Interest Only Mortgages in the UK Market: Benefits & Risks

What is an interest only-mortgage? Interest-only mortgages are a type of mortgage where the initial loan amount (or principal) remains the same over the entire mortgage term. It is typically repaid through the sale of the mortgaged property or other forms of repayment strategy, including remortgaging or drawing upon savings and other investments.

08/04/2025By Pauzible Team · Editorial Team

Explore the nuances of interest-only mortgages in the UK. Compare rates, weigh buy-to-let options, and make informed choices for your financial future.

What is an interest only-mortgage? Interest-only mortgages are a type of mortgage where the initial loan amount (or principal) remains the same over the entire mortgage term. It is typically repaid through the sale of the mortgaged property or other forms of repayment strategy, including remortgaging or drawing upon savings and other investments.

Choosing an Interest-Only Mortgage

When considering an interest-only mortgage, it is essential to consider your long-term financial stability, including your ability to manage surges in mortgage interest rates and the eventual lump sum principal repayment, and your plans for the property.

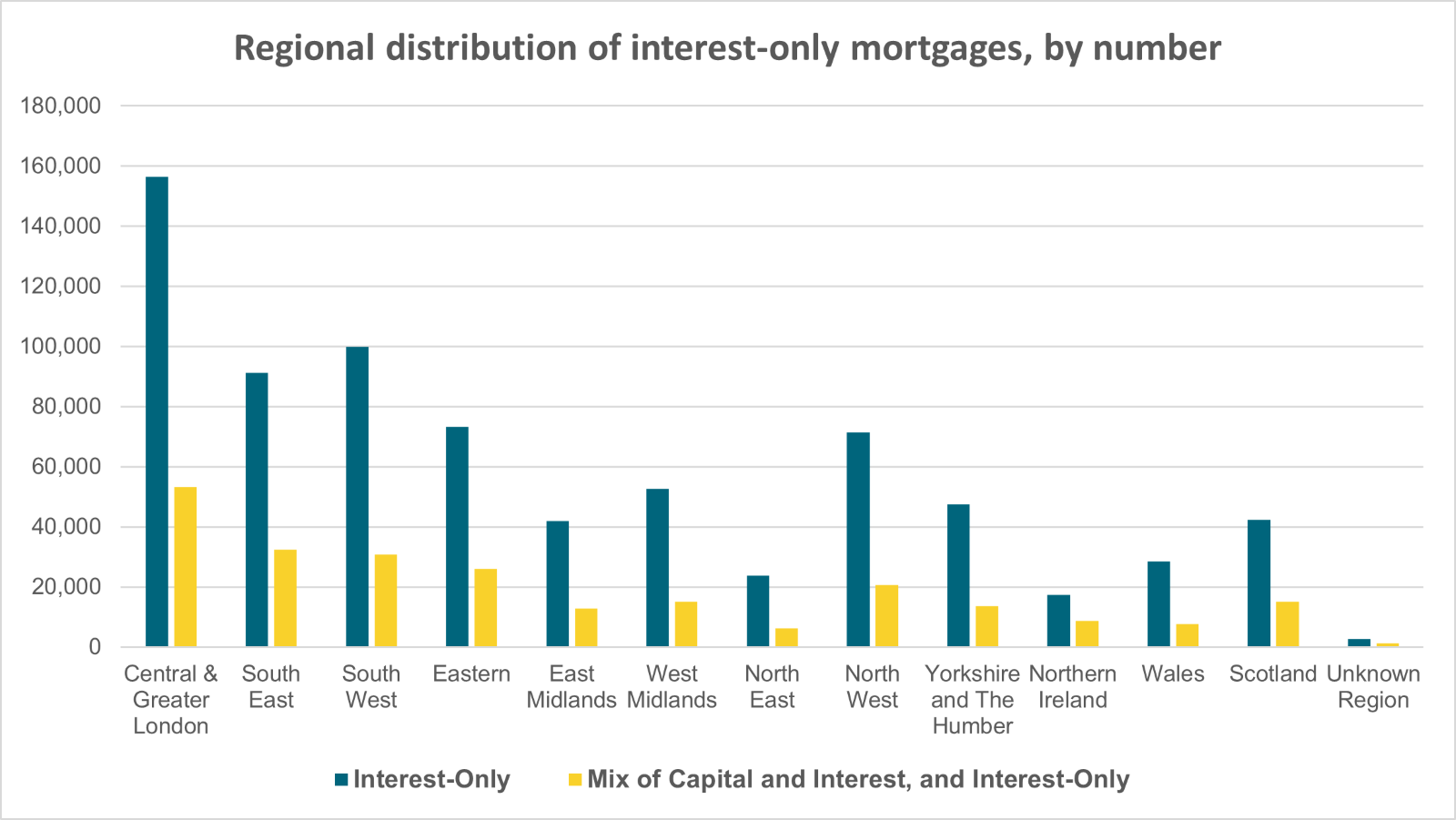

Source¹ : FCA

Benefits of Interest-Only Mortgages

Lower Monthly Payments: One of the main advantages of an interest only mortgage is that the monthly payments are lower than traditional repayment mortgages. This is because you only pay interest on a monthly basis. The principal amount is not repaid in monthly instalments, but rather as an eventual lump sum repayment. This can be especially helpful for those with limited monthly disposable income.

Flexibility: Interest only mortgages offer flexibility, making it beneficial for people with variable income. Individuals have the option of being able to make some principal repayments when they can afford to. This means that if you have a variable income, you can take advantage of the flexibility of an interest-only mortgage.

Investment Potential: Another advantage of interest-only mortgages is that some borrowers may invest the money saved from lower monthly payments in other assets. By investing the money saved from lower costs, borrowers can diversify investments, some of which can be used to pay off the mortgage principal eventually.

