Overpaying your mortgage reduces your outstanding mortgage balance faster and allows you to save money on interest payments correspondingly. Multiple overpayments can also lead to your mortgage being repaid faster than originally scheduled. However, overpayment also carries some potential risks, which you need to factor into your decision. Assessing your financial situation is key.

08/04/2025By Pauzible Team · Editorial Team

Overpaying your mortgage reduces your outstanding mortgage balance faster and allows you to save money on interest payments correspondingly. Multiple overpayments can also lead to your mortgage being repaid faster than originally scheduled. However, overpayment also carries some potential risks, which you need to factor into your decision. Assessing your financial situation is key.

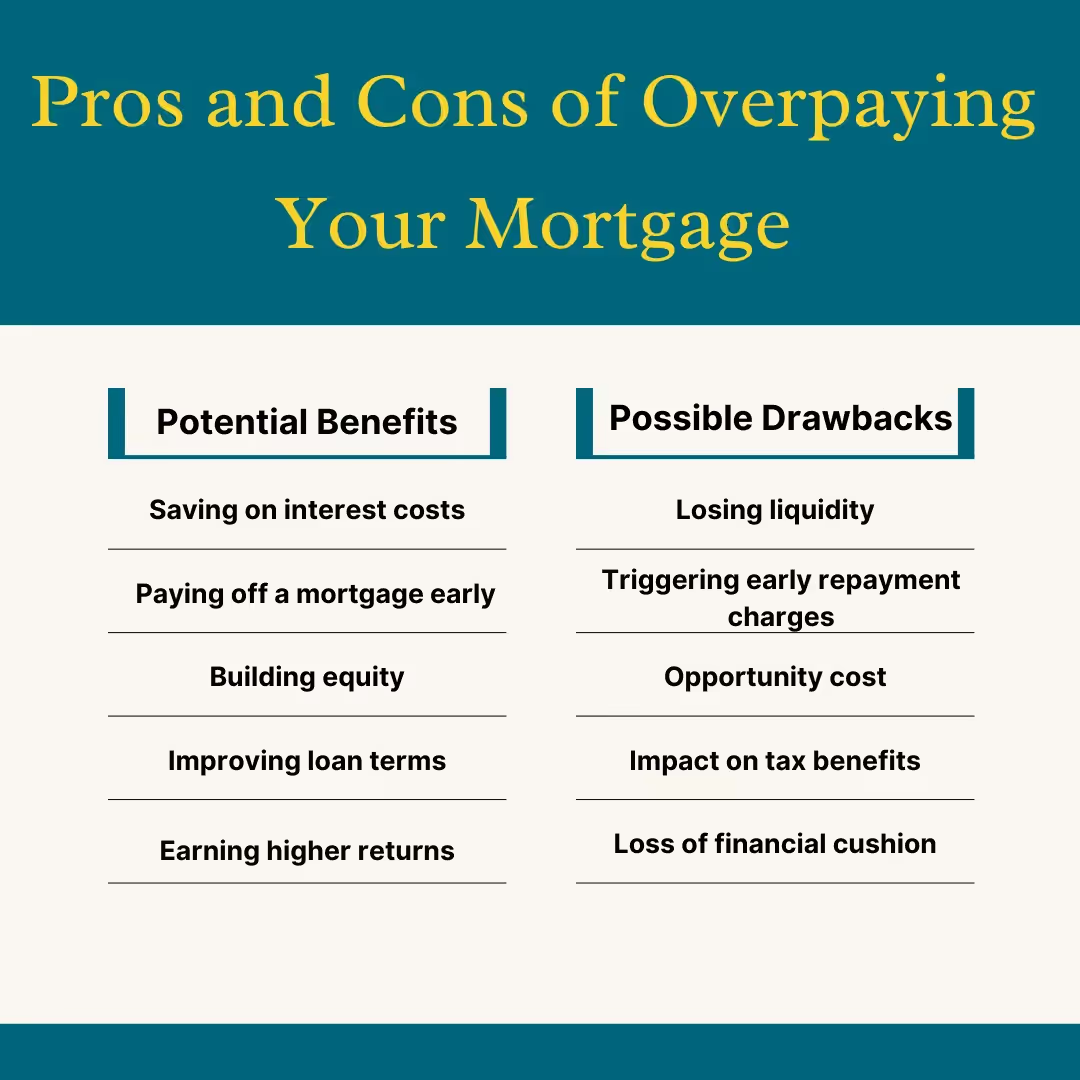

Potential Benefits

- Saving on interest costs: If you pay extra towards your mortgage, it will reduce the principal balance faster. This, in turn, will lower the total interest you will pay over the entire loan term, resulting in savings that can accumulate to significant amounts. By paying more than the required monthly payment, you can also reduce the amount of time it takes to pay off your mortgage if you so choose.

- Paying off a mortgage early: By shortening the length of your mortgage term, you can own your home outright sooner than expected. This will allow you to save money on interest charges and achieve financial freedom faster. For instance, if you have a 30-year mortgage and make extra payments towards your principal balance, you could pay off your mortgage in 20 or 25 years, depending on your extra payments.

