Rising inflation can have a powerful impact on the housing market, leaving a mark on mortgage interest rates, and on the financial wellbeing of homeowners and prospective buyers alike.

08/04/2025By Pauzible Team · Editorial Team

Introduction

Rising inflation can have a powerful impact on the housing market, leaving a mark on mortgage interest rates, and on the financial wellbeing of homeowners and prospective buyers alike.

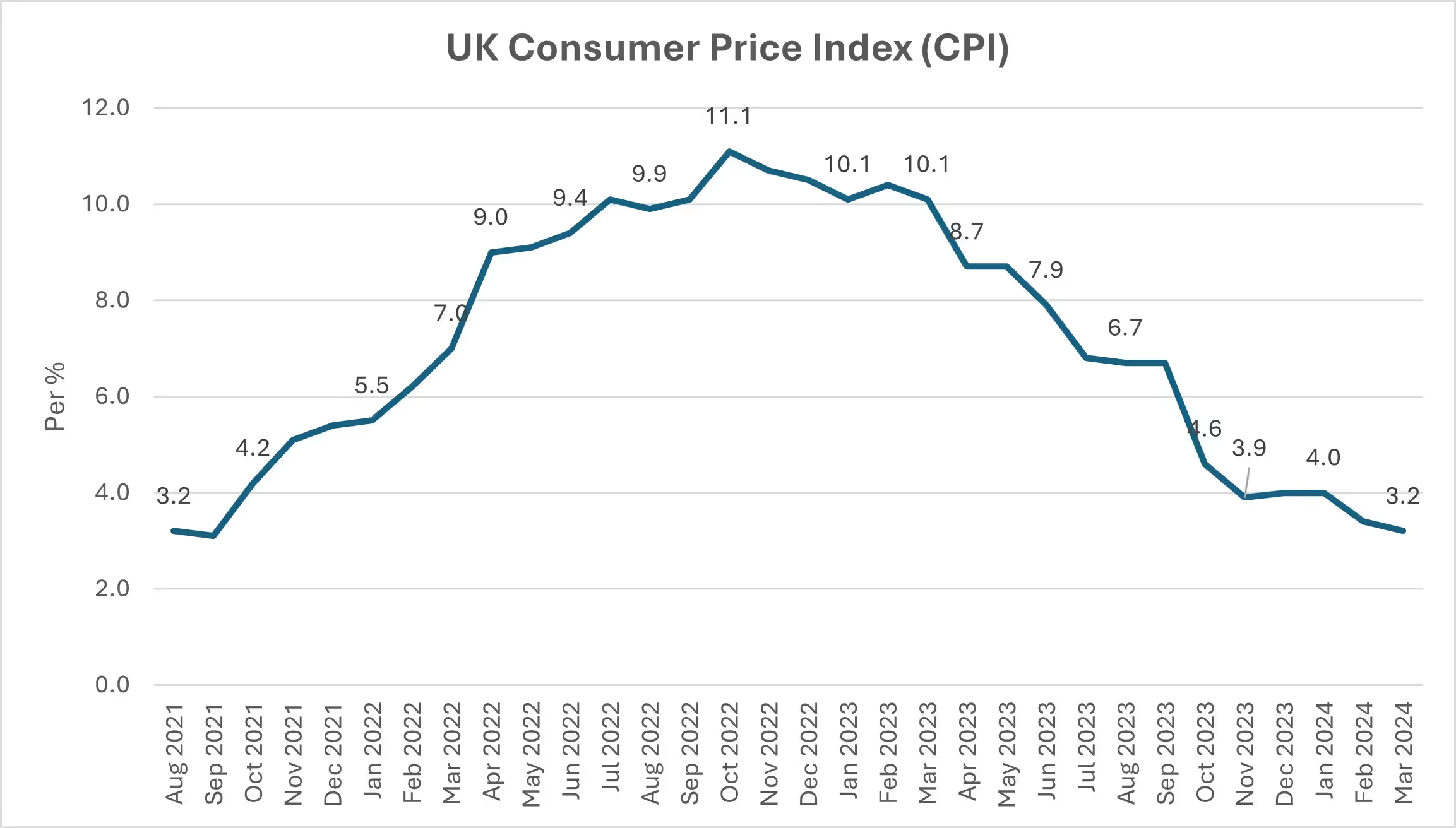

For example, the Consumer Price Index (CPI) annual rate has witnessed a notable rise every month since August 2021:

Source¹ : ONS

In response, the Bank of England has increased its base rate 14 times since December 2021 in order to try and bring the inflation rate down to its target level of 2%:

BOE Official Bank Rate:

Year

Date

Month

New rate %

2021

16

Dec

0.2500

2022

3

Feb

0.5000

2022

17

Mar

0.7500

2022

5

May

1.0000

2022

16

Jun

1.2500

2022

4

Aug

1.7500

2022

22

Sep

2.2500

2022

3

Nov

3.0000

2022

15

Dec

3.5000

2023

2

Feb

4.0000

2023

23

Mar

4.2500

2023

11

May

4.5000

2023

22

Jun

5.0000

2023

3

Aug

5.2500

Source² : BOE

This upward trajectory in the base rate serves as a stark reminder of the relationship between inflation and the Bank of England base rate. The base rate, in turn, has an impact on mortgage rates.

Understanding the Link

The connection between inflation and the Bank of England's base rate decisions is deeply rooted in historical precedent. A retrospective glance at the 1970s, a period marked by rising inflation, reveals the decisive actions taken by the Bank, substantial hikes in the base rate, reaching an unprecedented peak of 17% by the end of 1979. These bold moves responded directly to rising inflation, eventually curbing its advance and restoring greater economic stability. However, the interest rate hikes raised mortgage rates and dramatically increased the cost of borrowing for homeowners.