Property Appreciation: Those with interest-only mortgages can benefit from an increase in the property's value over time while maintaining lower monthly payments. As the property's value increases, the value of the homeowners’ home equity also increases, which can benefit the borrower in the long term.

Tax Advantages for BTL Investors: About 20% of interest payments on buy-to-let (BTL) properties can be offset against rental income for tax purposes, providing some tax advantages for BTL investors. This means BTL investors with interest-only mortgages can offset some of their interest payments against the rental income they receive, reducing their tax liability.

Risks and Drawbacks

Repayment of Principal: Due to the nature of the interest-only mortgage, the principal amount remains the same throughout the term, requiring a significant repayment at the end. This means that at the end of the mortgage term, you will still owe the loan amount, which can be a financial burden.

Investment Risk: If you use investments to repay the loan, you must have a solid investment strategy. However, there's always a risk that your assets may need to grow more to cover the cost of the loan. This could leave you with a shortfall.

Property Value Fluctuation: There's a risk that the value of your property may decline over time. If this happens, you may owe more on the loan than the property is worth. This is known as “negative equity” and can be a significant financial burden.

Interest Rate Fluctuation: If interest rates rise sharply, the monthly cost of an interest-rate mortgage also rises sharply; there is no cushion from a steadily falling outstanding principal mortgage balance that is a feature of a repayment mortgage. Where interest costs exceed rental income, the property owner will need to fund negative cashflow from other sources or even consider selling the property.

Eligibility Criteria: If you are considering an interest only mortgage, it is essential to understand that lenders have stringent eligibility criteria. You will need to have a solid repayment plan in place, which may include investments or other assets that can be used to pay off the loan, and the ability to withstand significant increases in interest rates. This can limit access to some borrowers.

