Why use home equity? Reasons/benefits of using home equity

It's a powerful financial asset that can be leveraged for various purposes, highlighting the home equity loan benefits. Understanding why and how to use home equity, alongside acknowledging its potential pitfalls, is crucial for any homeowner looking to make informed decisions about their property and finances.

08/04/2025By Pauzible Team · Editorial Team

What is Home Equity?

Home equity represents the part of your home that you own, calculated as the difference between the property's current market value and the amount still owed on the mortgage. It's a powerful financial asset that can be leveraged for various purposes, highlighting the home equity loan benefits. Understanding why and how to use home equity, alongside acknowledging its potential pitfalls, is crucial for any homeowner looking to make informed decisions about their property and finances. To illustrate, if your home is valued at £300,000 and you owe £150,000 on your mortgage, your home equity amounts to £150,000. This equity accumulates over time as you pay your mortgage and the property's value appreciates, signifying the benefits of using home equity in the UK.

Reasons and Benefits to Use Home Equity

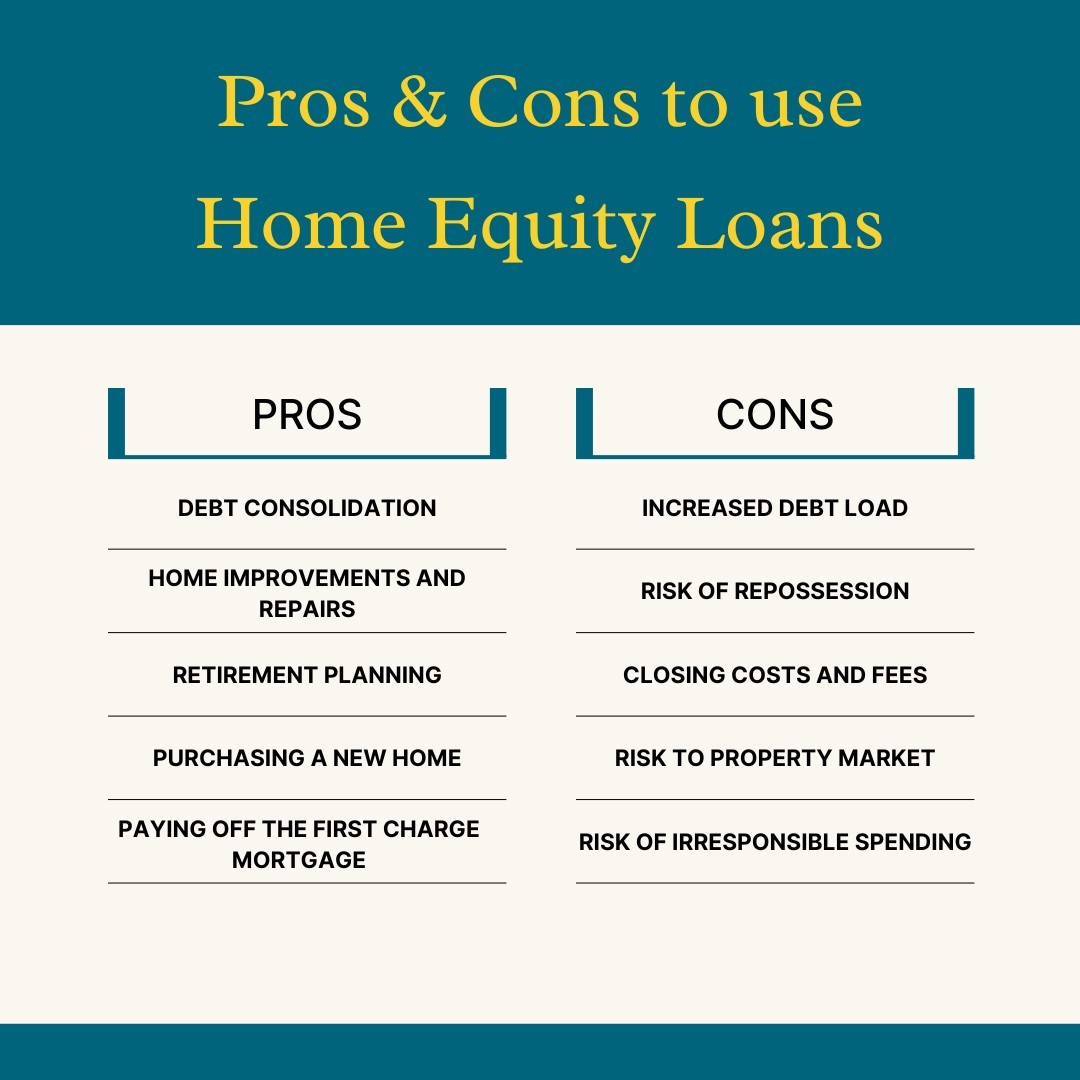

1. Debt Consolidation: If you have multiple high-interest debts, you can use your home equity to consolidate them into a single, lower-interest loan. Generally, credit card APRs can range from 15% to 25%, whereas home equity loans offer rates from 3% to 12%, depending on creditworthiness and market conditions. By consolidating debt through home equity, you can save up to 10-15% in interest charges annually, a perfect model of debt consolidation with home equity loan.

2. Home Improvements and Repairs: Investing in your home can make it more comfortable, aesthetically pleasing, and energy-efficient. This can increase the value of your home, improve your living conditions, and save you money on utility bills in the long run (depending on what you spend the improvements on). The Telegraph1 states that around 23% of UK homeowners unlock equity to improve their homes, one of the key reasons to release home equity in the UK.

3. Funding Education: Using your home equity to finance education can be a wise investment in your or your family's future. This can help you cover the costs of tuition, textbooks, and other educational expenses at a lower interest rate than other types of loans.

