A mortgage in principle (MIP) is a mortgage lender's confirmation as to how much they would be willing to lend to you based on the limited preliminary information you have provided them with about your finances. While not a guaranteed mortgage offer, an MIP carries significant weight.

08/04/2025By Pauzible Team · Editorial Team

What is a Mortgage in Principle?

A mortgage in principle (MIP) is a mortgage lender's confirmation as to how much they would be willing to lend to you based on the limited preliminary information you have provided them with about your finances. While not a guaranteed mortgage offer, an MIP carries significant weight. It tells estate agents and sellers that you are a serious buyer with financial credibility and the willingness to make your homeownership dream a reality by applying for and committing to the required mortgage. A MIP is sometimes also referred to as an “Agreement in Principle (AIP)”, “Decision in Principle (DIP)”, “Mortgage Promise” or “Lending Certificate”.

Why Get a Mortgage in Principle?

Imagine navigating the vast ocean of property listings without a clear sense of how much you can realistically afford to spend on the purchase of a new home. In this sense, a MIP can act as a financial compass, orienting you toward homes that are aligned with your borrowing potential. By obtaining this document before you even begin house hunting, you can streamline your search and focus your efforts on properties that are likely to be within your reach.

However, a MIP offers far more than just budgetary clarity. It positions you as a serious contender in the eyes of estate agents and sellers, giving you a competitive edge over buyers who do not have such a document. When you find that perfect property, a MIP can potentially expedite the mortgage application process, as you will have gathered much of the required information and documentation already.

A MIP can also be a useful negotiating tool. Armed with proof of your potential borrowing capacity, you can approach estate agents and sellers demonstrating your readiness to make a credible offer confidently and potentially secure a better purchase price.

How to Get a Mortgage in Principle

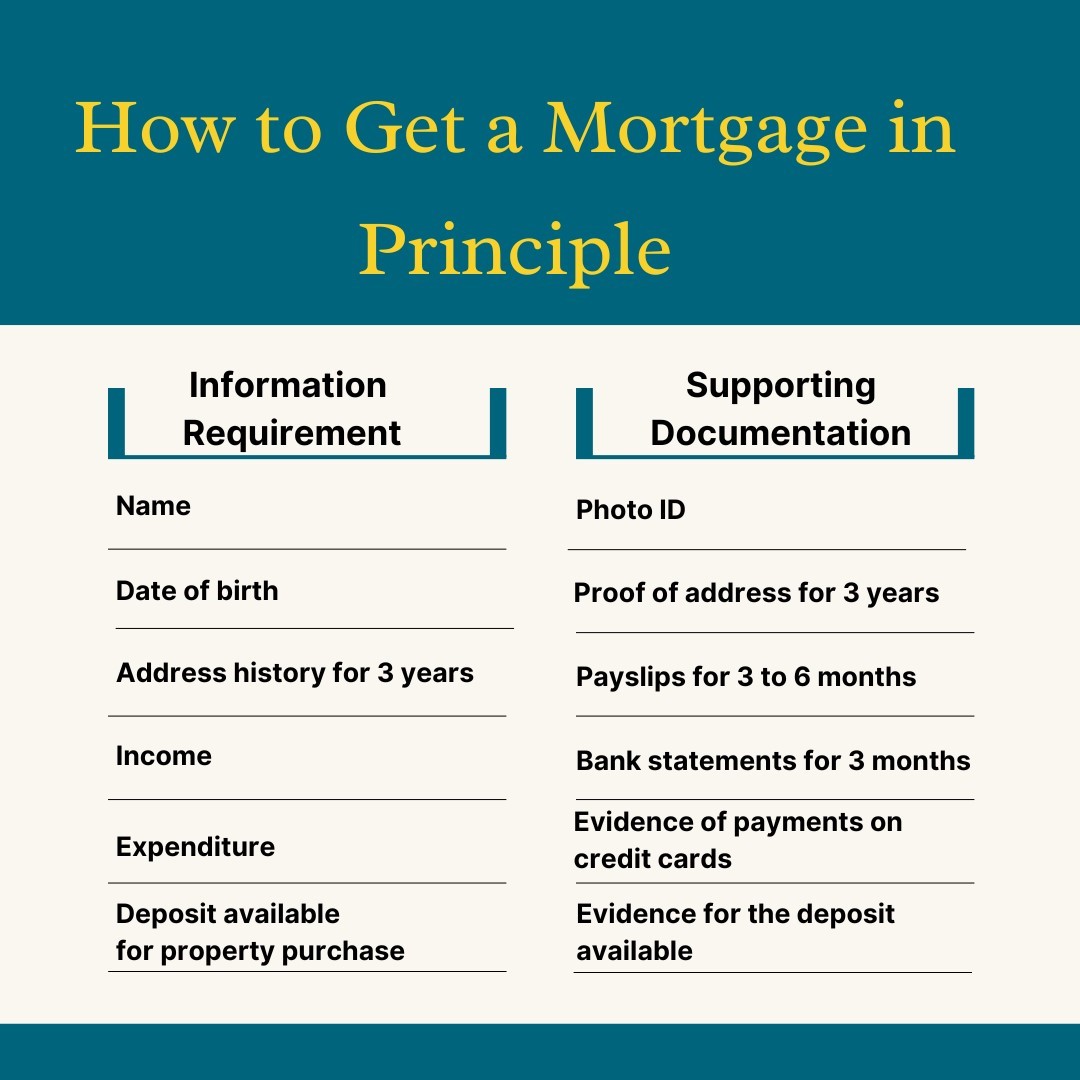

To obtain a MIP, you will need to apply to a mortgage lender either directly or through a mortgage broker. The application will require putting together a reasonable amount of information, including your (and any joint applicant’s):