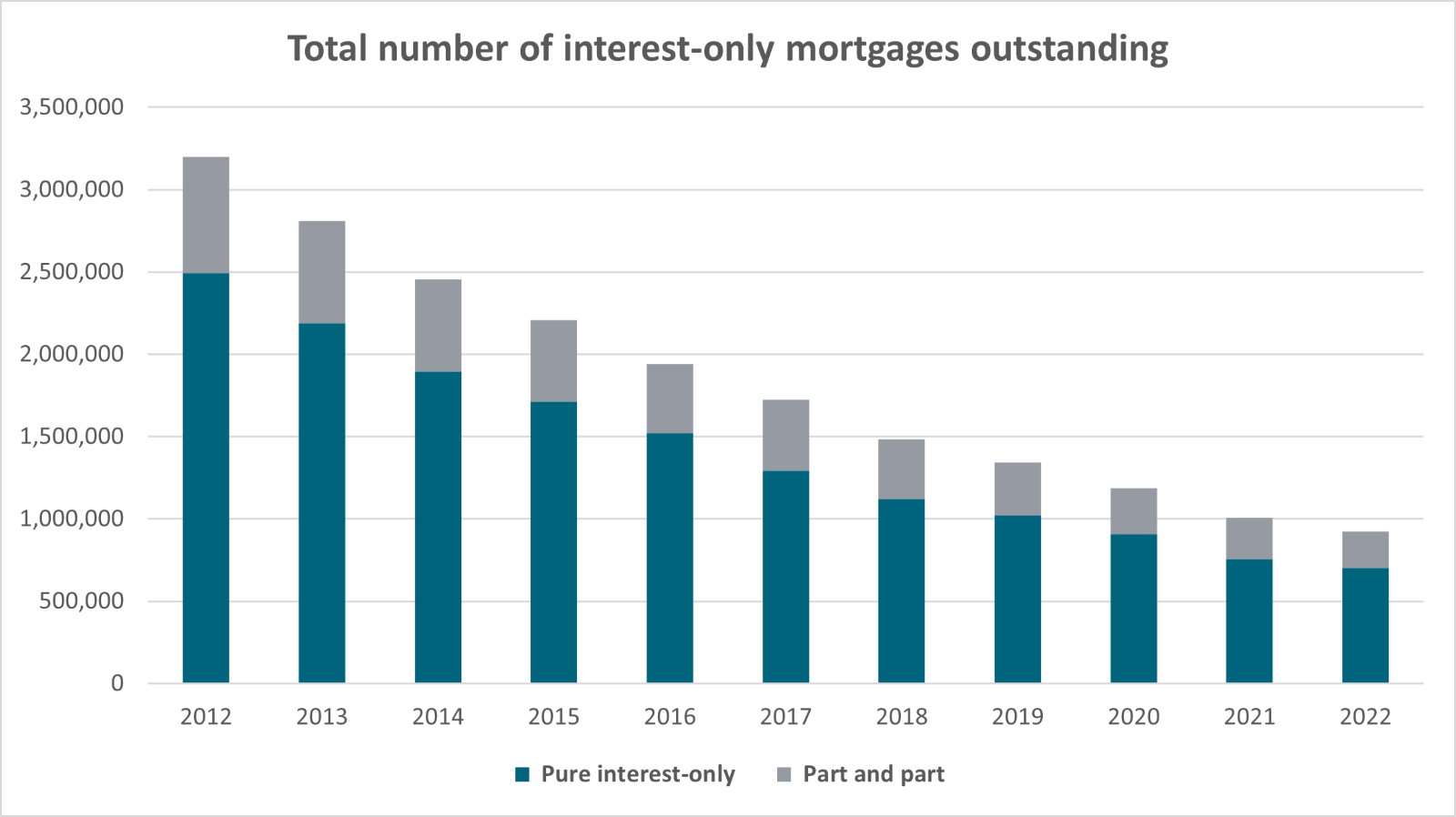

Total number of interest-only mortgages outstanding

Year

Pure interest-only

Part and part

2012

2,494,000

705,000

2013

2,188,000

623,000

2014

1,895,000

559,000

2015

1,711,000

498,000

2016

1,520,000

420,000

2017

1,293,000

429,000

2018

1,123,000

360,000

2019

1,023,000

318,000

2020

908,000

277,000

2021

754,000

252,000

2022

702,000

222,000

Source: UK Finance²

Source: UK Finance²

Helpful Insights in Constructing a Repayment Plan

Savings and Investments: Regular contributions to savings or investment vehicles can effectively accumulate the necessary funds. Consider ISAs, stocks, bonds or other investments.

Property Sale Plan: If the plan is to sell the property, keep abreast of market conditions and clearly understand when it would be best to sell.

