How do Life Insurance and Critical Illness cover differ?

Discover the key differences between life insurance and critical illness cover, including benefits, coverage, and why you may need both for comprehensive security.

08/04/2025By Pauzible Team · Editorial Team

What Is Life Insurance?

Life insurance is a contract between yourself and an insurer where, in exchange for regular insurance premia, the insurer pays a lump sum to your beneficiaries upon your death. Such cover is usually taken out to ensure essential financial support for your family after you die. They might need it for them to be able to meet everyday living expenses, or large commitments such as a mortgage repayment or payment of school fees.

Types of Life Insurance

There are two main types of life insurance policy:

Term Life Insurance: This type of life policy covers you for a specified period, usually until you reach the age of 70 or 75, although you may prefer to choose a shorter term than that. If you pass away within the term specified under the policy, the insurer will pay out the amount of cover to your beneficiaries. If you survive the term, the policy ends and no payment will be made upon your death.

Whole of Life Insurance: This type of policy covers you for the whole of your life, as the name suggests. The insurer will pay out the amount of cover to your beneficiaries when you die.

What Is Critical Illness Cover?

Critical illness cover is a policy that pays out the amount of cover you took out insurance for if you are diagnosed with a critical illness during the term of the policy. You do not necessarily need to be diagnosed as being terminally ill. Critical illness cover does not pay out upon death, as it is not life insurance.

How Does Critical Illness Cover Work?

Critical illness cover can be taken out as a standalone policy or as a combined policy with life insurance. It pays out the amount of cover if you are diagnosed with a critical illness. It typically protects you against a range of critical medical conditions. While coverage can vary between policies, common conditions covered include:

Cancer

Heart attack

Stroke

Multiple sclerosis

Organ failure

Alzheimer’s disease

Parkinson’s disease

It is important to note that policies can be particular about which conditions are covered and under what circumstances they will pay out. Always read the policy terms carefully to understand the exact coverage before choosing the policy and provider.

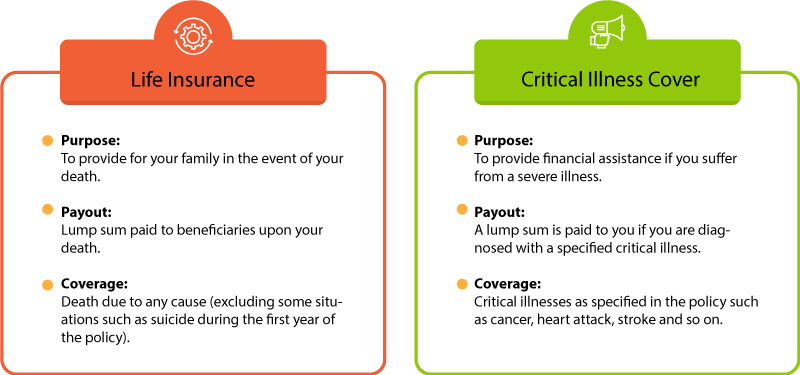

Life Insurance vs Critical Illness Cover

While both life insurance and critical illness cover are essential tools for financial planning, they are different in terms of coverage, purpose and payout conditions. Here, briefly, is how they compare:

Life Insurance

Critical Illness Cover

Purpose: To provide for your family in the event of your death.

Purpose: To provide financial assistance if you suffer from a severe illness.

Payout: Lump sum paid to beneficiaries upon your death.

Payout: A lump sum is paid to you if you are diagnosed with a specified critical illness.

Coverage: Death due to any cause (excluding some situations such as suicide during the first year of the policy).

Coverage: Critical illnesses as specified in the policy, such as cancer, heart attack, stroke and so on.

The Benefits of Combining Life Insurance and Critical Illness Cover

Life and critical illness cover can be combined into one policy for those looking to maximize protection. Known as life insurance with critical illness cover, this type of policy covers both death and diagnosis of critical illness.

Why Consider Combined Cover?

Comprehensive Protection: You are covered for both death and critical illness, ensuring you and your family receive financial support in either situation.