Not all of the above documentation may be required by a lender considering your MIP application. However, providing it to a mortgage broker if you are applying for a MIP through one may still be a good idea. They tend to be experienced in such matters and may be able to check that there are no inconsistencies in your MIP application, for example. In any event, you will need the supporting documentation that you will have gathered when subsequently submitting a full mortgage application. Lenders will also carry out a credit check for MIP purposes.

Once you have put together the required information for a MIP application, it might be a good idea to analyse it, possibly with the help of a mortgage broker, before making the application. This will enable you to estimate how much you might be able to borrow and if there is something you could do to enhance your purchasing power, such as rationalising your expenditure and increasing your savings and deposit amount.

How Long Does a Mortgage in Principle Last?

A MIP is usually valid for 90 days. However, depending on the specific lender's policies, it could be for a shorter period. The validity period should normally be long enough for most prospective homebuyers to be able to find their ideal property and make an offer. However, if the MIP does run out before you have found your ideal home, there is no need to panic. You can easily reapply for a new one and ensure that you have a valid MIP again as you continue your property search.

Once you have made an offer to purchase a property and it has been accepted, the next stage will to submit a full mortgage application and obtain a formal mortgage offer. This will involve a more detailed examination of your finances, supporting documentation and credit profile by the lender, as well a valuation of the property. Assuming everything is satisfactory and that you receive the mortgage offer, you will then proceed to the conveyancing stage, including searches, exchange of contracts, completion and registration with the Land Registry.

The journey to homeownership is an adventure filled with challenges and rewards. By obtaining a mortgage in principle, you can equip yourself with a vital navigational tool, charting a clear course towards your dream destination. With careful preparation and proper guidance, you should be well on your way to anchoring at the shores of your ideal home.

FAQs:

Q. Is a mortgage in principle a guarantee of a mortgage offer?

A: No, a mortgage in principle is not a guarantee that you will get a mortgage offer. It is an initial indication from a lender as to how much they may be willing to lend to you based on a preliminary assessment of your finances. A formal mortgage application process will still need to be completed, and your income, outgoings and credit history, and the valuation of the property will need to be scrutinized in more detail before a formal mortgage offer is made by the lender.

Q. How long does a mortgage in principle last?

A: A mortgage in principle is typically valid for 90 days, although this depends on the specific lender. This timeframe should normally give you enough of a window to find a property and make an offer before the MIP expires. If it does expire, however, you can reapply for a new MIP and continue your property search.

Q. What documents do I need for a mortgage in principle?

A: To put together the information that you will need to apply for a mortgage in principle, you will need to consult the relevant supporting documentation, including, for example:

Photo ID

Proof of address for three years

Payslips for three to six months

Bank statements for three months

Evidence of payments on credit cards, hire purchase agreements and other loans

Evidence for the deposit and its source

Not all of the above documentation may be required by a lender. However, providing it to a mortgage broker if you are applying for a MIP through one may be a good idea. They tend to be experienced in such matters and may be able to check that there are no inconsistencies in your application, for example. In any event, you will need the supporting documentation when you subsequently make a full mortgage application.

Q. Can I get a mortgage in principle with poor credit?

A: It is possible to get a mortgage in principle with poor credit, but this will depend on the severity of your credit issues and the lender's criteria. A low credit score and missed payments on your record may limit the amount that a lender might be willing to lend, for example. It may be worth getting a mortgage broker’s advice and applying for a mortgage in principle through them if you have poor credit.

Q. How much can I borrow with a mortgage in principle?

A: The amount stated on your MIP will be based on how lenders assess your financial circumstances during an initial check based only on limited information and scrutiny. It is not a formal mortgage offer. The amount you can borrow for purchasing a property will ultimately depend on the lender’s detailed assessment of your full mortgage application, including income, outgoings, deposit, credit history and the value of the property, and supporting documentation. Typically, most lenders will cap the amount they will lend at 4 – 4.5 times your annual income, subject to affordability assessment.

About the author

Pauzible Team

Editorial Team

The Pauzible Team consists of finance professionals and property market specialists dedicated to reinventing home ownership and BTL financing. With deep expertise across UK real estate and innovative financial products like Equity Partnership Agreements, we provide landlords and homeowners with the insights they need to unlock equity, navigate market volatility, and build sustainable wealth through property. Our mission is to make complex property finance simpler, quicker, and more accessible for everyone.

Ready to see what Pauzible could unlock?

Explore how accessing equity from your BTL property could support your business investment plans.

No obligation. Just a clear view of what might be possible.