Fixed-rate mortgages are a popular option, where the interest rate stays the same for a set period, providing stability and predictability in the constantly changing finance space. In this article, we will explore the details of three different fixed-rate mortgage options, 2-year, 5-year, and 10-year, to help you understand their advantages and disadvantages and, hopefully, allow you to make an informed decision.

08/04/2025By Pauzible Team · Editorial Team

A Guide to 2, 5, and 10-Year Terms

When applying for a mortgage, selecting the appropriate type of interest rate is just as important as choosing the property itself. Fixed-rate mortgages are a popular option, where the interest rate stays the same for a set period, providing stability and predictability in the constantly changing finance space. In this article, we will explore the details of three different fixed-rate mortgage options, 2-year, 5-year, and 10-year, to help you understand their advantages and disadvantages and, hopefully, allow you to make an informed decision.

Moreover, the choice between shorter or longer-term fixed rates can vary based on market conditions and individual financial situations. Potential homeowners must consider their financial stability, risk tolerance, and future plans when deciding on the mortgage term. Before deciding, it's essential to consider the advantages and disadvantages of fixed-rate mortgages.

What Are Fixed-Rate Mortgages?

A fixed-rate mortgage is where your interest rate is locked in for a set period. This means your monthly mortgage payments will remain the same during this period, regardless of any potential interest rate increases or decreases. This is a popular option for those who want to have certainty and stability in their budgeting and financial planning amidst the ever-changing cost of living.

