Leveraging Home Equity: Borrowing Options Explained

Building equity in your home is a gradual process that occurs as you pay down your mortgage and your property's value increases over time. Essentially, home equity is the difference between the current value of your home and any outstanding mortgage debt. The equity you build up can be utilized in various ways to help you achieve your financial goals.

08/04/2025By Pauzible Team · Editorial Team

Building equity in your home is a gradual process that occurs as you pay down your mortgage and your property's value increases over time. Essentially, home equity is the difference between the current value of your home and any outstanding mortgage debt. The equity you build up can be utilized in various ways to help you achieve your financial goals.

- One option is to remortgage, which involves replacing your current mortgage with a new one, often at better interest rates or with different loan terms.

- Another option is to take out a second-charge mortgage or home equity loan, which gives you access to a lump sum of cash secured against the equity you've built in your home.

- Finally, additional borrowing or advances on your current mortgage can also provide you with extra funds from your original lender.

Key Types of Secured Loans in the UK

In the UK, secured loans that use home equity as collateral can be divided into three main categories: Second-hand mortgages, Home equity loans, and Further advances.

Second-charge mortgages are entirely separate loans that are provided by another lender in addition to your primary mortgage. These loans are typically used by homeowners who want to borrow additional funds without having to remortgage their property. Unlike remortgaging, second-charge mortgages allow borrowers to keep their existing mortgage in place while taking on additional debt.

On the other hand, home equity loans are additional borrowings arranged through the borrower's first mortgage lender and secured against their property. These loans are also known as 'second mortgages' and allow borrowers to access a lump sum of money that they can use for any purpose they choose.

Further advances are offered by the borrower's existing lender, which provides additional funds on top of their current mortgage balance. These loans are typically more accessible than second-charge mortgages or home equity loans if the borrower is eligible. However, the amount of money that can be borrowed may be limited, and the interest rate may be slightly higher.

Overall, second charges and home equity loans allow borrowers to get more significant loan amounts, while further advances are more accessible to obtain if eligible with your current lender. It's important to carefully consider the pros and cons of each option before deciding which type of home equity loan is right for you.

Eligibility Criteria for Secured Loan Borrowing

When you apply for a loan, lenders evaluate multiple criteria to determine your eligibility. These criteria include your home equity, credit history, employment status, income, age, and residency. Let's take a closer look at each factor.

Firstly, the lender will assess the equity in your home. Most lenders require at least 15-20% equity remaining in your home after you borrow the loan. This equity acts as collateral, ensuring that the lender has a secure investment.

Secondly, your credit history and score are crucial factors in determining your loan eligibility. Your credit history shows your reliability in managing debts, and a good credit score demonstrates your ability to make timely repayments. A high credit score increases the likelihood of loan approval and may lead to more favourable interest rates.

Thirdly, your employment status and income are evaluated. Steady employment and income assure the lender that you can meet the repayment obligations. The lender may also assess the stability of your job or business to ensure that your income remains consistent.

Fourthly, lenders commonly mandate age and residency requirements. You must be 18 years old and a UK resident for 1-3 years to be eligible for most loans. These requirements ensure that you are legally capable of entering into a loan agreement and have a stable residency in the UK.

By meeting these conditions, you provide the best loan approval chance and may qualify for competitive interest rates.

Comparing Key Features: Remortgaging vs Second Mortgages

Feature

Remortgaging

Second Mortgage

Purpose

Replace existing mortgage

Extra borrowing, in addition to the primary mortgage

Lender(s)

Typically one new lender

Original lender plus a second lender

Eligibility

Based on property value and income

Contingent on sufficient leftover home equity

Costs

Possible early repayment charges from old lender

Arrangement fees for new second charge loan

Interest Rates and Fees for Secured Loan Products

Second-charge and home equity loans typically have higher interest rates than main mortgages but lower than personal loans. Depending on product features and personal factors, ranges range from 4-10% APR. Arrangement fees are standard, along with early repayment charges in some cases.

