The Closing Explained

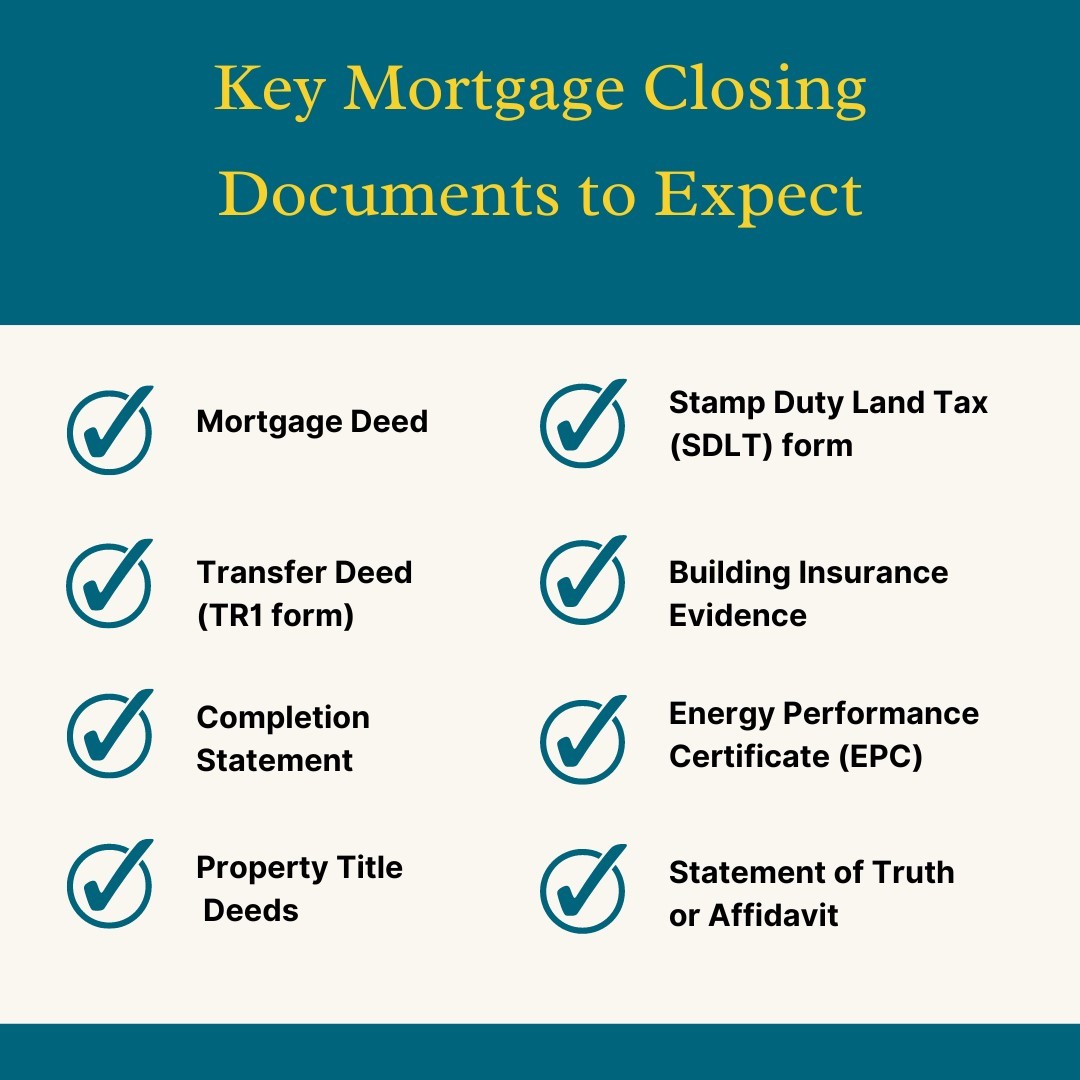

A mortgage closing, also known as completion, is the final step in the process of buying a home with a mortgage. This is when the legal transfer of the property from the seller to the buyer is finalised. The process involves several steps. First, all the financial transactions are settled and the buyer's solicitor will ensure that all parties have signed all the necessary documents. These include the mortgage deed and transfer deed. These documents are important as they legally bind the buyer to the mortgage terms and transfer the property's ownership. Any outstanding fees will be paid, including any solicitor's fees and stamp duty land tax. Once everything is signed and all funds have been transferred, the seller can hand over the keys to the property. The buyer's solicitor will then register the transfer deed with the Land Registry which completes the transaction.