Preparing for a Mortgage Application: A UK Homebuyer's Checklist

Before applying for a mortgage, you must have a realistic understanding of your financial situation. If your financial health is in good standing, you are already improving your chances of becoming a homeowner.

08/04/2025By Pauzible Team · Editorial Team

The process of buying a home in the UK is, for one, extremely exciting. However, it can also be overwhelming. For a large part of the population, it is the biggest purchase, commitment, and, in many cases, investment made. One of the most important steps in this process is applying for a mortgage. Being well-prepared can greatly improve your chances of success. To assist UK homebuyers in preparing for a mortgage application, we have created a comprehensive checklist. This article will help guide you through the essential stages, smoothing the path to homeownership and eradicating any surprises that may lurk between the lines.

Understanding Your Finances

Before applying for a mortgage, you must have a realistic understanding of your financial situation. If your financial health is in good standing, you are already improving your chances of becoming a homeowner.

Understanding your finances entails:

Keeping a record of all your income sources to evaluate your income. Lenders usually prefer consistent and dependable income streams.

Monitor your monthly expenses to understand your spending patterns. This will help you ensure that your expenditure is less than your income. This will also provide you with intel to locate areas of improvement in your expense.

Your credit score plays a vital role in mortgage approvals. Get a copy of your credit report, check for any inaccuracies, and take steps to improve your score if necessary.

Saving for a Deposit

When buying a property for the first time in the UK you will need to put down a deposit. The higher this deposit- usually a percentage of the property price above 15%- the better your chances are of securing a lender willing to assist a first-time lender on such a scale. It will allow you to get better mortgage rates from the lender. According to This is Money¹, first-time homebuyers are looking at minimum deposits of at least 21% of the property price. A Percentage that has skyrocketed in recent years.

An effective savings strategy for a property deposit in the UK involves several key steps:

Budgeting: Assess and manage your monthly expenses to create a realistic savings plan. Identifying and reducing non-essential spending can free up more money for savings.

Savings Account: Open a dedicated savings account, possibly an ISA (Individual Savings Account), which offers tax-free interest to accumulate your deposit.

Regular Savings Contributions: Treat savings contributions like a recurring expense. Set up a direct debit to transfer a fixed amount into your savings account regularly- do this before you run other non-essential expenses when you receive your salary contributions; this will help ensure that you do not end up not having enough money to save.

Review Finances Regularly: Periodically reassess your budget and savings goals, adjusting as needed to stay on track. Do not burn extra cash; put it away.

Reduce High-Interest Debt: Paying off high-interest debt, credit card debt for example, scan reduce monthly outgoings and allow you to save more towards your deposit.

Government Schemes: Look into government schemes like the Lifetime ISA or Help to Buy, which offer bonuses or advantages for first-time home buyers.

Mortgage Research

It is important to have a good understanding of the different types of mortgages available in the market and to look for the best deals. You can start by familiarizing yourself with fixed-rate, variable, and interest-only mortgages. Additionally, it is recommended to compare offers from different lenders, such as banks and mortgage brokers, to compare interest rates and terms.

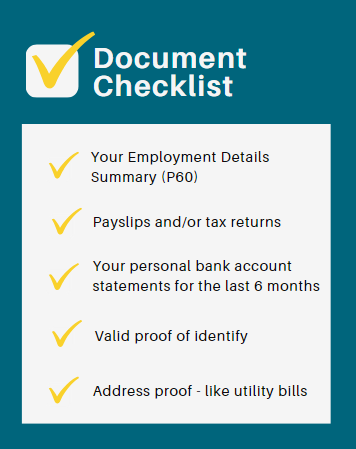

Preparing Documentation

It's important to gather all the necessary documents well in advance when applying for a loan or credit. Here are the essential documents you'll need to have:

Proof of income: This can be in the form of payslips, tax returns, or accounts if you're self-employed.

Bank statements: Usually, you'll need to provide the last three to six months of bank statements.

Identification and address proof: You'll need to provide a valid ID and utility bills or bank statements for address verification.

Budget for Additional Costs

When buying a home in the UK, there are several extra costs to consider besides the purchase price, and being aware of these costs can save you a lot of unnerving head-scratching:

Stamp Duty Land Tax (SDLT): This tax is applicable to properties over a certain value, and the amount varies based on the property price and whether you are a first-time buyer or not. At the time of going to print, first-time buyers in England and Wales buying residential property can be exempted up to £425,000 on properties costing up to £625,000².

