Understanding the Debt-to-Income Ratio (DTI) for Mortgages

Discover the importance of the Debt-to-Income (DTI) ratio in securing a mortgage. Learn how to calculate your DTI, understand lenders' expectations, and improve your ratio for better approval chances.

08/04/2025By Pauzible Team · Editorial Team

When you are considering applying for a mortgage, one of the key factors lenders look at is your Debt-to-Income (DTI) ratio. This ratio is your total monthly debt payments as a proportion of your gross monthly income expressed in percentage terms. It gives lenders an idea of how much of your income goes towards debt payments each month and helps them determine if you can comfortably afford to take on additional debt. A lower DTI ratio is generally preferred in mortgage lending as it indicates that you have adequate disposable income available to cover your mortgage payments. Understanding what the DTI ratio is and how it impacts your mortgage application is thus important for home buyers.

Calculating Your DTI Ratio

Calculating your DTI ratio is relatively straightforward. First, add up all your monthly debt payments. These include mortgage or rent payments, credit card bills, student loans, car loans and any other debt obligations. Then, add up your gross monthly income, including your salary, any rental income and income from any other regular sources. Once you have added up your total monthly debt payments and monthly income, divide your total debt figure by your total income figure. Then, multiply the resulting figure by 100. For example, if your total monthly debt payments amount to £800 and your gross monthly income is £3,000, your DTI ratio would be calculated as (800 / 3000) x 100 = 26.67%. Top of Form

The Ideal DTI for Mortgages

Most UK lenders will consider mortgage applicants with DTI ratios of about 40% or lower. This means that your total monthly debt payments, including your mortgage, should ideally not exceed around 40% of your gross monthly income. DTI ratios of 20% or lower are considered even more desirable. A lower DTI ratio suggests you have more room in your budget to afford your mortgage payments and other debt obligations comfortably.

Having a lower DTI ratio also improves your chances of qualifying for a mortgage with more favourable terms. With a lower DTI, you could receive lower interest rates and qualify for larger loan amounts. Mortgage lenders view borrowers with lower DTI ratios as less risky because they have demonstrated the ability to manage their debts responsibly. By keeping your DTI ratio low, you can increase your chances of securing a mortgage that fits within your budget. This helps you achieve your homeownership goals without overextending your finances.

Debt Considerations

When calculating DTI ratios, various types of debts are typically considered to provide a comprehensive picture of an individual's financial obligations. These debts include secured and unsecured loans, including mortgages, car loans, personal loans, credit card balances, student loans and other outstanding financial liabilities. Secured debts, such as mortgages and car loans, are tied to collateral, while unsecured debts, such as credit card balances and personal loans, do not require collateral. Including both types of debts in the DTI ratio calculation allows lenders to gauge the extent to which an individual's income is allocated to various types of financial obligations.

Understanding which debts are factored into the DTI ratio is important for borrowers seeking loans or credit. By accounting for a broad range of debts, lenders gain insights into an individual's overall debt burden and their ability to manage multiple financial commitments simultaneously. This assessment helps lenders make informed decisions regarding loan approvals, interest rates and borrowing limits.

Beyond the DTI Ratio

While the DTI ratio is crucial in mortgage applications, lenders also consider several other key aspects of an individual's financial profile. Their credit score holds significant weight in assessing a borrower's creditworthiness. A higher credit score indicates a history of responsible borrowing and timely payments. A lower credit score, on the other hand, might signal to the lender that the borrower might not be ready for homeownership at this point. Employment history is another important factor. Lenders typically prefer borrowers with stable employment and consistent income.

The amount of deposit offered by the borrower as part of their property purchase price also influences the lender's perception of risk. A larger deposit reduces the loan-to-value ratio and indicates a greater commitment to the property and potentially lower risk. A smaller deposit may require a lower DTI ratio to mitigate the lender's perception of risk. Financial stability also plays a crucial role. Lenders assess factors such as savings, investments and other assets. A borrower with substantial assets and a diversified investment portfolio is likely to be viewed more favourably. Individuals with limited financial reserves may need to maintain a lower DTI ratio to reassure lenders of their ability to handle mortgage payments in the event of unforeseen financial challenges.

