Investing in a buy-to-let (BTL) property with funding from a BTL mortgage is a strategic way of generating income and building wealth over time. This guide aims to explain the process of securing a BTL mortgage, focusing on understanding eligibility and the application process and providing tips for prospective landlords.

08/04/2025By Pauzible Team · Editorial Team

Investing in a buy-to-let (BTL) property with funding from a BTL mortgage is a strategic way of generating income and building wealth over time. This guide aims to explain the process of securing a BTL mortgage, focusing on understanding eligibility and the application process and providing tips for prospective landlords.

Introduction to BTL Mortgages

A BTL mortgage is a specialized financial product designed for investors looking to purchase property specifically for the purpose of renting it out. Unlike traditional owner occupied residential mortgages, BTL mortgages are assessed based on the expected rental income of the property rather than the borrower's personal income. However, most lenders will still require proof that the BTL borrower has a certain basic level of personal income.

Other factors are also taken into account while assessing the mortgage, such as the remaining length of the lease (unless it is a freehold property), condition and value of the property, the amount of the deposit, amount to be borrowed, stress testing of the mortgage interest rate against expected rental income, the borrower’s prior experience of BTL properties and so on.

When planning a property purchase with a BTL mortgage, it's wise to allow for some flexibility in your timeline to account for any unforeseen delays in the approval process.

Understanding BTL Mortgage Eligibility

Eligibility for a BTL mortgage hinges on several key factors that lenders use to evaluate the borrower's suitability, property’s suitability and potential profitability of the investment:

Minimum Personal and Rental Income Requirements: Most BTL lenders insist on a minimum annual personal income of £25,000 to £30,000. This income threshold serves as a safety net, ensuring that the borrower has a stable source of income to cover potential void periods or unexpected expenses.A good credit score, typically above 700, is required to demonstrate financial reliability and responsible borrowing history. Lenders will also view the borrower's credit report to assess their ability to manage debt effectively.

In addition, lenders will want to assess the expected rental income from the property versus outgoings, including monthly mortgage payments, letting agent fees, service charges, insurance premia, maintenance costs and so on. Mortgage payments will be considered at significantly higher interest rates than present rates in order to stress test future affordability and profitability should rates rise.

Deposit Requirements: For BTL mortgages, a larger deposit is usually required, often at least 25% of the property’s value and sometimes no less than 35% - 40%. This higher deposit requirement provides lower loan-to-value (LTV) ratios, reducing the lender's risk and also enables borrowers to secure better interest rates. Nevertheless, BTL mortgage interest rates typically tend to be higher than owner occupied residential rates.

Property Requirements: Lenders will also have a property survey done to establish that the remaining lease is sufficiently long (unless it is a freehold property), the condition and value of the property, the rental yield, property price appreciation prospects and so on.

Investment Experience and Strategy: Some lenders may assess the borrower's experience in property investment and their strategy for managing the rental property, including factors such as tenant selection, property maintenance and cash flow management.