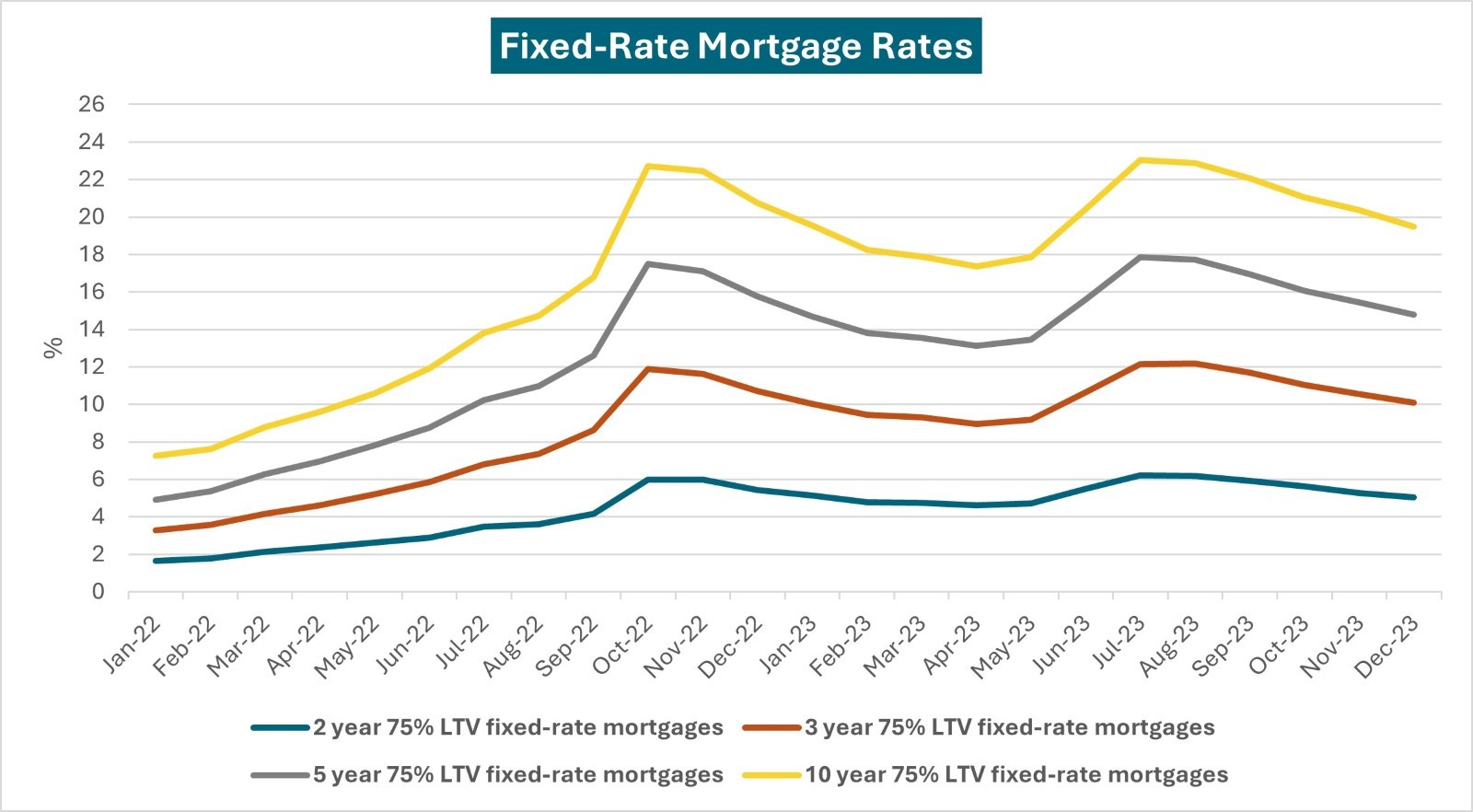

Source¹ : Bank of England

2-Year Fixed-Rate Mortgages

Pros:

Shorter mortgage terms often have lower interest rates and provide flexibility for changes in financial situations, making them ideal for first-time homeowners to adjust to fixed monthly payments. This is also quite beneficial for those who anticipate changes in their financial situation, such as a potential move or change in income, or who plan to remortgage in the near future for better terms.

For first-time homeowners, this option can alleviate any stresses that come with the commitment of paying a mortgage for the first time.

Cons:

Once the 2-year term ends, the mortgage often reverts to the lender's standard variable rate (SVR), which can be higher than you initially signed up for. This change can lead to significant increases in monthly payments, requiring financial readiness for such adjustments. This option can create uncertainties for those still determining where their financial situation will be at the end of the 2-year term.

A shorter fixed term means you may need to remortgage more frequently to avoid higher SVR rates. This process can incur additional costs, provision of documentation and requires continuous attention to mortgage market changes, which can be inconvenient and time-consuming. This option may also not remain profitable for buy-to-let mortgages when the monthly mortgage payments become greater than the rental income after the two-year period.

5-Year Fixed-Rate Mortgages

Pros:

A 5-year fixed-rate mortgage locks in your interest rate for an extended period (5 years), providing consistent and predictable monthly payments. This stability is particularly beneficial for budgeting and financial planning, as it shields you from potential interest rate hikes during the term. It's ideal for those who value certainty in their financial outgoings. This option can allow you to build up savings with the difference of what you would've paid if adhering to the lender's SVR.

With the economic climate often fluctuating- as we have experienced in the past years- a 5-year fixed rate offers protection against rising interest rates. If the Bank of England raises rates, your mortgage payments won't be affected for the term. This can be particularly advantageous in an environment where rates are expected to rise, as it can lead to substantial savings over the 5-year period compared to a variable rate mortgage. This is particularly popular amongst those who value extra monthly savings or have some breathing space with payments.

Cons:

This type of mortgage binds you to a fixed rate for five years, and if you wish to switch mortgages or repay early, you may face substantial early repayment charges (ERCs). This can be particularly restrictive if circumstances change unexpectedly, such as wanting to move house or accessing better mortgage deals that emerge over time. Such fees can make it costly to adapt your mortgage to changing personal or financial situations during the 5-year term.

10-Year Fixed-Rate Mortgages

Pros:

A 10-year fixed mortgage secures your interest rate for a decade, providing unparalleled protection against potential interest rate increases. This is particularly beneficial for those worried about the changing economic climate, allowing them ease of mind.

