A Mortgage Indemnity Guarantee (MIG) is a type of insurance policy that lenders require borrowers to take out in certain circumstances. Typically, it is associated with mortgages with loan-to-value (LTV) ratios of greater than 75% where lenders are seeking additional security.

08/04/2025By Pauzible Team · Editorial Team

A Mortgage Indemnity Guarantee (MIG) is a type of insurance policy that lenders require borrowers to take out in certain circumstances. Typically, it is associated with mortgages with loan-to-value (LTV) ratios of greater than 75% where lenders are seeking additional security. It protects the lender against potential losses if a borrower defaults on their mortgage payments and the subsequent sale of the property repossessed by the lender after due process fails to cover the outstanding loan amount in full.

It is important to understand that a MIG is not an insurance policy for the borrower but is specifically designed to protect the lender's interests. Although the lender benefits from the cover, the borrower typically bears the cost of the MIG.

How MIGs Work:

The mechanics of a MIG are relatively straightforward. If a borrower defaults on their mortgage payments, the lender can initiate proceedings to repossess the property and exercise its power of sale in an attempt to recover the outstanding loan amount. If the sale proceeds from the repossessed property are insufficient to cover the full amount, the lender can make a claim on the MIG to recover the shortfall.

For example, consider a situation where a borrower has an outstanding mortgage of £200,000 and has defaulted. Assume that subsequently the property is repossessed by the lender and sold after due process for £180,000. Under this scenario, the lender is faced with a loss or shortfall of £20,000. They can claim this shortfall from the insurer under the MIG policy.

However, it is important to bear in mind that the borrower is still personally liable for the lender’s shortfall under the terms of the mortgage agreement. Since the insurer has the right of subrogation under the MIG, any shortfall recovered from the borrower belongs to the insurer. The insurer, or the lender on the insurer’s behalf, can take action against the borrower to recover the shortfall if the borrower does not repay it voluntarily.

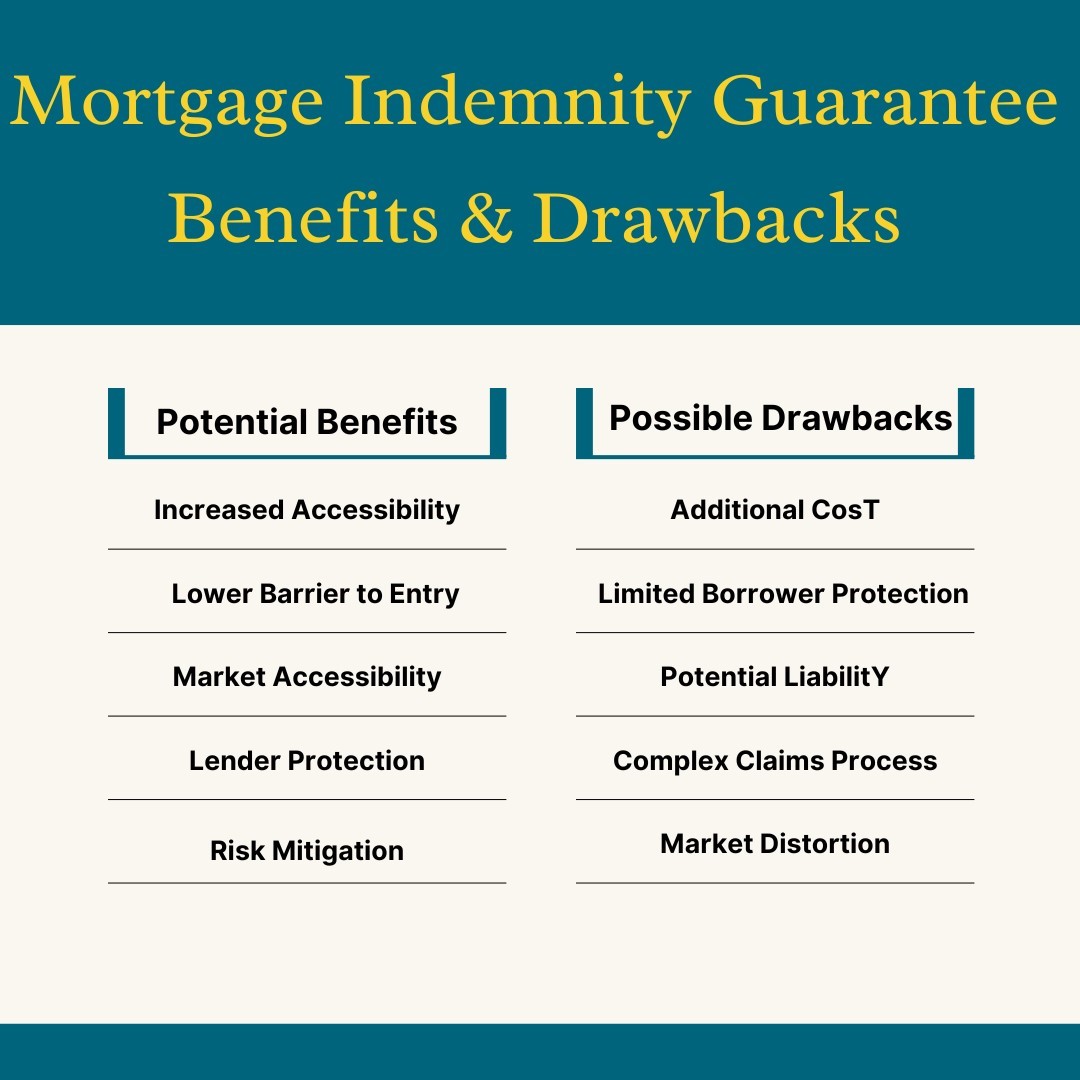

Benefits and Drawbacks:

From a borrower's perspective, MIGs can be both beneficial and disadvantageous.

