Understanding mortgage stress tests is important for prospective homebuyers. In simple terms, a mortgage stress test is a regulatory requirement for a lender to assess a borrower's ability to maintain mortgage payments in the event of interest rate increases.

08/04/2025By Pauzible Team · Editorial Team

Understanding mortgage stress tests is important for prospective homebuyers. In simple terms, a mortgage stress test is a regulatory requirement for a lender to assess a borrower's ability to maintain mortgage payments in the event of interest rate increases. This precautionary measure aims to mitigate the risk of default and is associated with responsible lending practices.

What is a Stress Test?

A stress test evaluates whether a borrower can continue to make mortgage payments if interest rates rise above the initial rate of the loan. The Bank of England’s Financial Policy Committee (FPC) recommended in 2014 that lenders apply an affordability test to prospective borrowers at a stress interest rate, i.e. a rate 3% above the reversion rate, which is the rate a mortgage would revert to after any discounted fixed or tracker rate deal ends. Another FPC recommendation at the time was a loan to income (LTI) flow limit, which limited to 15% the number of mortgages a lender could extend to borrowers with LTI ratios of 4.5 times or greater.

As of 20 June 2022, the FPC confirmed that it would withdraw the affordability test recommendation effective 1 August 2022, while retaining the LTI flow limit. Despite this change, the Financial Conduct Authority's Mortgage Conduct of Business rules for responsible lending still require lenders to conduct a wide assessment of affordability. This includes assessment of income vs monthly mortgage payments, other debt payments, regular household expenses and other bills, and “stress testing” the borrower’s finances in situations such as a rise in interest rates.

Why are Stress Tests Important?

The significance of stress tests lies in the potential prevention of a recurrence of past financial crises precipitated by irresponsible lending practices. The tests serve as a safeguard against an excessive accumulation of household debt and an increase in the number of highly indebted households. By ensuring that borrowers have sufficient financial capacity to withstand potential rate hikes, stress tests contribute to the stability of the housing market and the broader economy.

The Stress Test Process Explained

Lenders employ various methods to calculate a mortgage stress test. They consider factors such as the loan-to-value (LTV) ratio, which is the amount borrowed relative to the property's value, and a stressed mortgage rate to determine if the borrower can afford the mortgage in the event of interest rate increases. Other wider affordability assessment inputs include income vs. mortgage payments; other monthly expenses such as council tax, utilities, loans, credit cards, car loans, childcare, school fees and insurance; and other expenses, such as food, clothing, holidays, gym, leisure and entertainment, and so on.

For buy-to-let mortgages, the stress test calculation incorporates an interest rate cover ratio (ICR), which is the ratio of gross rental income to mortgage interest repayments. Other wider buy-to-let affordability assessment inputs include rental income vs. mortgage payments, and other costs such as service charges, letting commission, management fees, maintenance expenses and insurance premia.

Lenders may use a predetermined stress rate, such as the Bank of England's historically recommended 3% above the reversion rate, or they may employ rates based on their own proprietary stress test models that consider various economic factors and scenarios.

If a borrower fails a stress test, it may result in the mortgage application being rejected or the borrower being offered a lower affordable mortgage amount. This is because the lender deems the borrower's income insufficient to cover the potential higher mortgage payments in the event of rate increases.