Valuation Fee: The lender charges this fee to evaluate the value of the property you are interested in purchasing. This evaluation determines if the property purchase price aligns with the actual value.

Survey Costs: These are the expenses related to examining the condition of the property you wish to buy.

Legal Fees: This fee is paid to a solicitor or conveyancer for handling the legal aspects of your property purchase.

Mortgage Arrangement and Broker Fees: If you use a mortgage broker, you may be charged a fee for their services. Furthermore, there may be a charge from the lender for setting up the mortgage. .

Insurance: You must buy building insurance, which mortgage lenders typically require, to safeguard your property in case of unforeseen events.

And of course, do not forget moving costs.

The table below gives an estimate of some of these costs

Type of cost

Estimated cost

Conveyancer/ solicitor’s fees

£2,000

Mortgage arrangement fees

£1,000 to £2,000+

Mortgage booking fee

£100 to £200

Valuation fee

£150 to £800

Property survey

£400 to £1,500

Removals

£150 to £2,000+

Stamp duty

0% to 12% of home value

Source³ : Zoopla as of Oct-2023

Seek Professional Advice

Consulting with financial/mortgage advisors or mortgage brokers can offer personalized guidance tailored to your situation. They can provide insights on the best mortgage products and help navigate complex financial scenarios.

Conclusion

Preparing for a mortgage application involves several steps, from understanding your finances to gathering necessary documents and seeking expert advice. By following this checklist, UK homebuyers can enhance their readiness for a mortgage application, paving the way for a successful home purchase journey without any hindrances.

FAQs:

Q: How much deposit do I need for a mortgage in the UK?

A: Mortgage deposit requirements vary across lenders. But the amount of deposit you will need depends on the property price and your personal circumstances. First-time buyers typically need a minimum deposit of 5% but the average for a first time buyer is around 15% .Aiming for a larger deposit can improve your chances of securing a better interest rate.

Q: What are the additional costs of buying a house in the UK besides the purchase price?

A: Expect to pay Stamp Duty Land Tax, valuation fees, survey costs, legal fees, mortgage arrangement fees, and building insurance. Use cost calculators or consult a financial advisor for accurate estimates.

Q: Can I get a mortgage in the UK with bad credit?

A: It's challenging, but not impossible, especially with specialist lenders. Building your credit score, providing a large deposit, and explaining the circumstances behind your bad credit might help.

Q: What are the different types of mortgages available in the UK?

A: Fixed-rate mortgages offer predictable payments, while variable-rate mortgages offer flexibility but fluctuate with interest rates. Interest-only mortgages on the other hand require monthly interest repayments only with principal repayment at maturity.

Q: Do I need a mortgage broker in the UK?

A: Using a broker can save you time and money by comparing offers from different lenders and providing expert advice. However, they might charge fees, so compare options before committing.

Q: How long in advance should I start preparing for a mortgage application?

A: It's best to start at least 6-12 months in advance. This gives you enough time to save more funds, pay down debts, and gather all required paperwork. Starting early removes last-minute stresses.

Q: What are the alternatives if I can't get a traditional mortgage?

A: Options include guarantor mortgages (a third party guarantees your payments) or shared ownership schemes to buy a share in a property. These still require deposits but allow more access to homeownership.

Q: How much mortgage can I afford on my income?

A: Affordability criteria vary across lenders but they typically allow up to 4.5 times your annual income. Stricter affordability rules from some lenders might mean you may be eligible for smaller income multiples. It makes sense to scan the market to find a lender that offers a good combination of low first-time mortgage rates, a small mortgage deposit and a high income multiple.

The Pauzible Team consists of finance professionals and property market specialists dedicated to reinventing home ownership and BTL financing. With deep expertise across UK real estate and innovative financial products like Equity Partnership Agreements, we provide landlords and homeowners with the insights they need to unlock equity, navigate market volatility, and build sustainable wealth through property. Our mission is to make complex property finance simpler, quicker, and more accessible for everyone.

Ready to see what Pauzible could unlock?

Explore how accessing equity from your BTL property could support your business investment plans.

No obligation. Just a clear view of what might be possible.