Fractional Selling: A Real Solution to the Mortgage Rate Crisis Facing UK Homeowners

The housing market has always been a subject of debate in the UK, given its historic importance to both personal wealth and the nation's economy. The current mortgage rate crisis, caused by the drastic rise in UK mortgage rates since December 2021, has plunged many homeowners into a sea of uncertainty and stress.

08/04/2025By Rajesh Pai · Co-Founder

The housing market has always been a subject of debate in the UK, given its historic importance to both personal wealth and the nation's economy. The current mortgage rate crisis, caused by the drastic rise in UK mortgage rates since December 2021, has plunged many homeowners into a sea of uncertainty and stress.

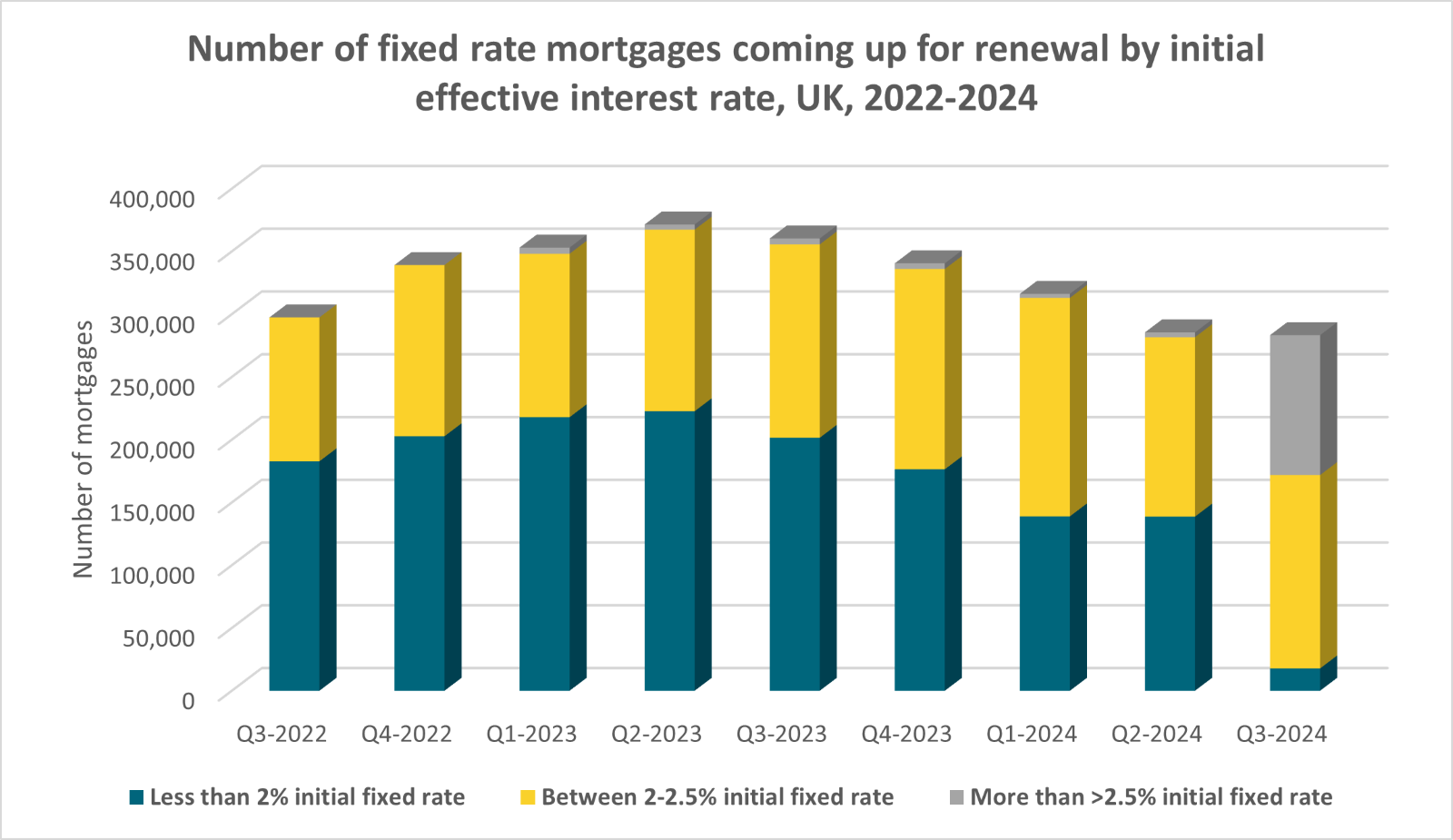

With almost two million UK homeowners on the brink of facing a significant increase in their cost of living due to a shift from previously low to sharply higher mortgage rates, the scenario looks grim. Data from the Office for National Statistics (ONS)1 reveal that a vast majority of borrowers coming to the end of their fixed rate mortgages in the first half of 2024 were on annual fixed mortgage rates of 2.5% or lower. With new rates likely to be much higher, the strain on households is intense. Monthly interest payments could potentially triple, further compounding the financial stress caused by the high inflation rate.

