Renting Properties to Universal Credit Recipients in the UK: Navigating Rental Realities

The landscape of the UK rental market is multifaceted, including tenants receiving Universal Credit, the welfare system designed to help claimants with living costs. Recipients of this benefit are sometimes met with hesitation from private landlords due to perceptions of financial instability. However, by understanding Universal Credit better, landlords can potentially establish fruitful relationships with tenants relying on welfare.

08/04/2025By Pauzible Team · Editorial Team

The landscape of the UK rental market is multifaceted, including tenants receiving Universal Credit, the welfare system designed to help claimants with living costs. Recipients of this benefit are sometimes met with hesitation from private landlords due to perceptions of financial instability. However, by understanding Universal Credit better, landlords can potentially establish fruitful relationships with tenants relying on welfare.

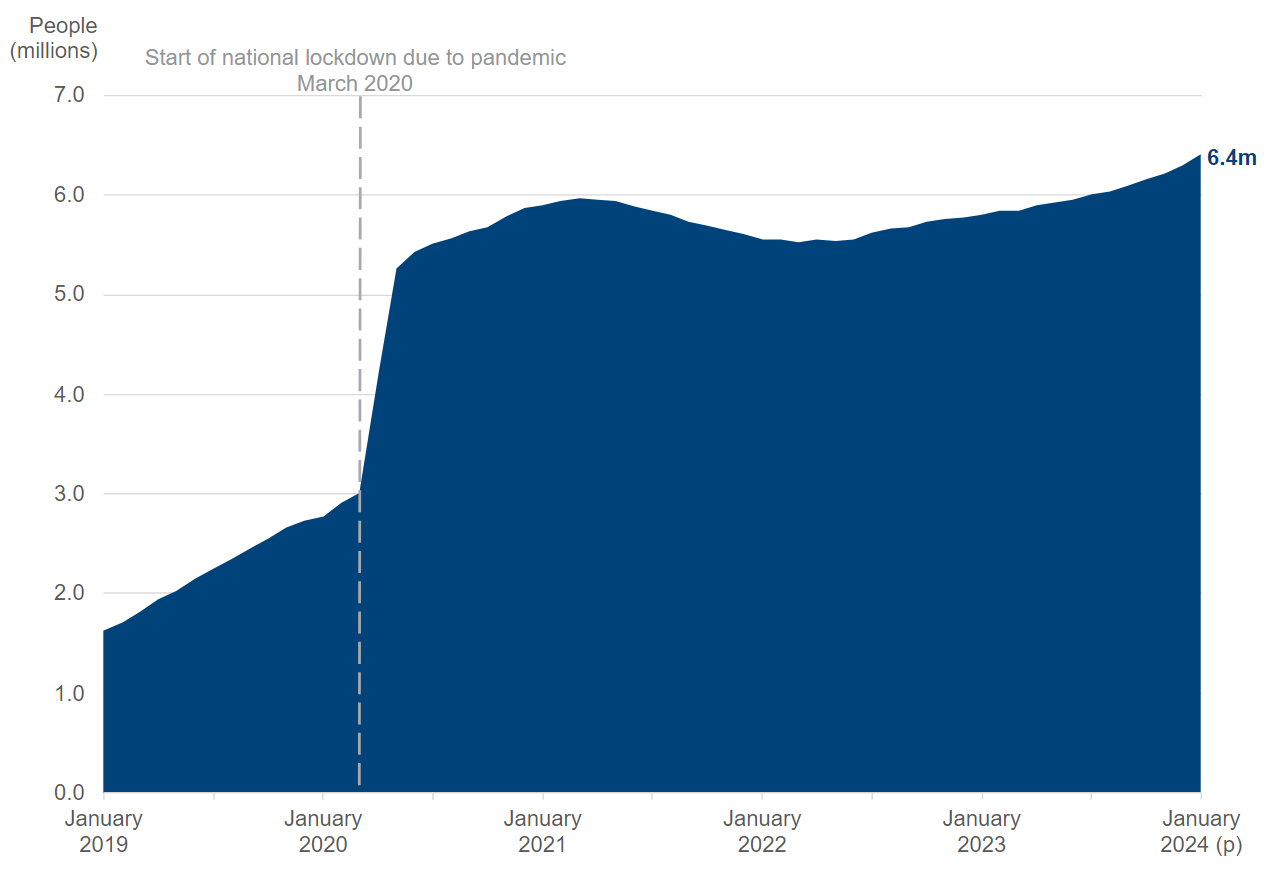

In January 2024, the UK’s Universal Credit system supported 6.4 million individuals, signifying its integral role in the nation’s social security framework1. A notable trend observed was that a large segment of these claimants (37%) fell into the category that does not require them to seek employment as a condition for receiving benefits.