How to Borrow Responsibly Using Home Equity

While home equity borrowing provides convenient access to funds, it carries risks like foreclosure if overextended financially. Tips for responsible lending include:

Borrow only what you can comfortably afford to repay

Build in a buffer for potential rate rises on adjustable-rate products

Set up automatic payments to avoid late fees

Compare loan costs across multiple providers

Keep sufficient equity to absorb potential property value decreases

Consulting a financial advisor can guide prudent strategies aligned to your situation.

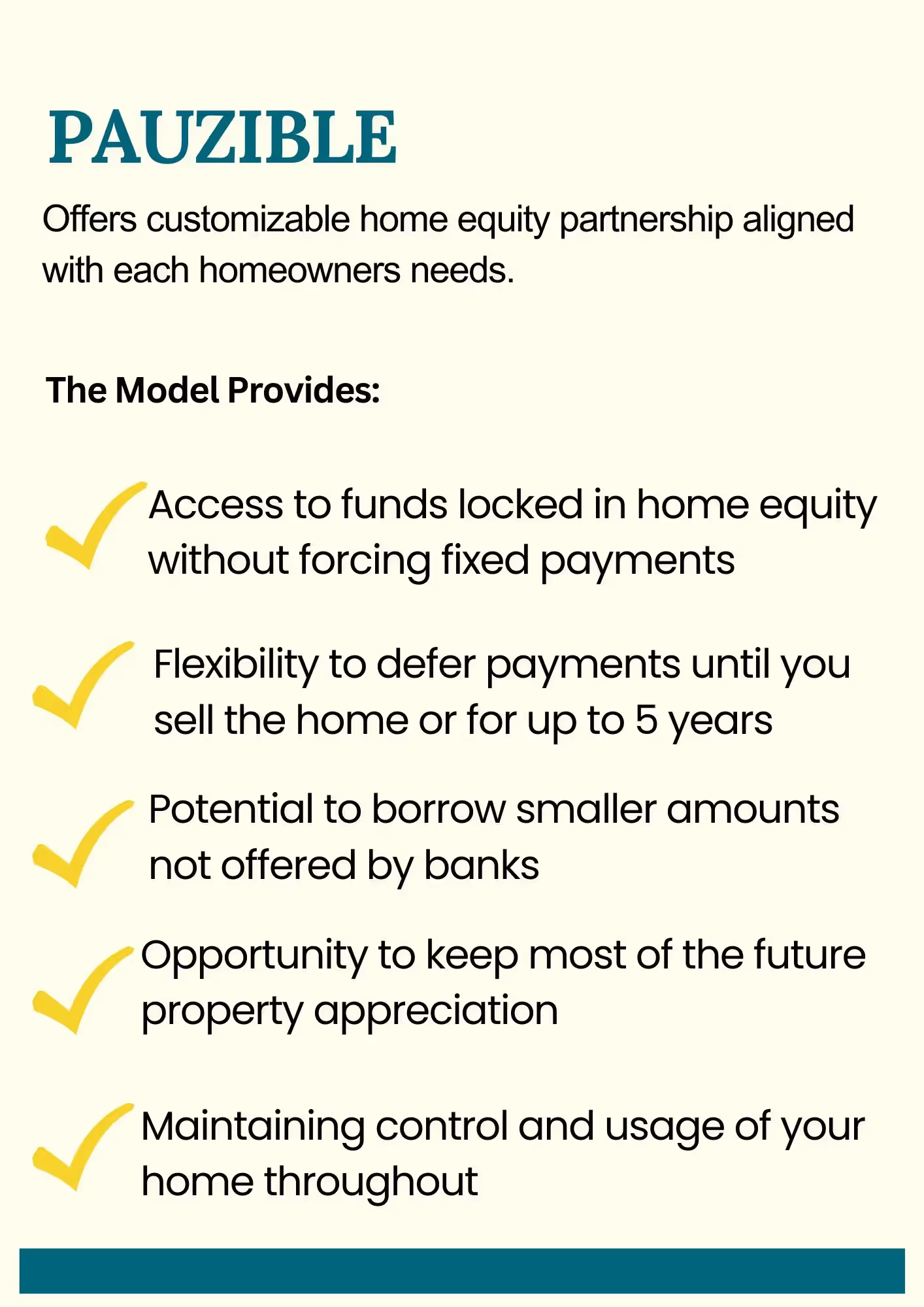

Alternative Solutions with Pauzible

Suppose you determine that a remortgage, second-charge mortgage, or home equity loan needs to be better suited for your situation. In that case, innovative alternatives like Pauzible may provide a better borrowing experience.

Reasons why traditional home equity borrowing options might not be viable could include:

Need funds for a shorter period rather than a long-term loan

Seeking smaller borrowing amounts

Want to avoid fixed monthly repayment obligations

Unfavourable loan terms or unaffordable payments

Pauzible focuses on collaborative equity sharing, giving homeowners an alternative path to access capital when they need it most while retaining ownership. This innovative approach may help if standard borrowing methods don't match your financial preferences or constraints.

Pauzible opens more possibilities for UK homeowners by providing creative home equity solutions.

FAQs:

Q. Is it a good idea to borrow more on mortgage?

A: Borrowing more on your mortgage is a sensible option if your home's value has increased. But, consider the long-term implications, such as increased loan-to-value ratios and potential difficulty in remortgaging in the future. Needless to say, any borrowing should be for a sensible purpose.

Q. How can I make sure I borrow responsibly?

A: Borrow responsibly by checking your credit record, ensuring you can afford the monthly payments, and making sure the value of your home has increased. Use mortgage affordability calculators and budget planners to understand your financial capability before borrowing.

Q. What are the key differences between a remortgage and a second mortgage?

A: Remortgage is replacing your current mortgage with a new one, while a second mortgage is an additional loan against the equity in your home. Further advance rates are usually lower than personal loans.

