Understand the mortgage default and repossession process, potential consequences, and strategies to avoid repossession, including seeking help from counseling agencies.

08/04/2025By Pauzible Team · Editorial Team

A mortgage default occurs when a borrower fails to fulfil the agreed-upon terms of their mortgage loan by not making timely payments. Failure to make payments as scheduled can potentially result in the lender initiating repossession proceedings. Mortgage defaults are often triggered by financial hardship resulting from events such as job loss, illness, unexpected expenses or an increase in mortgage rates. Anyone facing financial difficulties should understand the potential consequences of a mortgage default.

Potential Consequences of Default

The potential consequences of defaulting on a mortgage include:

Repossession: One of the most significant consequences of mortgage default is the risk of repossession. If the homeowner continues to miss payments and fails to reach an agreement with the lender, the lender may start repossession proceedings.

Damage to Credit Score: Defaulting on a mortgage can severely damage the homeowner's credit score. A lower credit score can make it challenging to obtain credit in the future and may result in higher interest rates when credit does become available.

Legal Costs: If repossession proceedings are initiated, the homeowner may be liable for legal costs associated with the process. These costs can add to the financial burden of defaulting on the mortgage.

Homelessness: In severe cases, defaulting on a mortgage can lead to homelessness if the homeowner is unable to find alternative housing.