This type of mortgage offers a long horizon for financial planning, allowing homeowners to budget and plan their finances with certainty. Knowing your mortgage payments will remain consistent for ten years can be extremely valuable for long-term financial stability and peace of mind.

Cons:

Fixed-rate mortgages typically offer higher interest rates than other types of mortgages. This is because the interest rate remains the same throughout the mortgage term, providing more stability for the lender. However, fixed-rate mortgages also come with a decade-long lock-in commitment that can be restrictive if circumstances change. If you need to sell your home or refinance your mortgage before the end of the term, you may be subject to penalties or fees.

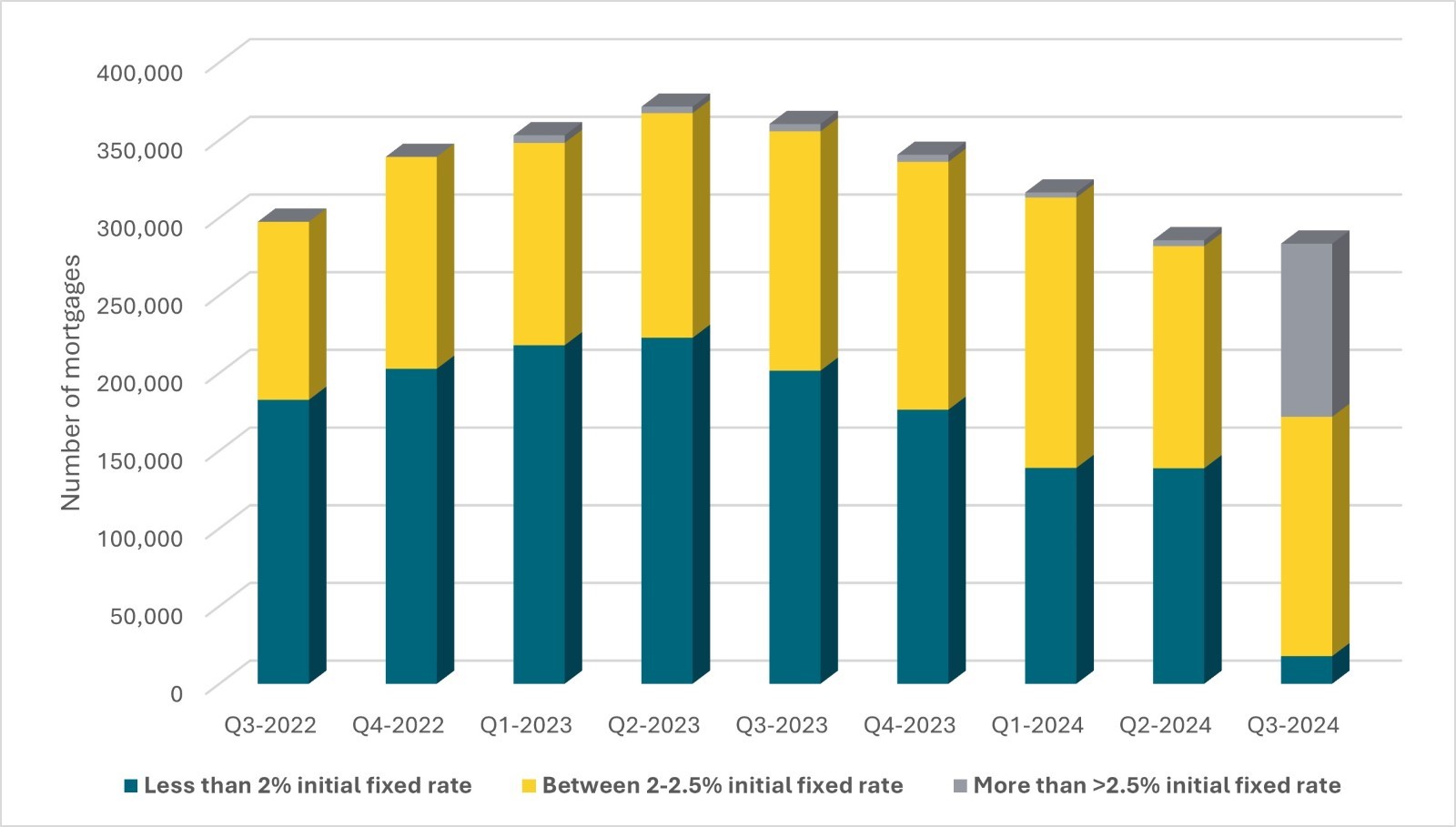

Number of fixed rate mortgage loans coming up for renewal in the United Kingdom (UK) from 1st quarter 2022 to 3rd quarter 2024, by initial effective interest rate

Source² : ONS

See table below for a quick summary of the benefits for different fixed rate maturities

2 year

5 year

10 year

Flexibility

✓✓✓

✓✓

✓

Peace of mind

✓

✓✓

✓✓✓

ERC (early repayment charge)

✓✓✓

✓✓

✓✓

Remortgage costs

✓✓✓

✓✓

✓✓

Lowest mortgage rate

✓✓✓

✓✓

✓

Tips for Choosing the Right Fixed-Rate Mortgage

Assess Your Financial Stability: Consider your long-term income security and possible life changes. Also, analyse your current expenses and ability to make mortgage payments if your income were to decrease.

Market Trends Analysis: Keep an eye on interest rate trends and economic forecasts. Check with financial advisors for opinions on where rates could go in the next 5-10 years.

Flexibility vs. Stability: Strike a balance between the need for stability and the potential need for flexibility. Discuss different fixed-rate term options with your mortgage advisor and how refinancing may impact your situation.

Exit Strategy: Understand the penalties and processes involved in switching or paying off your mortgage early. Ask lenders to clearly explain prepayment penalties and how you can avoid or minimize them if you need to refinance or move.