People on Universal Credit, Great Britain, January 2019 to January 2024

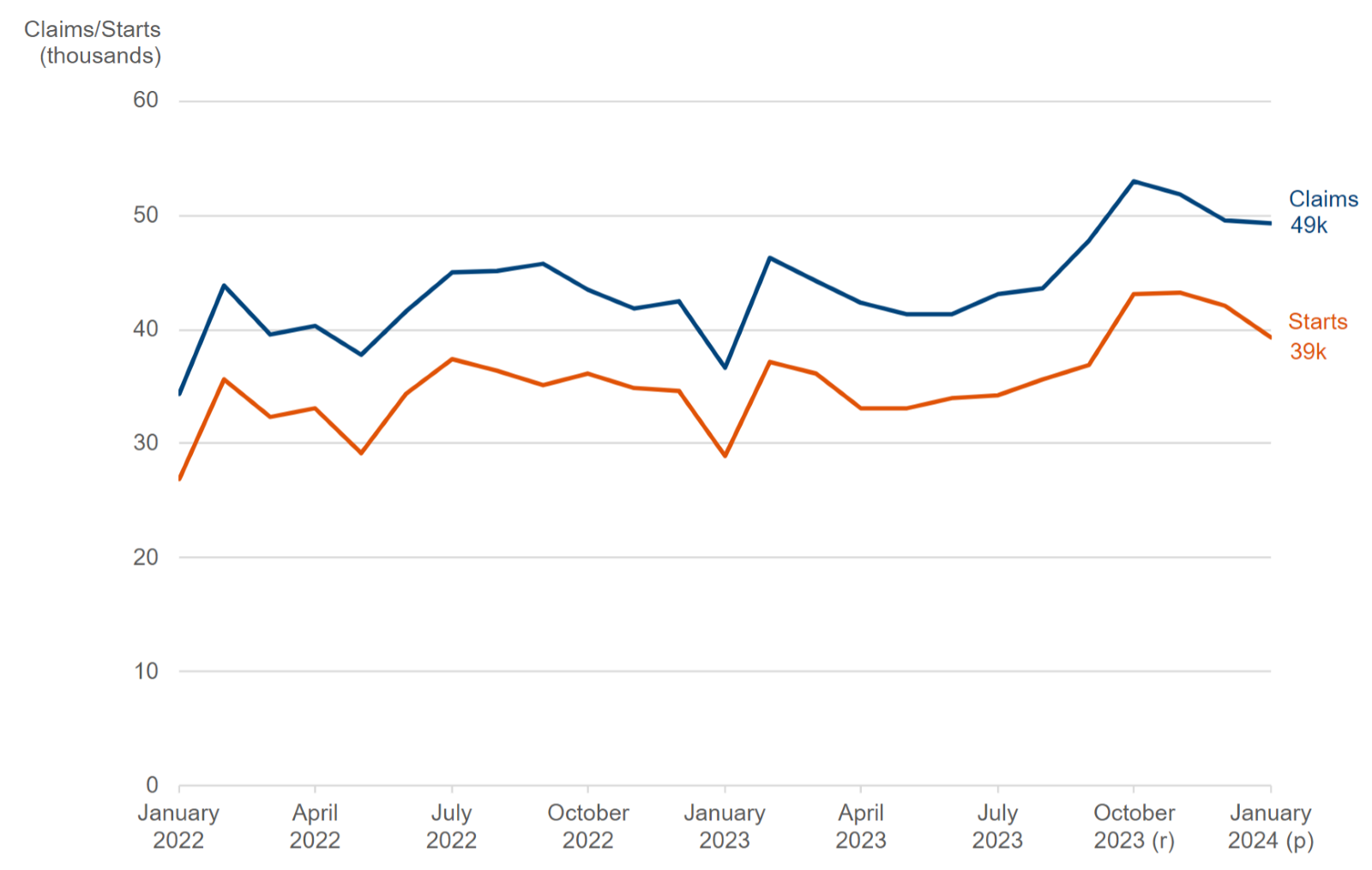

During January 2024, Universal Credit saw an average of 49,000 new claims each week, with 39,000 claimants commencing their benefits. This underscores the dynamic nature of the system, with a significant number of new individuals seeking assistance and a large number being continually integrated into the programme.

Claims and Starts to Universal Credit, average weekly rates, Great Britain, January 2022 to January 2024

Families with children represent a significant portion of the Universal Credit system, accounting for half of all households that received payments in November 2023. This reflects the system's role in providing critical financial support to families. Furthermore, in November 2023, there were 163,000 households that benefited from the Universal Credit childcare element, highlighting the program's assistance in enabling parents to access childcare services, which is often a vital factor in supporting families and enabling parents to work.