On the positive side, they can open up homeownership opportunities to those with limited deposits who would not otherwise qualify for high LTV mortgages based on lenders’ affordability assessments. By allowing such borrowers to secure mortgages, MIGs can make the property market more accessible.

However, MIGs also come with drawbacks. They represent an additional cost that typically borrowers must bear, which can increase the expense of obtaining a mortgage. Furthermore, while MIGs protect lenders, they do not offer protection to borrowers. Indeed, if the MIG policy pays out a loan shortfall to the lender after the latter has repossessed the property and exercised its power of sale, the insurer, with the right of subrogation, can still seek to reclaim the shortfall amount from the borrower.

When are MIGs Used?

Lenders might require MIGs when the LTV ratio, which is the mortgage loan amount as a percentage of the value of the mortgaged property, exceeds a certain threshold. Usually, this threshold tends to be 75%, meaning borrowers seeking mortgages with an LTV of greater than 75% might be required to obtain MIGs. However, as the mortgage market has evolved, some lenders have raised this threshold to 80% or 85%, while others have pushed it even higher, up to 90% or 95% LTV. Such flexibility in LTV requirements can be attributed to factors such as property market conditions, competition among lenders and lenders' risk appetite.

Alternatives to MIGs:

While MIGs can be a valuable tool for enabling homeownership, borrowers might also want to explore other options.

One potential alternative is to save for a larger deposit, which can lower the LTV ratio and eliminate the need for a MIG. For instance, if a borrower can, say, save enough to be able to put down a 25% deposit, they might, subject to the lender’s affordability assessment, not be required to obtain a MIG at all, as 75% LTV would be below the usual MIG threshold.

Another option could be to find a lender who, subject to their affordability assessment of the borrower, is prepared to offer a loan with an LTV of greater than 75% without requiring a MIG.

Yet another option for some borrowers might be to find a guarantor for their mortgage payments. Under such an arrangement, a third party guarantor, such as a close family member, agrees to cover the mortgage payments if the borrower cannot. Guarantors would need to meet the lender’s affordability criteria and enter into a formal guarantee agreement. This can provide lenders with an additional layer of security, potentially negating the need for a MIG.

Cost and Considerations:

The cost of a MIG can vary depending on the lender, value of the property and specific loan terms. However, industry estimates suggest that the average cost can, broadly, range between 6% and 8% of the loan amount above the 75% LTV threshold.

Let us suppose, for example, that a borrower can secure an 85% LTV mortgage with a MIG to purchase a property for £200,000. In this situation, their deposit would be £30,000, or 15% of the £200,000 purchase price. The mortgage loan amount would be £170,000, or 85% of the £200,000 purchase price.

Let us suppose further that the cost of the MIG would be 7% of the LTV above the 75% threshold. The 85% LTV loan amount is £170,000. At 75% LTV, the loan amount would have been £150,000, or 75% of the £200,000 purchase price. The difference between the 85% LTV loan amount of £170,000 and the 75% LTV loan amount of £150,000 is £20,000, i.e. £170,000 minus £150,000. 7% of the difference of £20,000 would be £1,400, or the MIG cost.

Sometimes, lenders may allow borrowers to add the MIG premium to the mortgage loan amount at the outset rather than requiring an upfront lump sum fee payment. While this can make the upfront costs more manageable, it also means that the borrower will be paying interest on the MIG premium over the life of the mortgage.

For borrowers considering a MIG, it is important to weigh the costs and potential benefits taking into account their financial circumstances. Consulting with a mortgage advisor can provide valuable guidance in understanding the full implications of a MIG and possible alternatives tailored to the borrower's unique situation.

FAQs:

Q. What is a mortgage indemnity guarantee (MIG)?

A: A MIG is an insurance policy designed to protect lenders against potential losses or shortfalls if a borrower defaults on their mortgage payments and the subsequent sale of the property repossessed by the lender after due process fails to recover the outstanding loan amount in full.

Q. Who pays for a mortgage indemnity guarantee?

A: While the MIG policy benefits the lender, the borrower usually bears the cost. This can take the form of an upfront fee or added to the mortgage balance.

Q. When might a lender require a MIG?

A: Lenders may require a MIG when the loan-to-value (LTV) ratio of a mortgage is above a certain threshold, traditionally around 75%. However, some lenders may apply a higher threshold before requiring a MIG.

Q. Are there advantages to using a MIG?

A: The primary advantage for borrowers is the potential to access higher loan-to-value mortgages, meaning that they can, subject to the affordability assessment by the lender, potentially purchase a home with a smaller deposit.

Q. Are there disadvantages to MIGs?

A: The borrower incurs an additional cost for a MIG, which does not provide them with any protection. Furthermore, if the insurer pays out a claim to the lender, the borrower can be pursued by the insurer to recover this amount.

References:

1. What is a Mortgage Indemnity Guarantee | Mortgagerequired.com

About the author

Pauzible Team

Editorial Team

The Pauzible Team consists of finance professionals and property market specialists dedicated to reinventing home ownership and BTL financing. With deep expertise across UK real estate and innovative financial products like Equity Partnership Agreements, we provide landlords and homeowners with the insights they need to unlock equity, navigate market volatility, and build sustainable wealth through property. Our mission is to make complex property finance simpler, quicker, and more accessible for everyone.

Ready to see what Pauzible could unlock?

Explore how accessing equity from your BTL property could support your business investment plans.

No obligation. Just a clear view of what might be possible.