Alternate Property Equity: If you own multiple properties, consider how equity from one can help repay the interest-only mortgage on another.

Regular Reviews: Conduct regular reviews of your repayment plan to ensure it's on track. Adjust your strategy according to changes in financial circumstances or market conditions.

Contingency Measures: Have contingency plans, such as downsizing or extending the mortgage term, if the original plan becomes unfeasible.

How to Qualify for Interest-Only Mortgages

When obtaining a loan, eligibility criteria can vary depending on the lender. However, in general, lenders will typically scrutinize an applicant's financial stability and require a substantial deposit, strong income and a credible plan to repay the principal at term-end. This means the lender will want to see that you have a solid financial foundation to manage interest rate increases and can repay the loan in full.

Buy-to-Let Considerations

Tax Efficiency: About 20% of interest payments on BTL mortgages can often be offset against rental income for tax purposes.

Market Dynamics: Understanding rental market dynamics is crucial. Strong rental demand and yields can make an interest-only BTL mortgage more viable.

Capital Appreciation: BTL investors often rely on property value appreciation to repay the mortgage at the end of the term. However, this requires careful market analysis and a backup plan if property values stagnate or fall.

Interest-only mortgages offer both potential benefits and risks. They require careful consideration, a clear repayment strategy, and an understanding of the long-term financial implications.

The Pauzible Insights article Financial Pressures on Buy-to-Let Landlords (UK BTL Crisis : Rising Rates Crushing Landlords ) provides detailed scenario analyses of a BTL investment with an interest-only mortgage.

FAQs:

Q: What If You Can't Pay the Final Principal Repayment Amount?

A: Failing to repay can lead to property repossession. It's crucial to have a solid repayment strategy and consider options like downsizing or remortgaging.

Q: Who Typically Chooses Interest-Only Mortgages?

A: These mortgages often appeal to high earners or those with significant assets who can manage the final principal repayment. They're also popular among buy-to-let investors.

Q: What is an interest-only mortgage?

A: An interest-only mortgage differs from a traditional mortgage in how you repay the loan. With an interest-only mortgage, you only pay the interest accrued on the borrowed amount each month. The principal loan amount itself remains unchanged until the end of the mortgage term. You'll then need a separate plan to repay the entire principal sum, such as selling the property, remortgaging, or using savings.

Q: Which is better, interest-only or repayment?

A: It depends on your individual circumstances and goals. If you need lower monthly payments but have a clear plan for the final lump sum, interest-only can be an option. Repayment offers long-term stability and lower overall costs but requires higher monthly payments.

Q: Can I use an interest-only mortgage for a buy-to-let property?

A: Yes, some lenders offer interest-only mortgages for buy-to-let properties. This can be attractive for maximizing rental income, but remember the risks of rising interest rates or property value dips impacting your repayment ability.

Q: Are there tax benefits for buy-to-let interest-only mortgages?

A: In the UK, you can often offset up to 20% of interest payments on buy-to-let mortgages against your rental income for tax purposes. However, tax regulations can change, so consult a financial advisor for current information.

Q: What are the current interest-only mortgage rates in the UK?

A: Rates vary depending on your loan amount, credit score, and other factors. Generally, expect interest-only rates to be slightly higher than repayment rates. Use online comparison tools to find current deals from different lenders.

Q: Do I need a large deposit for an interest-only mortgage?

A: Yes, lenders typically require a higher deposit for interest-only mortgages due to the increased risk. Expect deposit requirements to be at least 20%-25% of the loan amount.

The Pauzible Team consists of finance professionals and property market specialists dedicated to reinventing home ownership and BTL financing. With deep expertise across UK real estate and innovative financial products like Equity Partnership Agreements, we provide landlords and homeowners with the insights they need to unlock equity, navigate market volatility, and build sustainable wealth through property. Our mission is to make complex property finance simpler, quicker, and more accessible for everyone.

Ready to see what Pauzible could unlock?

Explore how accessing equity from your BTL property could support your business investment plans.

No obligation. Just a clear view of what might be possible.