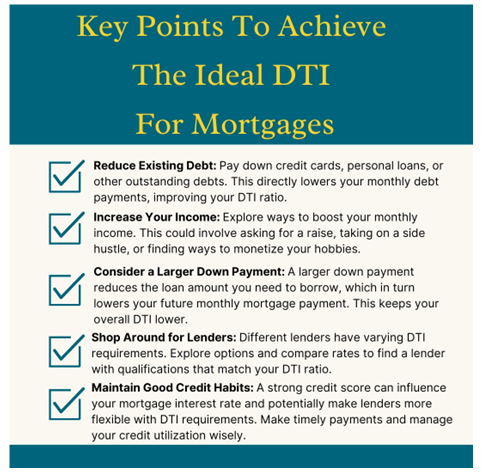

Improving Your DTI Ratio

Improving your DTI ratio can help significantly when applying for a mortgage. One strategy would be to reduce existing debt before seeking a mortgage. This can involve paying off outstanding credit card balances, consolidating high-interest debts into lower-rate loans or even negotiating with creditors for better repayment terms. Reducing your total debt can decrease your DTI ratio, which will benefit you when applying for a loan.

Top of Form

Increasing your income is another effective way to improve your DTI ratio. This can be achieved through various means. You can seek a higher-paying job, take on additional part-time work or explore alternative sources of income such as rental income. It is important to ensure that any additional income is stable and reliable.

Managing your finances carefully and budgeting effectively can help contribute to a healthier DTI ratio. You can start by tracking your expenses, prioritizing debt payments and avoiding unnecessary spending. Creating and sticking to a realistic budget can help you allocate more of your income towards debt repayment.

FAQs Section

Q. What is the DTI ratio and how does it impact mortgages?

A: The debt-to-income (DTI) ratio is a measure used by lenders to assess a borrower's ability to manage mortgage payments based on their income and existing debt obligations. The DTI ratio plays a crucial role in mortgage applications as it helps lenders determine the level of risk associated with lending to a particular individual. A higher DTI ratio suggests that a larger portion of the borrower's income is committed to debt repayments. A lower DTI ratio indicates that the borrower has more disposable income to cover mortgage payments, which may increase their chances of approval.

Q. What is a good DTI ratio for getting a mortgage?

A: Lenders generally prefer DTI ratios of about 40% or lower. DTI ratios of 20% or less are considered even more desirable. However, some lenders may accept higher DTI ratios depending on other factors such as your credit score, employment history and overall financial stability. Aiming for a low DTI ratio is important to show lenders that you possess enough income to manage your mortgage payments and other financial commitments comfortably.

Q. How can I calculate my DTI ratio?

A: First, add up all your monthly debt payments. These include mortgage or rent payments, credit card bills, student loans, car loans and any other debt obligations. Then, add up your gross monthly income, including salary, rental income and income from any other regular sources. Once you have added up your total monthly debt payments and monthly income, divide your total debt figure by your total income figure. Multiply the result by 100. For example, if your total monthly debt payments amount to £800 and your gross monthly income is £3,000, your DTI ratio would be calculated as (800 / 3000) x 100 = 26.67%.

Q. What types of debt are considered when calculating DTI ratio for a mortgage?

A: When calculating the DTI ratio for a mortgage application, various types of debts are considered. These typically include rent and mortgage payments, and any other recurring monthly debt obligations, such as credit card payments, loan repayments, car finance and personal loans.

Q. Can I still get a mortgage with a high DTI ratio?

A: Getting a mortgage with a high DTI ratio is possible, but may be more challenging. While lenders generally prefer lower DTI ratios, they may consider other factors such as your credit score, employment history and overall financial stability when assessing mortgage applications. Having a strong credit history, stable income and a sizable deposit may increase your chances of getting approved for a mortgage. Some lenders may offer specialized mortgage products tailored to borrowers with higher DTI ratios. These types of loan may come with higher interest rates or stricter lending criteria.

About the author

Pauzible Team

Editorial Team

The Pauzible Team consists of finance professionals and property market specialists dedicated to reinventing home ownership and BTL financing. With deep expertise across UK real estate and innovative financial products like Equity Partnership Agreements, we provide landlords and homeowners with the insights they need to unlock equity, navigate market volatility, and build sustainable wealth through property. Our mission is to make complex property finance simpler, quicker, and more accessible for everyone.

Ready to see what Pauzible could unlock?

Explore how accessing equity from your BTL property could support your business investment plans.

No obligation. Just a clear view of what might be possible.