Renting to Tenants on Universal Credit in the UK

Accepting tenants on Universal Credit may require landlords to consider alternative rent payment arrangements, such as having the housing element of Universal Credit paid directly to them. This option can safeguard against rent arrears, a primary concern cited by private landlords about tenants claiming the benefit.

Universal Credit Housing Element

The housing element of Universal Credit helps claimants with rental costs. As a supportive measure, private landlords can provide a letter confirming tenancy, which is essential for tenants to secure this aspect of Universal Credit.

Landlord Rights and Responsibilities

As a landlord, it is important to understand that you have certain rights and responsibilities. Firstly, you have the right to receive rent from your tenants in a timely manner. However, this right must be balanced with your duty to ensure that the property you are renting out is habitable and safe to live in. This includes making sure that the property meets all necessary building and safety regulations, as well as being free from any hazards or dangers that could pose a risk to your tenants.

Additionally, if you are renting to Universal Credit tenants, you have a responsibility to ensure that you are accommodating their needs appropriately. For example, you may need to make necessary adaptations to the property to ensure that it is accessible and suitable for disabled tenants. You may also need to consider the impact that your rental policies and practices have on tenants who are on a low income, and take steps to ensure that you are not unfairly discriminating against them.

By balancing your rights with your responsibilities as a landlord, you can help to ensure that your tenants are happy, safe and satisfied with their rental experience. This can lead to long-term tenant relationships, positive reviews and a good reputation as a landlord.

Tenant Checks and References

When evaluating potential tenants who receive state benefits, it is crucial to conduct a comprehensive screening process. This involves verifying their income, employment history and credit score to determine if they can afford the rent and if they have a history of paying bills on time.

For individuals without a traditional rental history, such as first-time renters or those who have been living with family or friends, it may be necessary to obtain alternative references. These references may include personal or professional contacts who can vouch for the tenant's character, reliability and ability to comply with lease terms.

In summary, thorough tenant screening is necessary to ensure that the tenant will be a good fit for the property and that the landlord's investment is protected. Alternative references can provide valuable information for those without a rental history, increasing the chances of making an informed decision.

Guarantor Options

Requiring a guarantor to cover rent if tenants cannot pay helps landlords manage financial risks. Guarantors are often required for tenants receiving benefits. They provide landlords with a backup plan in case of financial difficulties. However, landlords should ensure that the guarantor is willing and able to fulfil their obligations before signing a lease agreement.

Rent Arrears and Evictions

Landlords should be aware of the necessary protocols and legal procedures involved in reclaiming their owed rent from tenants who are unable to fulfil their financial obligations. It is important to have a clear understanding of the laws and regulations governing the landlord-tenant relationship, including the eviction process, in case this course of action becomes unavoidable. By following the correct procedures, landlords can protect their rights while ensuring that tenants are treated fairly and with respect.

Fair Housing Rights and Anti-Discrimination

It is essential landlords comply with fair housing laws and avoid discriminating against tenants on benefits. Such an inclusive approach can positively impact the housing crisis by providing homes to those most in need.

Ultimately, embracing Universal Credit recipients with an informed, empathetic approach can lead to stable tenancies and support community members through difficult times.

FAQs:

Q. Why does Universal Credit ask for my details as a landlord?

A: Your tenant must provide evidence of their rent liability and proof that they are living in your property. This evidence should confirm:

tenant and landlord’s name, address and contact details

address of the property

date the tenancy began and how long the term is

amount of rent and how often it is paid

any deposit amounts payable

Your tenant may also ask you to confirm in writing that they are living in your property if they do not have any other evidence of this.

Q. How do I get my tenant’s housing benefit paid directly to me?

A: To have your tenant’s housing benefit from Universal Credit paid directly to you, you will need to apply for an Alternative Payment Arrangement (APA) through the Department for Work and Pensions (DWP).

Q. Can I find out if my tenant is claiming housing benefits?

A: Landlords can typically only find out if a tenant is claiming housing benefits if the tenant informs them, as this information is private.

Q. Is Universal Credit paid in arrears?

A: Yes, Universal Credit payments are made in arrears, usually one month after the claim and then monthly on or about the same date.

Q. Does Universal Credit contact landlords?

A: Universal Credit may contact landlords if there are issues with the housing component of the claim or if the tenant has requested that the rent be paid directly to the landlord.

The Pauzible Team consists of finance professionals and property market specialists dedicated to reinventing home ownership and BTL financing. With deep expertise across UK real estate and innovative financial products like Equity Partnership Agreements, we provide landlords and homeowners with the insights they need to unlock equity, navigate market volatility, and build sustainable wealth through property. Our mission is to make complex property finance simpler, quicker, and more accessible for everyone.

Ready to see what Pauzible could unlock?

Explore how accessing equity from your BTL property could support your business investment plans.

No obligation. Just a clear view of what might be possible.