How to use Pauzible to get help with mortgage payments

Times of uncertainty can be difficult and profoundly impact people's lives in different ways. The cost of your mortgage can certainly be one of those. The UK saw interest rates rise in December 2021 after unprecedented low rates for almost two years previously.

08/04/2025By Pauzible Team · Editorial Team

UK interest rate hike and inflation uncertainty

Times of uncertainty can be difficult and profoundly impact people's lives in different ways. The cost of your mortgage can certainly be one of those. The UK saw interest rates rise in December 2021 after unprecedented low rates for almost two years previously. The Bank of England has since increased interest rates dramatically to help slow down the momentum of inflation. Fast forward to 2024 and the nation faces high interest rates, and higher food and energy bills. The average person is facing a financial crisis with such factors at work. Given poor economic growth and wages not aligning with the cost of living, what can people do? Is the answer to take out a second mortgage to help with the increase in the cost of living? That would only burden finances further with a new monthly payment. Should they take out new credit cards or start using the ones they have up to their limits? Credit card borrowing, which is expensive, has soared to its highest monthly level since 2004.Bank of England data show individuals borrowed an additional £1.5bn in all forms of consumer credit, of which £1.2bn was on credit cards, as concerns mounted over the impact of high inflation on struggling households. It might be time for a different solution that has a less negative impact on already strained finances.

1

Introducing PAUZIBLE: a lifeline to homeowners

Pauzible’s product was created with the struggling homeowner in mind. The founders are a group of caring individuals deeply passionate about using their years in the financial sector to help find a solution for homeowners. They have studied the issues behind today’s financial hardships and devised an innovative solution. What if you can keep making your current mortgage payments and not have to pay the mortgage increases you might experience when your current 2- or 5-year fixed rate expires? Will that make a difference if you are struggling financially or even considering having to sell your home? Pauzible’s product is intended to help people get through this kind of problem by offering a product linked to the value of the equity in their home. Pauzible can pay the difference between the new and old monthly mortgage payments in return for a small share of the equity that you have built up in your home. You can decide the terms of the agreement, whether it be 2 or 5 years of receiving monthly payments from Pauzible. This solution allows you to get your finances sorted over a 10-year term, if necessary, with the opportunity to buy back Pauzible’s share in the value of your home at any point during that period. Pauzible can enable consumers to tap into their home equity without taking on new debt. The critical component of the agreement for many struggling households is the chance not to take on new debt.

Should I consult a Financial Advisor?

It would be advisable to consult a financial advisor or mortgage broker to guide you through the process or let you know if Pauzible’s product is unsuitable for your particular circumstances. They have qualified individuals trained to answer questions you might have.

