of the purchase price.

Buyer Costs at Auction

Buying a house at auction can be an appealing way to purchase a property because it can come at a lower price. However, buyers should also be aware of costs associated with this process. Educating yourself before buying a house at auction is important to avoid unnecessary surprises.

In addition to the obvious cost of the house, the buyer often has to pay an administrative fee to the auction house. These fees can vary but are typically a few hundred pounds. Always check the auction house’s terms to understand if there are any such administrative charges. Auction contracts often also include seller’s fees, basically a contribution to the seller’s legal costs and auction costs. There can also be legal fees when purchasing a property at auction. You should have legal assistance to review the legal pack, conduct searches and handle the transaction. Legal fees can range from £500 to £1,500 or more. It is advisable to engage a solicitor with experience in auction properties. It is also recommended that a survey be completed on an auctioned property. A survey can help identify any potential issues that might affect the property's value or if expensive repairs are required. Survey costs can range from c. £300 to £1,500 depending on the type of survey and size of property. Stamp Duty Land Tax is payable on all property purchases above a certain amount. The amount of stamp duty depends on the purchase price of the property and the applicable rates at the time of purchase. For residential properties, the rates can vary based on the price and whether you are a first-time buyer or a second-home buyer. Lastly, arranging building insurance immediately after winning the bid is crucial to protecting your investment.

The Auction Process for Sellers

For sellers, preparing the property for auction is the first step. Get your property valued and decide on a reserve price, which is the minimum amount you are willing to accept. Preparing a legal pack with all necessary documents is essential. This pack will be provided to potential buyers and should include the official copy of the register of title, lease, local authority search results and any other relevant information and documents.

Marketing the property properly is important. List it in an auction house catalogue which will be seen by potential buyers. Arrange viewings for interested buyers so that they can inspect the property before the auction. This can help generate more interest and potentially higher bids.

On the day of the auction, the auctioneer will manage the bidding process. You do not need to do anything during the auction itself. If the property sells, the buyer will pay a deposit and sign a contract. You will receive the full payment within 28 days, making the auction process a relatively quick way to sell a property.

Seller Costs at Auction

Auctioneer's fees are one of the most significant costs. These fees are a percentage of the final sale price of the property. The percentage can vary, but usually ranges from 1.5% to 3% plus VAT. Negotiating these fees with the auction house and understanding exactly what services are included is important. Most auction houses charge an entry fee to include your property in their auction catalogue. This fee can vary widely depending on the auction house and the marketing package you choose. Entry fees can range from a few hundred to a few thousand pounds. It covers the cost of listing your property in the auction catalogue, marketing materials and sometimes open house events. Additional marketing options might be available to enhance the visibility of your property. These include premium listings, professional photography, video tours and advertising. These additional marketing costs can range from £200 to £1,000 or more. Some auction houses charge an administration fee to cover the administrative costs associated with managing the sale. This fee can vary but is typically around £250 to £500 plus VAT. It is essential to confirm this fee with the auction house in advance. Preparing the legal pack for your property is essential for selling at auction. This pack includes all the necessary documents that potential buyers need to review before the auction. Legal fees for preparing this pack can range from £500 to £1,500. If you choose to have a survey done on your property to provide potential buyers with more information, this can add to your costs. Survey costs can range from £300 to £1,500. The last thing to consider is if your property does not sell because it did not meet the reserve price, you may still be liable for some of the auctioneer's fees, depending on the terms of your agreement. It is important to read and understand your agreement before committing to putting your house up for auction.

Buying at Auction with a Mortgage

Using a mortgage to buy a house at auction can be challenging due to the fast-paced nature of auctions. One of the main challenges is the speed of the process. Auctions require you to complete the purchase within 28 days, which is often too short for many mortgage lenders to complete their checks and processes. To mitigate this, you should arrange a mortgage in principle before the auction. This shows you are likely to get the loan, but it is not a guarantee. Ideally, you should also have a contingency financing plan, such as a bridge loan.

Another challenge is the condition of the property. Some auction properties may not be in good condition, making lenders hesitant to approve mortgages for homes that need a lot of work done to them. To overcome this, choose properties that are more likely to meet lender criteria and get a survey done beforehand to understand any potential issues.