When it comes to choosing a mortgage plan, you have several options to consider. You can opt for the lower rates and flexibility of a 2-year fixed mortgage, a balanced approach with a 5-year term, or the long-term security of a 10-year fix. It is essential to weigh these options carefully. An independent financial advisor or mortgage broker can help assess your risk appetite, interest rate and future economic and property market outlook and recommend a solution that suits your circumstances.

FAQs:

Q: What is the difference between a fixed and variable rate mortgage?

A: A fixed rate mortgage locks in a set interest rate for the term chosen (2, 5, or 10 years typically). This provides payment predictability. A variable rate mortgage fluctuates based on the Bank of England and market conditions, so payments can go up or down.

Q: Are there fees for paying off my fixed-rate mortgage early?

A: Yes, most lenders charge early repayment charges (ERCs) if you pay off a fixed-rate mortgage before the term ends. ERCs can be expensive, so make sure to understand these before committing.

Q: Should I choose the longest mortgage term possible?

A: Not necessarily. While 10-year fixed terms offer exceptional stability, they also charge higher interest rates and substantial ERCs. Consider your budget and plans for the future before opting for the longest available term.

Q: Can I switch between fixed rate terms?

A: Yes, you can usually switch between fixed rate mortgage terms at the end of your existing fixed rate deal without incurring an early repayment charge. This would incur new arrangement fees but allows you to re-assess the best option.

Q: What are the early repayment charges for a 5 year fix in the UK?

A: Early repayment charges vary across lenders and fixed rate terms. Speak to your lender or check your mortgage document.

The Pauzible Team consists of finance professionals and property market specialists dedicated to reinventing home ownership and BTL financing. With deep expertise across UK real estate and innovative financial products like Equity Partnership Agreements, we provide landlords and homeowners with the insights they need to unlock equity, navigate market volatility, and build sustainable wealth through property. Our mission is to make complex property finance simpler, quicker, and more accessible for everyone.

Ready to see what Pauzible could unlock?

Explore how accessing equity from your BTL property could support your business investment plans.

No obligation. Just a clear view of what might be possible.