Q. What factors should I consider when choosing a secured loan provider?

A: Compare interest rates, loan terms, fees, and reputation when choosing a secured loan provider. Look for flexibility in repayments and early repayment charges. Consider lenders who perform soft searches during initial comparisons to avoid impacting your credit rating.

Q. What can you use the additional money for?

A: A secured loan can provide extra funds for home improvements, investing in a new property, or other major purchases. It's recommended to use such loans for projects that add value to your property or for significant investments, rather than for paying off existing debts.

Q. Will you be charged any fees if you borrow more on your mortgage?

A: Borrowing more on your mortgage may come with fees such as arrangement, valuation, and legal fees. Ask your lender about any potential fees and factor them into the overall cost of borrowing.

Q. What is additional borrowing?

A: Additional borrowing is taking on more debt, typically at a different rate than your main mortgage, for significant expenditures or to raise funds for a particular purpose.

Q. How long does it take to receive the money?

A: Getting money from additional borrowing on your mortgage can take several weeks. It involves a credit check, affordability assessment, and property valuation.

Q. Can you take out additional borrowing on mortgage to pay off any debts?

A: You can use your mortgage to pay off debts, but it can be risky. Consider the long-term costs for both obligations before doing so.

About the author

Pauzible Team

Editorial Team

The Pauzible Team consists of finance professionals and property market specialists dedicated to reinventing home ownership and BTL financing. With deep expertise across UK real estate and innovative financial products like Equity Partnership Agreements, we provide landlords and homeowners with the insights they need to unlock equity, navigate market volatility, and build sustainable wealth through property. Our mission is to make complex property finance simpler, quicker, and more accessible for everyone.

Ready to see what Pauzible could unlock?

Explore how accessing equity from your BTL property could support your business investment plans.

No obligation. Just a clear view of what might be possible.