The legal pack for auction properties must be thoroughly reviewed before bidding. Obtaining a mortgage can be difficult if there are any legal issues, including unclear title or disputes. Lenders need to be assured that the property has a clear and marketable title. Any complications in the legal documentation can cause delays or lead to the mortgage application being rejected.

Not all mortgage lenders are comfortable dealing with auction properties. Buyers may need to seek out specialized lenders who understand the auction process and are willing to work within the tight deadlines. These lenders might offer tailored mortgage products, but they often come with higher interest rates and fees, adding to the overall cost of purchasing the property.

Having a backup plan is also important. Ensure you have other funding options, such as bridging loans, in case your mortgage application takes too long.

Consequences of Failed Funding

Failing to secure funding for an auctioned property can have serious consequences. First, you will forfeit the 10% deposit paid on the auction day. Secondly, the seller may seek further compensation for any losses incurred due to the failed sale. This can include the difference in money if the property sells for a lower price at a subsequent auction. The seller might also ask for legal fees and re-marketing costs. Not completing your purchase may also harm your future reputation and credibility. Having your finances fully arranged before bidding is crucial to avoid these detrimental outcomes.

Conclusion

Buying a house at auction can be a great way to find a unique property or a good deal. It requires careful preparation and quick decision-making. If you plan to use a mortgage, make sure you are prepared for the challenges. By understanding the auction process and having your finances in order, you can navigate the auction successfully and secure your new home.

Selling your house at auction can be a quick way to sell, but it comes with various costs that need to be considered. The primary expenses are auctioneer's fees, entry fees, additional marketing costs, administration fees and legal fees. By understanding these costs and planning accordingly, you can decide whether selling at auction is the right choice for you. Always discuss the fees in detail with the auction house to ensure you clearly understand all the costs involved.

Q&A

Q. What are the main advantages of selling a house at auction?

A. Selling a house at auction offers several advantages. It provides a quick and efficient sales process, with the sale typically completed within 28 days of the auction. Auctions can create a competitive bidding environment, which can potentially drive up the sales price.

Q. How can I prepare financially to buy a house at auction?

A. Financial preparation is crucial when buying a house at auction. Ensure you have the 10% deposit readily available to pay immediately if you win the bid. Obtain a mortgage in principle to show you are likely to secure financing and have alternative funding options, such as bridging loans, in place. Review the legal pack and arrange for a survey to understand any potential additional costs for repairs or renovations.

Q. What should I look for in the legal pack before bidding on a property at auction?

A. The legal pack contains vital documents about the property, and you should review it carefully. Key elements to look for include title information, local authority searches for any planning or environmental issues, and any leases or tenancy agreements. Also, check for any restrictive covenants or easements that might affect the property. It is advisable to have a solicitor to review the legal pack on your behalf.

Q. What happens if the property does not sell at auction?

A. If a property does not sell at auction, it means it did not reach the reserve price set by the seller. In this case, the property may still be available for purchase through post-auction negotiations. Interested buyers can make offers directly to the auctioneer, who will relay them to the seller. The seller can then decide whether to accept an offer or re-list the property in a future auction.

Q. Can I use a mortgage to buy a house at auction and what are the challenges?

A. You can use a mortgage to buy a house at auction, but it comes with challenges. The main issue is the short completion timeframe of typically 28 days, which may not be enough for standard mortgage processing. Additionally, the property's condition must meet the lender's criteria, which can be difficult if the property needs significant repairs. To mitigate these challenges, get a mortgage in principle before the auction and have alternative financing options ready in case the mortgage process takes longer than expected. Be aware that failing to secure funding for an auctioned property can have serious consequences. You will forfeit the 10% deposit paid on auction day. The seller may also seek further compensation for any losses incurred due to the failed sale. This can include the difference in money if the property sells for a lower price at a subsequent auction, legal fees and re-marketing costs.

About the author

Pauzible Team

Editorial Team

The Pauzible Team consists of finance professionals and property market specialists dedicated to reinventing home ownership and BTL financing. With deep expertise across UK real estate and innovative financial products like Equity Partnership Agreements, we provide landlords and homeowners with the insights they need to unlock equity, navigate market volatility, and build sustainable wealth through property. Our mission is to make complex property finance simpler, quicker, and more accessible for everyone.

Ready to see what Pauzible could unlock?

Explore how accessing equity from your BTL property could support your business investment plans.

No obligation. Just a clear view of what might be possible.