Strategies to Improve Your Chances of Passing

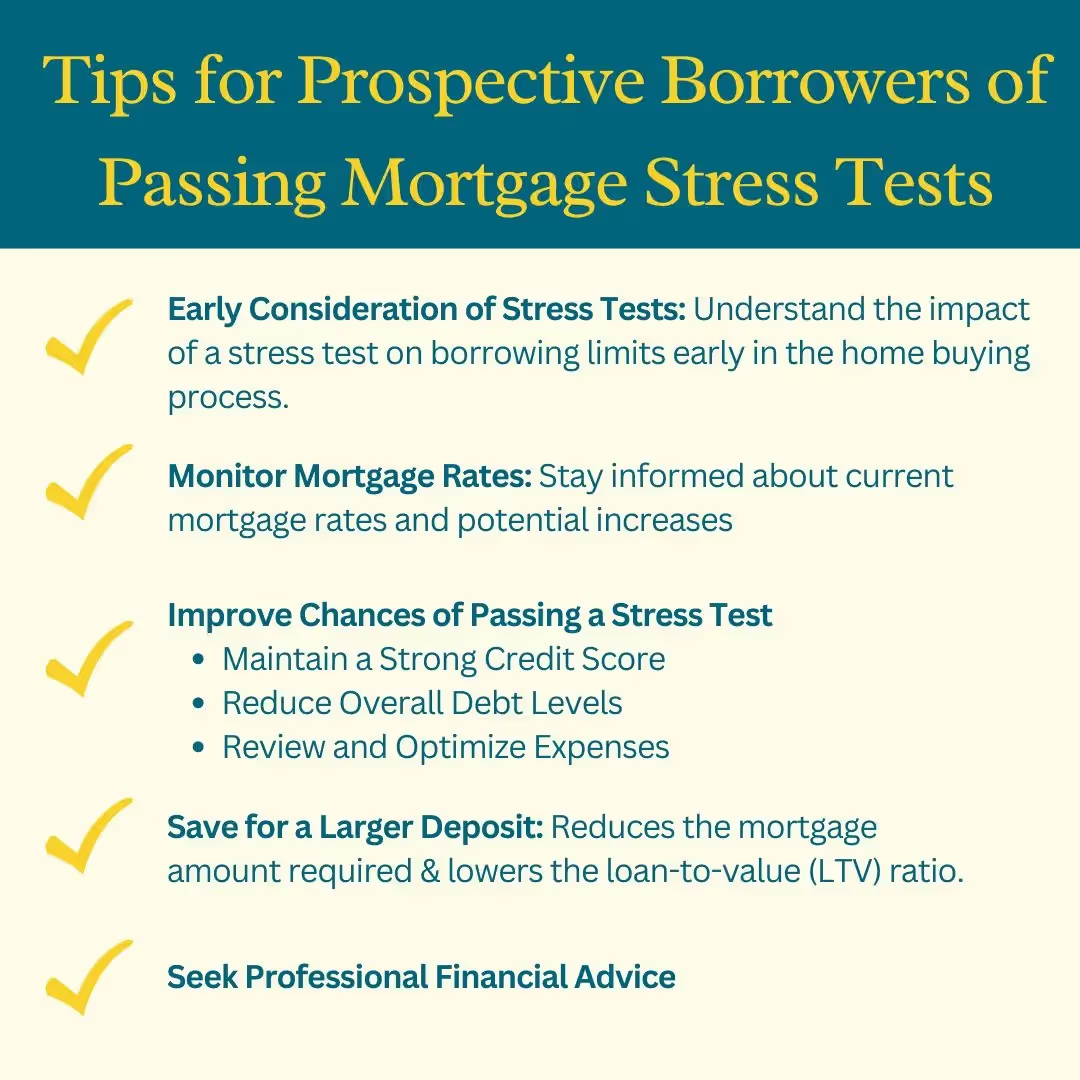

Prospective borrowers should begin considering the potential impact of a stress test, as well as other affordability criteria, such as income vs. all expenditure, on their borrowing limit early on in the home buying process. Obtaining a 'Decision in Principle', which provides a preliminary but non-binding indication of the amount that the lender might be prepared to advance, is not a substitute for a formal wider analysis of affordability, including stress testing. It is also advisable for prospective borrowers to stay informed about mortgage rates as these can sometimes rise relatively rapidly, depending on Bank of England base rate increases.

To improve their chances of passing a mortgage stress test, borrowers can take several proactive steps. Firstly, maintaining a strong credit score is important, as it demonstrates a track record of responsible borrowing and repayment. Additionally, reducing overall debt levels can increase disposable income and improve the borrower's loan-to-income ratio, a key factor considered by lenders. It is also advisable to review and optimize one’s expenses, as this can free up additional funds to allocate towards mortgage payments. Cutting unnecessary costs and demonstrating financial discipline usually enhances a borrower's profile in the eyes of lenders.

Another effective strategy is to save for a larger deposit, which can reduce the mortgage amount required and lower the loan-to-value (LTV) ratio. A lower LTV ratio not only improves the borrower's chances of passing the stress test but also potentially qualifies them for more favourable interest rates from lenders.

The Direction of Mortgage Rates

The direction of mortgage rates in 2024 will continue to be influenced by economic factors such as inflation and the base rates set by the Bank of England in response. The Bank of England rate stands at 5.25% as of 9 May 2024. With inflation showing some recent signs of decline, there is speculation about the potential for rate cuts, but their timing is still quite uncertain.

Seeking Professional Guidance

While the Bank of England withdrew its affordability test recommendation, it retained the LTI flow limit recommendation. and the Financial Conduct Authority's rules still require lenders to conduct a wide assessment of affordability, including stress testing borrower finances against a potential rise in interest rates.

In this complex environment, a professional mortgage broker can provide guidance tailored to a borrower's specific financial situation, helping them navigate the intricacies of mortgage rates and lender criteria, including affordability assessment and stress testing.

FAQs:

Q. What is a mortgage stress test?

A: A mortgage stress test is a regulatory requirement for a lender to assess a borrower's ability to maintain mortgage payments in the event of interest rate increases. This precautionary measure aims to mitigate the risk of default and is associated with responsible lending practices.

Q. Why do lenders conduct mortgage stress tests?

A: The Financial Conduct Authority's Mortgage Conduct of Business rules for responsible lending require lenders to conduct a wide assessment of borrower affordability. This includes assessment of income vs monthly mortgage payments, other debt payments, regular household expenses and other bills, and also “stress testing”.

Q. How is a mortgage stress test conducted?

A: Lenders may use a predetermined stress rate, such as the Bank of England's historically recommended 3% above the reversion rate, which is the rate a mortgage would revert to after any discounted fixed or tracker rate deal ends, or they may employ rates based on their own proprietary stress test models that consider various economic factors and scenarios.

Q. What happens if I fail a mortgage stress test?

A: If you fail a mortgage stress test, it may result in your mortgage application being rejected or the lender offering you a smaller mortgage amount. This is to ensure that you do not take on a loan that could become unaffordable in the future.

Q. Are there ways to improve your chances of passing a stress test?

A: You can potentially improve your chances of passing a stress test by ensuring a strong credit score, reducing your debts and expenses, and having a larger deposit, which will lower the loan-to-value ratio.

About the author

Pauzible Team

Editorial Team

The Pauzible Team consists of finance professionals and property market specialists dedicated to reinventing home ownership and BTL financing. With deep expertise across UK real estate and innovative financial products like Equity Partnership Agreements, we provide landlords and homeowners with the insights they need to unlock equity, navigate market volatility, and build sustainable wealth through property. Our mission is to make complex property finance simpler, quicker, and more accessible for everyone.

Ready to see what Pauzible could unlock?

Explore how accessing equity from your BTL property could support your business investment plans.

No obligation. Just a clear view of what might be possible.