4. Emergency Fund: Home equity can be valuable for unexpected expenses, such as medical bills or sudden job loss. By using your equity as a backup fund, you can avoid taking out high-interest loans or depleting your savings. Using your home equity for emergencies can help you avoid personal loans or credit card borrowing, which can come with high APRs ranging from 6% to 36%, according to Nerdwallet2, resulting in significant interest expenses.

5. Investment Opportunities: Using your home equity to invest in other properties, stocks, or business ventures can increase your wealth over time. This is a smart way to diversify your investment portfolio, earn a higher return on your money, or invest with home equity.

6. Retirement Planning: If you have limited retirement savings, using your home equity to supplement your income can be an intelligent way to ensure a comfortable retirement. You can receive a steady income stream by tapping into your equity in your retirement years, which can improve your lifestyle without taking additional debt.

7. Purchasing a New Home: Using your home equity as a down payment for a new property can be a smart way to move into a larger or more expensive home. Alternatively, you can use your equity to downsize and pocket the difference, saving money on housing expenses, which is a strategic move to buy a second property with home equity.

8. Paying Off the Mortgage: By using your equity to pay off your first charge mortgage early, you can save thousands of dollars in interest payments over the life of your loan. This can also free up your monthly budget for other expenses or savings goals.

A Representative Example

Consider Jane, who owns a home valued at £250,000 with a remaining mortgage of £100,000, giving her £150,000 in equity. She decides to take out a £30,000 home equity loan to renovate her kitchen, believing it will increase her home's value. While the renovation boosts her property's market value to £270,000, Jane now has a new loan to repay on top of her mortgage. If Jane's financial situation changes unexpectedly, she might find it challenging to manage the additional loan, highlighting the importance of carefully considering one's ability to repay before leveraging home equity.

Potential Pitfalls

While the benefits are compelling, there are also risks involved in using home equity:

Home equity can be a great way to access cash for expenses such as home renovations or education or to consolidate debt, as mentioned above. However, it's essential to consider the risks involved before deciding.

Firstly, if you borrow against your home equity, it can increase your debt load, which could cause financial strain if not appropriately managed. It's essential to have a clear plan for how to repay the loan and ensure you can make the monthly payments.

Secondly, there is a risk of repossession if you can't make the payments on a home equity loan. This means you could lose your home if you default on the loan.

Thirdly, equity loans come with closing costs and fees, which can reduce the amount of money you gain. Make sure you understand all of the costs involved before making a decision.

Fourthly, using home equity now means less wealth in your estate, which could affect your retirement lifestyle or your ability to move homes. Considering how using your home equity will impact your plans now is essential.

Fifthly, there is a market risk involved with using home equity. If the property market declines, you could owe more than your home is worth, a situation known as being "underwater" on your mortgage. This could make it challenging to sell your home in the future.

Sixthly, the money used to repay a home equity loan could have generated higher returns if invested elsewhere. It's essential to consider the opportunity cost of using your home equity.

Lastly, easy access to home equity can lead to spending on non-essential items, which can put homeowners at financial risk. Using home equity responsibly and having a clear plan for using the funds is essential.

Conclusion

Using home equity offers a range of benefits, from improving your current home to providing financial security. However, weighing these advantages against the potential risks and costs is crucial. Homeowners should consider their long-term financial goals, the stability of their income, and the current market conditions before tapping into their home equity. Consulting with a financial advisor can provide personalized insights and help you navigate the decision-making process more effectively.

FAQs:

Q: How do I know how much equity I currently have in my home?

A: You can estimate your home equity by subtracting your outstanding mortgage balance from your best estimate of the current market value of your home. Online calculators1 can also help determine an estimate.

Q: What are the most common reasons people use home equity?

A: People commonly use home equity for major expenses such as home renovations, education costs, debt consolidation, investing, or as an emergency fund. It's often seen as a cost-effective way to borrow since it typically has lower interest rates than other credit forms.

Q: Can I use home equity to consolidate high-interest debt?

A: Consolidating high-interest debt, such as credit card balances or personal loans, is an everyday use of home equity. Doing so can lower your monthly payments and total interest costs due to typically lower home equity loan rates.

Q: Is it a good idea to use home equity to invest?

A: Using home equity to invest can be advantageous if the investment yields a higher return than the cost of borrowing. However, it carries risks, as the investment performance isn't guaranteed and should be carefully considered within your overall financial strategy.

Q: What are the risks and benefits of using home equity to improve my lifestyle?

A: Benefits include access to funds for large purchases or lifestyle enhancements, potentially at lower interest rates. Risks involve the possibility of repossession if one cannot keep up with repayments and the reduction of the equity you have in your home, which could affect future financial options.

Q: Are there any tax implications of using home equity?

A: The tax implications of using home equity can vary. Sometimes, the interest on home equity loans may be tax-deductible. It's essential to consult with a tax professional regarding current tax laws and how they apply to your situation.

Q: What happens to home equity when a property owner dies?

A: When a homeowner dies, any equity they have in their home may pass to heirs as part of the probate process. The inheritance of equity will depend on whether the owner had a will stipulating distributions or other estate planning measures.

The Pauzible Team consists of finance professionals and property market specialists dedicated to reinventing home ownership and BTL financing. With deep expertise across UK real estate and innovative financial products like Equity Partnership Agreements, we provide landlords and homeowners with the insights they need to unlock equity, navigate market volatility, and build sustainable wealth through property. Our mission is to make complex property finance simpler, quicker, and more accessible for everyone.

Ready to see what Pauzible could unlock?

Explore how accessing equity from your BTL property could support your business investment plans.

No obligation. Just a clear view of what might be possible.