Understanding the Repossession Process

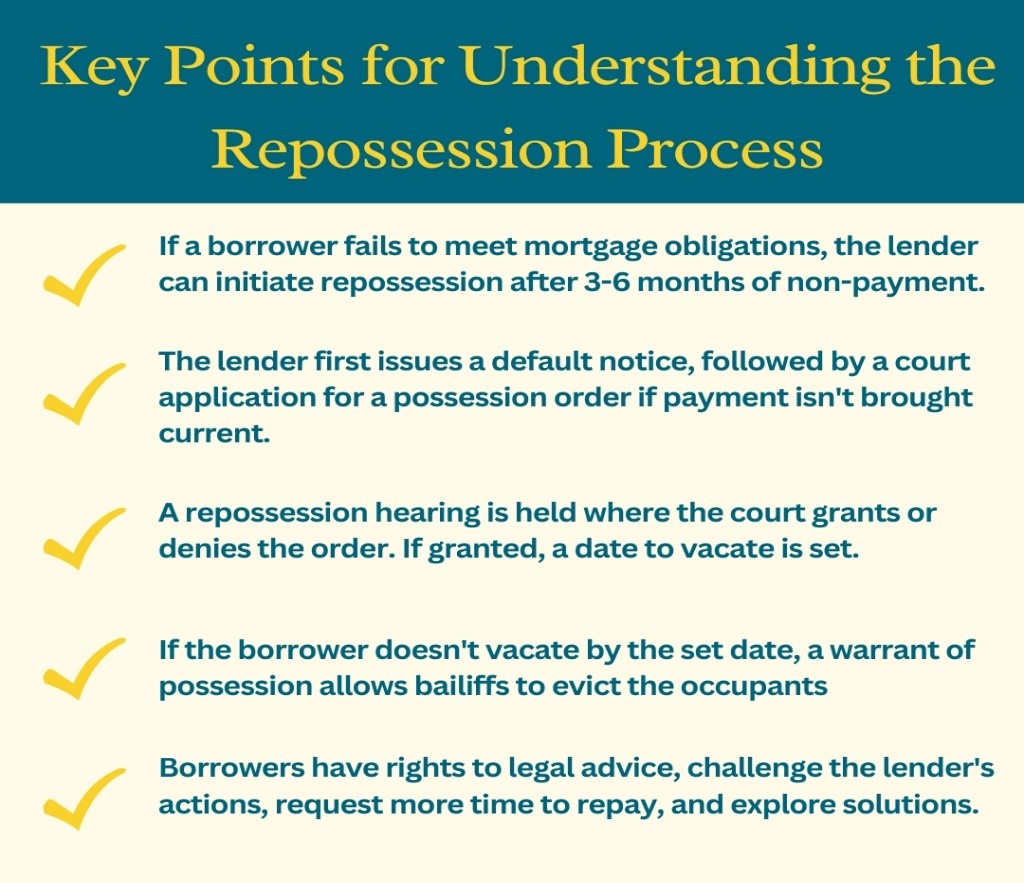

The repossession process is a legal procedure through which a lender takes possession of property from a borrower who has failed to meet their mortgage obligations. The process begins when the borrower falls behind on mortgage payments. After a certain period of non-payment, usually around three to six months, the lender can initiate legal proceedings to repossess the property.

The first step in the repossession process is for the lender to issue a default notice to the borrower. This document informs them of their arrears and gives them a specified time period to bring their payments up to date. If the borrower fails to do this, the lender can apply to the court for a possession order. The lender will have to submit evidence of the borrower's arrears and demonstrate that all necessary steps have been taken to keep the borrower informed and assist them to resolve the situation.

Once the possession order is granted, the court will set a date for a repossession hearing. This is where both the lender and the borrower have the opportunity to present their respective cases. If the court is satisfied that the lender has followed the correct procedures and that repossession is justified, it will issue a repossession order. This will specify a date by which the borrower must vacate the property. If the borrower fails to leave the property by the specified date, the lender can apply for a warrant of possession. This authorises bailiffs to evict the occupants and take possession of the property on behalf of the lender. The bailiffs will typically give the occupants a final opportunity to leave voluntarily before physically removing them from the property. In some cases, the court may grant a suspended possession order. This allows the borrower to remain in the property under certain conditions are met. This could be as simple as adhering to a repayment plan.

Throughout the repossession process, borrowers have certain rights and protections, including the right to seek legal advice and representation. They also have the right to challenge the lender's actions in court, request more time to repay their arrears and explore alternative solutions. Borrowers facing repossession should understand the importance of acting quickly and ideally engaging with their lender to try to resolve the situation before it reaches the courts.

Understanding Homeowners' Rights

Homeowners have certain rights when a mortgage goes into default. These rights aim to safeguard homeowners from unfair practices and provide opportunities to address the default and potentially avoid repossession.

One of these rights is the right to be informed. Lenders are required to provide homeowners with clear and transparent information about their mortgage terms. This includes any arrears, fees and potential consequences of default. This allows homeowners to understand their rights and options for addressing the default.

Homeowners also have the right to seek assistance and negotiate with their lender. Most lenders have procedures in place to help borrowers in financial difficulty, such as offering payment plans, temporary forbearance or refinancing options. It is crucial for homeowners to communicate with their lender as soon as they anticipate or experience difficulties in meeting their mortgage payments to explore these options.

Homeowners also have the right to legal representation and due process if repossession proceedings are initiated. This includes the right to attend court hearings and present their case before a judge. Courts will consider factors such as the homeowner's financial circumstances, efforts to address the arrears and any potential hardship repossession may cause. They also have the right to challenge the lender's actions in court, request more time to repay their arrears and explore alternative solutions.

While defaulting on a mortgage can be stressful and challenging, homeowners have rights and protections in place to help them navigate the process. This is to help them potentially avoid repossession. It is essential for homeowners facing financial difficulties to be aware of their rights and seek assistance from legal advisors or housing counsellors to explore all available options.

Strategies for Avoiding Repossession

Avoiding repossession requires proactive strategies and timely action from homeowners facing financial difficulties. One effective approach is to maintain communication with the lender. Open and honest communication allows homeowners to explain their situation and explore potential solutions. This may include loan modifications; revised repayment plans or forbearance agreements. Many lenders have specialized departments dedicated to assisting borrowers in financial distress. Reaching out early can increase the likelihood of finding a mutually beneficial resolution.