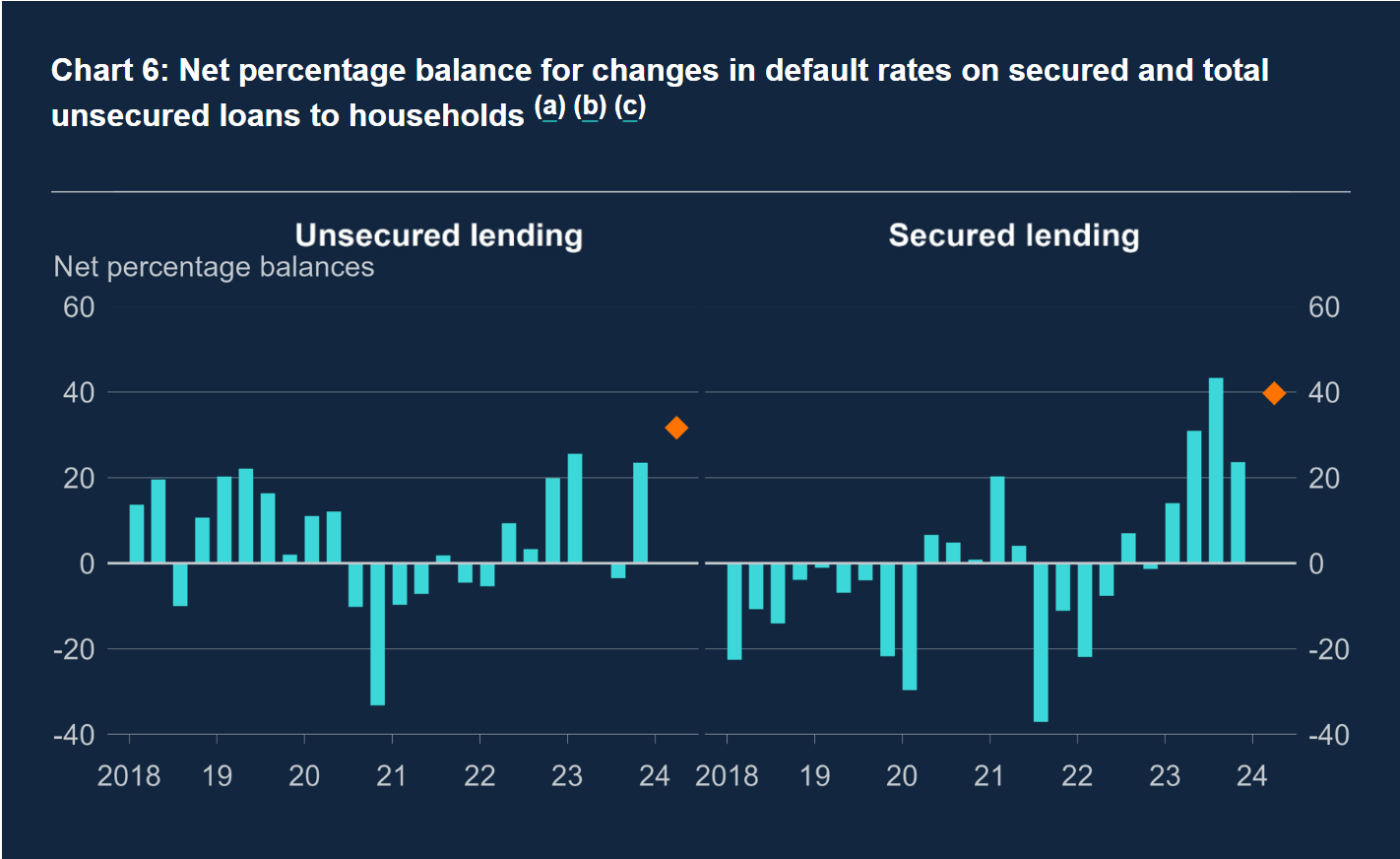

UK lenders fear defaults on mortgage payments

Source : Bank of England²

Higher interest rates and substantially higher household costs have caused people to wonder how they will afford their mortgage payments. Lenders anticipate the most significant rise in mortgage payment defaults since 2009. Lenders were already reporting an increase in defaults in the last three months of 2023.2 Default rates on secured loans to households and losses given default increased in Q4 2023. Both were expected to increase in Q1 2024. The Bank of England’s survey also found an increase in people defaulting on credit cards and unsecured loans.

Finding it hard to access or qualify for new credit?

Many people are having to rely on using their credit cards to pay for essentials and accessing new secured loans is becoming increasingly difficult. In 2023, many credit card institutions automatically increased limits on already strained households without affordability checks. These people have increased their credit card debt in 2024, along with much higher interest rates; even if they wanted to remortgage, their affordability checks would probably fail. The cost of living crisis has caused people’s finances to tighten to such an extreme that trying to apply for new loans has become almost impossible.

Conclusion

Some people wonder why the Bank of England’s Monetary Policy Committee took so long to raise interest rates to help contain inflation, but with a weakened economy and still in a pandemic, what choice did they have? People are struggling to make ends meet now, and many are going into default or having to sell their homes. Economists are predicting that interest rates will start moderating from 2025 onwards, but what are struggling households going to do in the meantine? One cannot turn the clock back on how we got here, but one can try and find a solution for struggling homeowners. Pauzible’s product might be the solution you are looking for.

FAQs:

Q. How much equity do I need to qualify for Pauzible’s product?

A: Ideally, you need at least 35% equity, although depending on your circumstances, we could consider cases with around 30% home equity.

Q. Who owns the property?

A: Pauzible will not own the property, but will share a portion of your property's value.

Q. How long can I pause my mortgage increase?

A: You can pause your mortgage increase for an agreed term of up to five years.

Q. What happens if the value of my property goes down?

A: If the value of your property goes down, we both make less. However, if you were to buy back or sell within the first three years of the contract, Pauzible will value the house no lower than at the start of the agreement.

Q. How is Pauzible different from other lending options?

A: Pauzible is different in many ways, but the main three differences are that it is not a lender, will not add any new debt, or monthly interest payments or debt repayments.

The Pauzible Team consists of finance professionals and property market specialists dedicated to reinventing home ownership and BTL financing. With deep expertise across UK real estate and innovative financial products like Equity Partnership Agreements, we provide landlords and homeowners with the insights they need to unlock equity, navigate market volatility, and build sustainable wealth through property. Our mission is to make complex property finance simpler, quicker, and more accessible for everyone.

Ready to see what Pauzible could unlock?

Explore how accessing equity from your BTL property could support your business investment plans.

No obligation. Just a clear view of what might be possible.