Convenience: Managing a single policy is more straightforward than juggling multiple insurance policies.

Cost-efficiency: Combined cover can be cheaper than purchasing two separate policies.

Drawbacks of Combined Cover

A potential downside is that, if you claim for a critical illness under a combined policy, the policy pay out upon death, if it occurs during the policy term, may be reduced. Having separate stand alone policies can avoid this problem.

Choosing the right type of policy

Choosing the right type of insurance policy depends on your particular circumstances, including your personal financial situation and family needs. Here are a few factors to consider:

Financial Dependents: Life insurance might be worth considering if you have a partner and children who rely on your income, and a substantial mortgage still needs to be paid off.

Health Risk: If you are at a higher risk of serious illness due to your family history, critical illness cover may provide additional peace of mind.

Budget: If cost is a concern, depending on your circumstances, you might, for example, wish to start with life insurance first and perhaps consider taking on critical illness cover at a later stage if you can afford it then.

Existing Benefits: Some employers provide life insurance and critical illness cover as part of their benefits package. Check what is available through your employer before buying further policies privately.

Conclusion: Do You Need Life Insurance, Critical Illness Cover or Both?

Ultimately, the decision between life insurance and critical illness cover, or having both, hinges on your personal financial circumstances and goals. Life insurance is important for anyone with dependents who would face financial hardship if they were no longer around, while critical illness cover offers a safety net if a serious illness disrupts your ability to work and earn. For many, taking on both policies provides a comprehensive safety net, ensuring peace of mind against life’s uncertainties. Regardless of your choice, having some form of protection in place can make a world of difference when life takes an unexpected turn. If you are unsure about the best option for your situation, consulting a financial advisor can help tailor a solution that meets your needs and budget.

FAQs:

Q. What is life insurance and how does it work?

A. Life insurance is a contract between yourself and an insurer where, in exchange for regular insurance premia, the insurer pays a lump sum to your beneficiaries upon your death. Such cover is usually taken out to ensure essential financial support for your family after you die. They might need it for them to be able to meet everyday living expenses, or large commitments such as a mortgage repayment or payment of school fees.

Q. What are the main types of life insurance available?

A. The two main types of life insurance are:

Term Life Insurance: This type of life policy covers you for a specified period, usually until you reach the age of 70 or 75, although you may prefer to choose a shorter term than that. If you pass away within the term specified under the policy, the insurer will pay out the amount of cover to your beneficiaries. If you survive the term, the policy ends and no payment will be made upon your death.

Whole of Life Insurance: This type of policy covers you for the whole of your life, as the name suggests. The insurer will pay out the amount of cover to your beneficiaries when you die.

Q. What does life insurance typically cover?

A. Life insurance covers death, providing a payout to your beneficiaries. This money can be used to cover costs such as mortgage payments, household bills, school fees and other expenses.

Q. What is critical illness cover and how does it differ from life insurance?

A. Critical illness cover is a policy that pays a lump sum if you are diagnosed with an illness such as cancer or a heart attack. While life insurance pays out upon death, critical illness cover pays while you are still alive to help cover medical expenses, mortgage payments or supplement lost income.

Q. Can life insurance and critical illness cover be combined?

A. Life insurance and critical illness cover can be combined into one policy. This ensures you are covered for both death and serious illness, providing comprehensive financial protection for your family and yourself in the event of death or critical illness. However, some policies may reduce payout on death if you have already claimed for critical illness, so it is important to consider the terms carefully. You might be able to avoid this problem by taking out two separate stand alone policies.

About the author

Pauzible Team

Editorial Team

The Pauzible Team consists of finance professionals and property market specialists dedicated to reinventing home ownership and BTL financing. With deep expertise across UK real estate and innovative financial products like Equity Partnership Agreements, we provide landlords and homeowners with the insights they need to unlock equity, navigate market volatility, and build sustainable wealth through property. Our mission is to make complex property finance simpler, quicker, and more accessible for everyone.

Ready to see what Pauzible could unlock?

Explore how accessing equity from your BTL property could support your business investment plans.

No obligation. Just a clear view of what might be possible.