Another strategy is to seek assistance from housing counselling agencies or legal advisors. These professionals can provide guidance on navigating the repossession process, understanding homeowners' rights and exploring available options for avoiding repossession. They can also negotiate with lenders on behalf of homeowners to secure favourable terms and alternatives to repossession. Financial planning and budget management are also essential in preventing repossession. Homeowners should assess their financial situation realistically. They should prioritize essential expenses and explore ways to increase income or reduce expenses to free up funds for mortgage payments. Creating and sticking to a realistic budget can help homeowners stay on track with their mortgage obligations and avoid falling into arrears.

Homeowners who are unable to afford their current mortgage payments may need to explore alternative housing options. This could involve downsizing to a more affordable property or possibly renting out a portion of the home to generate additional income. If none of those options are viable, then looking into government assistance programmes for housing support might be the solution.

Overall, preventing repossession requires a proactive and multi-faceted approach that includes communication with lenders, seeking professional assistance, managing finances effectively and considering alternative housing options. By taking timely action and exploring all available resources, homeowners can increase their chances of avoiding repossession and preserving homeownership.

Getting Help and Advice

Homeowners facing mortgage difficulties can access various resources to help them navigate their financial challenges and potentially avoid repossession. One valuable resource is counselling agencies, which provide free or low-cost counselling services to homeowners in financial distress. These agencies offer personalised guidance on managing mortgage payments, negotiating with lenders and exploring alternatives to repossession. They can also provide information on government assistance programmes and legal rights for homeowners. Examples of such agencies are Citizens Advice, National Debt line and Shelter. These organizations offer workshops, seminars and one-on-one counselling sessions to educate homeowners about their options and provide support throughout the repossession process. They may also have legal experts who can assist homeowners with legal proceedings and represent them in negotiations with lenders.

In addition, homeowners in financial distress can also reach out to their local council. Government assistance programmes are also available to support homeowners facing mortgage difficulties. For example, the government offers schemes to help struggling homeowners such as the Support for Mortgage Interest. These provide eligible homeowners with financial assistance.

Another option is online resources and informational websites, which can help homeowners gain valuable knowledge about dealing with mortgage difficulties. Websites operated by government agencies, housing organizations, and financial institutions often provide guidance on repossession prevention, mortgage assistance programmes and steps to take when experiencing financial hardship.

Overall, homeowners facing mortgage difficulties have access to a range of resources and support services to help them navigate their financial challenges and explore options for avoiding repossession. Homeowners can increase their chances of finding a viable solution by seeking assistance early and exploring all available resources.

FAQs:

Q. What happens if I miss mortgage payments?

A: If, you miss mortgage payments, you risk defaulting on your mortgage, which can lead to the lender repossessing your home.

Q. What is the difference between mortgage default and repossession?

A: Mortgage default occurs when a homeowner fails to make their mortgage payments, while repossession is the legal process by which the lender takes possession of the property due to default.

Q. What is the mortgage default and repossession process?

A: The mortgage default and repossession process typically involve arrears management, notice of default, possession order and eviction if the homeowner fails to address the arrears.

Q. What are my rights as a homeowner facing mortgage default?

A: Homeowners facing mortgage default have rights to information, representation and fair treatment throughout the repossession process.

Q. How can I prevent mortgage repossession?

A: To prevent mortgage repossession, homeowners can communicate with their lenders, consider mortgage restructuring, and access support and advice from housing debt counselling charities and government schemes.

About the author

Pauzible Team

Editorial Team

The Pauzible Team consists of finance professionals and property market specialists dedicated to reinventing home ownership and BTL financing. With deep expertise across UK real estate and innovative financial products like Equity Partnership Agreements, we provide landlords and homeowners with the insights they need to unlock equity, navigate market volatility, and build sustainable wealth through property. Our mission is to make complex property finance simpler, quicker, and more accessible for everyone.

Ready to see what Pauzible could unlock?

Explore how accessing equity from your BTL property could support your business investment plans.

No obligation. Just a clear view of what might be possible.