- Building equity: Equity is the difference between the market value of your home and the amount you owe on your mortgage. As the value of your home increases, so does your equity in it. As you repay your mortgage and the outstanding balance of your mortgage reduces, over time, the value of your equity increases, too. This growth in home equity provides financial flexibility for accessing funds in the future if you need them. For example, you can borrow against the equity in your home to cover expenses such as home repairs, medical bills, or other unexpected expenses.

- Improving loan terms: Increased equity and a lower loan-to-value ratio can qualify you for better mortgage rates when remortgaging. If you have made extra payments towards reducing your mortgage and have built up equity in your home, you may be eligible for a lower interest rate when you remortgage. This can result in significant savings over the life of the loan.

- Earning higher returns: During periods of low interest rates on savings, overpayments may beat returns offered by bank deposits. Some lenders allow overpayments without early repayment charges. By making extra payments towards reducing your mortgage, you could earn higher returns by increasing your home equity which might be appreciating at a higher rate than the interest offered by banks on deposits during periods of low interest rates. You can also pay off your mortgage faster and save money on mortgage interest charges without penalties.

Possible Drawbacks

- Losing liquidity: Large lump sum payments towards reducing your mortgage could reduce your cash savings. This could leave you with less money that you could use for other goals or unexpected expenses, should the need arise. Consider carefully before making such payments and ensure that you maintain an adequate level of cash savings to manage your everyday expenses.

- Triggering early repayment charges: Some mortgages may have a prepayment penalty, meaning that you may be charged a fee if you repay a loan amount above a certain threshold. It is important to check your mortgage agreement before making additional payments to avoid triggering early repayment charges. These are applicable if you overpay beyond the limit set by your lender, typically around 10% of the remaining balance per year.

- Opportunity cost: When you make overpayments towards your mortgage, your money could have been invested elsewhere for potentially higher returns. Consider the opportunity cost of making overpayments and compare the potential returns from other investment options before you decide on making extra payments.

- Loss of financial cushion: Having less accessible cash savings could leave you vulnerable financially. It is important to maintain an emergency fund that can cover your expenses for at least 6 – 12 months. Consider the impact of making overpayments towards your mortgage on your overall financial health before making any additional payments.

Key Considerations

If you have a mortgage, overpaying is a smart move to reduce your total interest costs and accelerate your payoff. It's important to first compare your mortgage interest rate with current savings and investment rates to determine whether overpaying makes financial sense. If there is a significant differential in rates, overpaying could be a good option.

However, before you start making overpayments, you should check if your mortgage includes limits or fees that may apply to overpayments. Some mortgages may only allow you to overpay a certain amount each year or may charge a fee for overpayments.

It is also essential to assess your overall budget to gauge if you can afford lower liquid savings. Overpaying your mortgage could mean that you have less cash available for other expenses or emergencies.

To make the right overpayment decisions, you should model different scenarios of mortgage payoff timing and interest savings. This will help you to determine the best approach for your financial situation and goals. Consider consulting a financial advisor to personalize mortgage overpayment advice for your financial needs.

Overpaying your mortgage can significantly reduce interest costs and accelerate your payoff. However, evaluating your mortgage terms, financial standing and goals is important to determine if it's the right decision for you.

FAQs:

Q: Is overpaying a mortgage worth it?

A. Overpaying can generate substantial interest savings over the full loan term and allow you to pay off your mortgage early. However, it could also reduce your financial savings cushion in case of unexpected expenses or emergencies.

Q: Is it better to overpay the mortgage or save?

A. It depends on your mortgage interest rate versus rates on savings accounts. Overpaying tends to provide better returns if your mortgage rate exceeds savings account rates and property price appreciation rates are attractive.

Q: Can I overpay my mortgage?

A. Most standard mortgages allow you to overpay by up to 10% of the outstanding loan amount per year without incurring early repayment charges.

Q: Is it better to overpay mortgage monthly or lump sum?

A. Whilst moderate monthly overpayments can lead to significant interest savings over time, large lump sum overpayments achieve higher immediate savings.

Q: If I overpay my mortgage, will my monthly payments go down?

A. No, regular monthly payments stay the same with overpayments - instead, your loan finish date shortens as you pay the principal down faster.

Q: Does overpaying a mortgage reduce interest?

A. Yes, overpaying directly reduces the total interest you pay over the entire mortgage term by reducing the principal faster.

Q: Is it better to pay off the mortgage or save?

A. It depends on your financial goals. Paying off your mortgage increases your home equity, but using up too much cash hinders other goals, so balance is ideal.

About the author

Pauzible Team

Editorial Team

The Pauzible Team consists of finance professionals and property market specialists dedicated to reinventing home ownership and BTL financing. With deep expertise across UK real estate and innovative financial products like Equity Partnership Agreements, we provide landlords and homeowners with the insights they need to unlock equity, navigate market volatility, and build sustainable wealth through property. Our mission is to make complex property finance simpler, quicker, and more accessible for everyone.

Ready to see what Pauzible could unlock?

Explore how accessing equity from your BTL property could support your business investment plans.

No obligation. Just a clear view of what might be possible.