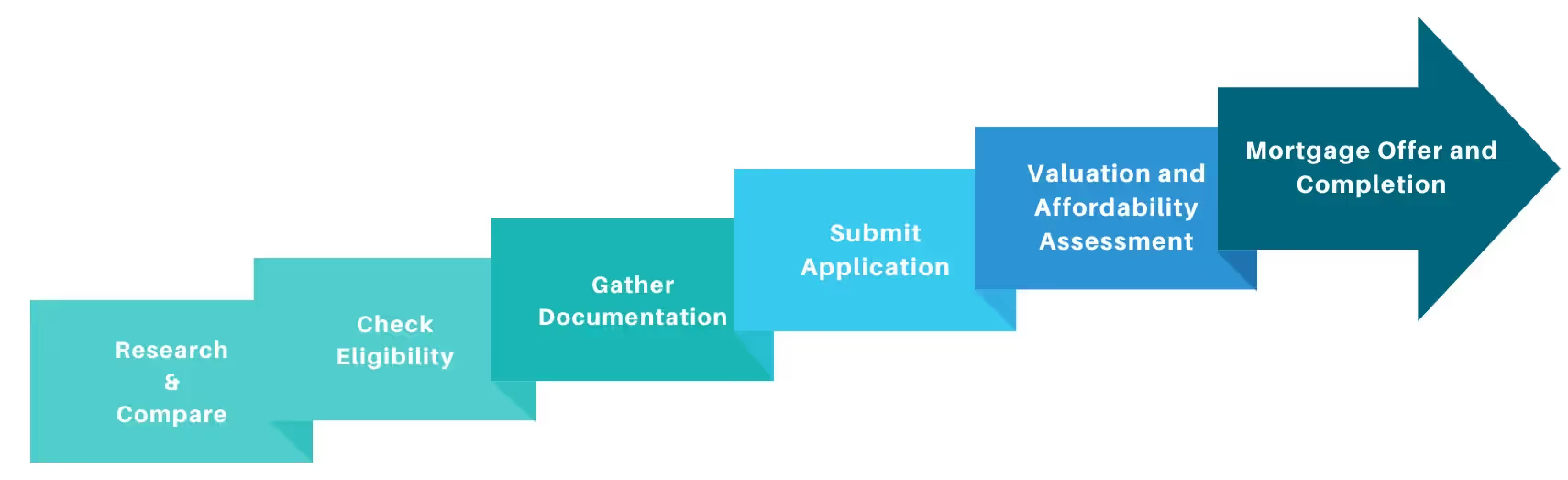

Steps to Apply for a Buy-to-Let Mortgage

1. Research and Compare: Conduct thorough research and compare various lenders, interest rates and fees associated with BTL mortgages. This preliminary research is essential to find the best deal suited to your needs and investment goals.

2. Check Eligibility: Before proceeding with the application process, carefully review the lender's eligibility criteria to ensure you meet all the requirements, including personal income, credit rating, deposit requirements, rental income, profitability and property requirements.

3. Gather Documentation: You will need to provide documentation, including proof of income and expenses (such as payslips and bank statements); proof of identity (such as passport or driving licence); proof of address (such as utility or council tax bills or bank statements); details of the property you plan to purchase, and expected rental income and profitability; and details of any investment properties you already own (including borrowing, rental income and profitability).

4. Submit Application: Once you have gathered all the necessary documentation, submit your application and the required supporting documents. Many lenders now offer online application portals for a more streamlined process.

5. Valuation and Affordability Assessment: After receiving your application, the lender will evaluate the property you intend to purchase, including the length of the remaining lease (unless it is a freehold property), the condition and value of the property, expected rental yield, property price appreciation prospects and so on. Additionally, they will also assess personal and rental income and affordability, including stress testing; credit rating; size of deposit and loan-to-value and so on.

6. Mortgage Offer and Completion: If your application is successful, you will receive a formal mortgage offer from the lender. Review the offer carefully, ensuring all the terms and conditions align with your expectations. If you accept the offer, you can complete the necessary legal formalities and finalize the mortgage agreement.

Additional Tips

Consider engaging a mortgage broker: Working with an experienced mortgage broker can be invaluable, as they can provide expert advice tailored to your specific situation, navigate the complexities of the application process, and potentially secure better mortgage rates through their arrangements with lenders than might be available to you otherwise.

Maintain transparency and honesty: It is crucial to provide accurate and truthful information to the lender throughout the application process. Misrepresenting or withholding information can jeopardize your application and lead to potential legal consequences.

In conclusion, securing a BTL mortgage in the UK requires diligent research and preparation. By carefully considering current rates and requirements, your eligibility and the application process, you can navigate the path to becoming a successful landlord. Always consider consulting with a mortgage broker and other financial experts to ensure you are making informed decisions suited to your investment goals and financial situation.

FAQs:

Q. What minimum deposit is required for a buy-to-let mortgage?

A: The typical minimum deposit is around 25% of the property value, although some lenders may require more, up to 40%, depending on factors like income, credit score, rental yield, property location and applicant experience.

Q. What is a buy-to-let mortgage stress test and how does it affect my application?

A: A stress test evaluates if the expected rental income can cover mortgage payments at a higher hypothetical interest rate. Passing is usually required for approval and failing may mean needing a larger deposit and lower mortgage amount.

Q. What documents do I need for a buy-to-let mortgage application?

A: You will need to provide documentation, including proof of income and expenses (such as payslips and bank statements); proof of identity (such as passport or driving licence); proof of address (such as utility or council tax bills or bank statements); details of the property you plan to purchase, and expected rental income and profitability; and details of any investment properties you already own (including borrowing, rental income and profitability). Lenders may also want business plans for more extensive portfolios.

Q. How long does buy-to-let mortgage approval take?

A: Timelines range from 2 - 4 weeks for straightforward cases to 6 - 8 weeks or longer for less more complicated ones. Factors such as document completeness, speed of property valuation and efficiency of lender processes can impact approval speed.

About the author

Pauzible Team

Editorial Team

The Pauzible Team consists of finance professionals and property market specialists dedicated to reinventing home ownership and BTL financing. With deep expertise across UK real estate and innovative financial products like Equity Partnership Agreements, we provide landlords and homeowners with the insights they need to unlock equity, navigate market volatility, and build sustainable wealth through property. Our mission is to make complex property finance simpler, quicker, and more accessible for everyone.

Ready to see what Pauzible could unlock?

Explore how accessing equity from your BTL property could support your business investment plans.

No obligation. Just a clear view of what might be possible.