Impact on Mortgage Payments

The consequences of rising inflation and interest rates are felt most acutely in tracker rate and standard variable rate mortgages, where the link to the Bank of England’s base rate is direct and immediate. Historical records from the tumultuous 1970s offer a sobering illustration of how inflation can precipitate mortgage rate hikes, with new borrowers in 1979 facing an average mortgage rate of 12.38%, a substantial increase from preceding years. This stark reality underscores the financial strain that homeowners have to endure during periods of escalating inflation as their monthly mortgage payments swell, potentially straining household budgets to breaking point. Fast forward to recent times when the CPI annual rate has risen above the Bank of England’s target inflation rate of 2% every month since August 2021, including in the range of 9% - 11.1% during the April 2022 – March 2023 period. In response, the Bank of England has raised its base rate from 0.25% in December 2021 to 5.25% in August 2023.

Strategies for Protection

Amidst the turbulence of rising inflation and interest rates, those who chose relatively low 2-year or, especially, 5-year fixed mortgage rates before the base rate started to rise gained a measure of protection. However, this was only for a limited period; as these fixed rate periods came to an end, the new rates borrowers had to choose, whether fixed or tracker, were inevitably much higher.

The Bank of England sheds light on another prudent strategy adopted by households during previous periods of inflation and high interest rates, such as the 1970s: a trend towards excess mortgage repayments or overpayments. By prioritizing the reduction of their outstanding mortgage balance, homeowners mitigated the longer term impact of interest rate hikes and bolstered their financial resilience in the face of economic uncertainty. However, many households do not have the level of income and savings necessary to be able to make overpayments sufficient to make a significant dent in their outstanding mortgage balances.

Another strategy for short term protection is government help. For example, depending on their circumstances, Support for Mortgage Interest (SMI) loans can help eligible homeowners with mortgage interest payments on their outstanding mortgage balances of up to a maximum of £200,000. SMI loans cannot be applied to mortgage interest arrears. To be eligible for SMI loans, homeowners must qualify for a benefit such as Income Support, income-based Jobseeker’s Allowance, income-related Employment and Support Allowance, Universal Credit or Pension Credit. SMI loans are repayable with interest when the property is sold or transferred.

House price increases and mortgage affordability

Average house price increases in the UK, especially in certain areas such as London and the South East, have for decades outstripped increases in average incomes. This means that the size of deposits and mortgages required for new home purchases has increased significantly and disproportionately compared to income, over time. Thus, house price inflation also has an impact on mortgage size and mortgage repayments. This situation is exacerbated further when the Bank of England raises interest rates to combat inflation, which leads to a rise in mortgage rates.

Seeking Professional Advice

The complexities inherent in the mortgage market due to an ever changing economic landscape can make professional financial advice invaluable. By consulting financial advisors who are well versed in the nuances of mortgage products, interest rates and the broader economic climate, homeowners can understand their options better and make informed decisions aligned with their longer term financial objectives.

Conclusion

Inflation can be a pervasive force that ripples through the fabric of the economy, leaving an indelible mark on mortgage rates and the housing market. By staying informed and seeking expert advice, homeowners can navigate these economic currents with greater assurance and strategic insight. As history has repeatedly demonstrated, understanding and planning are keys to weathering financial fluctuations and safeguarding one’s investment in the property market.

FAQs:

Q. How does inflation affect mortgage interest rates?

A: A persistent rise in inflation above its target inflation rate of 2% prompts the Bank of England to raise its base rate. This change directly impacts tracker rate and standard variable rate mortgages, where interest rates are aligned with the base rate. Consequently, as the base rate rises, so do the interest rates on these mortgages. Base rate rises also feed through to the new 2-year or 5-year fixed rates that mortgage lenders are willing to offer.

Q. What impact will rising inflation have on my existing mortgage payments?

A: Rising inflation can lead to higher interest rates for mortgages with tracker rates and standard variable rates, thus increasing monthly payments. If you have a relatively low fixed-rate mortgage, your payments will remain unchanged during the term of that fixed rate, regardless of inflation and interest rate changes. However, you will be impacted when your fixed rate period ends and you have to choose a new rate, whether fixed or tracker.

Q. How can I protect myself from the effects of inflation on my mortgage?

A: One way is by securing a fixed-rate mortgage while rates are low. This locks in your low mortgage rate for a set period, shielding you from an immediate rate increases flowing from the Bank of England’s response to inflation. Budgeting conservatively and setting aside savings can also provide a buffer against financial strains ultimately caused by inflation. Overpayments, to the extent possible, can also help weather the storm.

Q. Are there any government schemes or programs to help with rising mortgage costs?

A: Yes, the government occasionally introduces schemes to help homeowners struggling with mortgage interest payments. For instance, the Support for Mortgage Interest (SMI) loan scheme helps eligible homeowners pay interest on their mortgage up to a certain level. Keeping informed about such schemes can provide some welcome and necessary relief during difficult times.

The Pauzible Team consists of finance professionals and property market specialists dedicated to reinventing home ownership and BTL financing. With deep expertise across UK real estate and innovative financial products like Equity Partnership Agreements, we provide landlords and homeowners with the insights they need to unlock equity, navigate market volatility, and build sustainable wealth through property. Our mission is to make complex property finance simpler, quicker, and more accessible for everyone.

Ready to see what Pauzible could unlock?

Explore how accessing equity from your BTL property could support your business investment plans.

No obligation. Just a clear view of what might be possible.