Source: ONS¹

The UK Government Solution

The government announced a Mortgage Charter, a laudable move that ensures no repossession for a year. Yet, this is a mere band-aid on a gushing wound. The root problem is expected to persist beyond a year, making it imperative for homeowners to look for long-term solutions, especially as mortgage rates which have been artificially low for almost a decade are now moving towards normalisation at a much higher level. While cutting discretionary expenses or seeking help from family might be potential short-term solutions, borrowing more to pay current interest is a trap homeowners should avoid. After all, if current mortgage payments are a challenge, resorting to even higher-cost debt to meet these current payments does not seem financially prudent.

Better Alternatives

But every cloud has a silver lining. The ending of the same low interest rate regime that caused the mortgage crisis also, in many cases, considerably augmented property values in the UK over more than a decade. Consequently, many homeowners now find themselves sitting on significant wealth in the form of home equity. This untapped resource provides for a unique solution: fractional selling.

By selling only a fraction of their home, homeowners can access their home equity to bridge financial gaps. For instance, assuming a 50% loan-to-value (LTV) mortgage, additional interest payments due to interest rate rises could equate to roughly about 1.5% of a property's value. By selling about 15% of their property, however, homeowners could secure their financial situation for an extended period. What's more, this approach doesn't saddle them with additional interest payments or rent payments (on the portion of the home equity they have sold) or unexpected rate hikes. Moreover, maintaining 85% ownership ensures that, should their financial situation improve, homeowners have the option to repurchase the fractional ownership they sold. This strategy provides clear benefits over the traditional route of downsizing or renting.

In essence, homeowners can reduce their mortgage burden without having to downsize. In a landscape of high interest rates, compared to an extended low rate environment previously, divesting fractional equity is a prudent and efficient alternative to accumulating more debt.

Platforms like Pauzible are pioneering such solutions, providing homeowners with new options during these challenging times. As homeowners navigate these difficult times, it is important to consider the new solutions available, focusing on those that ensure financial security without compromising ownership of their homes.

Pauzible: A Bridge Over Troubled Waters for UK Homeowners

Amidst the turbulence of the current mortgage rate landscape, Pauzible offers an innovative and timely solution. At its core, Pauzible understands the emotional and financial value of a home for a homeowner. Pauzible’s approach goes beyond traditional financial solutions by directly addressing the immediate pain points homeowners face in these times of higher mortgage rates.

A crucial aspect of Pauzible's offering is its ability to make monthly payments to homeowners that effectively neutralise the increase in mortgage costs. For homeowners shifting from low mortgage rates to sharply higher ones, this feature is nothing short of a lifeline. Pauzible ensures that, for up to five years, homeowners will continue to make payments equivalent to their earlier, lower rates. This stability is a godsend, providing families ample time — a half-decade, to be precise — to recalibrate their financial strategies. For those on interest-only mortgages, such as buy to let landlords, the jump in monthly payments is even starker and they would benefit from Pauzible’s BTL solution.

Long term solution, not a short-term fix

This five-year period isn’t just an arbitrary timeline. In an inflationary environment, it provides a reasonable window for property prices to rebound. There's also a good chance for mortgage rates to stabilise and for household incomes to see an uptick. It also gives homeowners the breathing space to consider other avenues, such as downsizing or remortgaging, but at a time of their choosing rather than resorting to selling in a rushed, crisis-driven scenario when house prices are already under pressure.

But Pauzible's commitment to homeowners goes even beyond this five-year window. Recognising the potential for longer term growth in property values and the importance of homeownership, Pauzible offers the homeowner the option to buy back its share of the homeowner’s equity for a period of up to 10 years. This means that the dream of reclaiming full ownership remains within reach, without adding any significant financial burden.

Conclusion

The beauty of Pauzible’s solution lies in its simplicity and its duration. It doesn’t just offer a quick fix, it provides homeowners with a robust, decade-long strategy to navigate the current crisis. While doing so, Pauzible not only preserves the homeowner's ability to remain in their beloved homes, but also ensures peace of mind. In an era where homes are more than just bricks and mortar, but spaces full of memories, safety and comfort, Pauzible's offerings are not just financially sensible, but also emotionally considerate.

Rajesh Pai, Head of Finance, Pauzible, says “For homeowners caught in the storm of high mortgage rates and high cost of living due to high inflation rates, Pauzible offers a powerful alternative solution. By enabling fractional selling of their property, they can continue to live in their cherished home exactly as before without having to make increased mortgage payments for several years or taking on further debt in other forms, such as high cost second charge mortgages.”

For those caught in the whirlwind of rising mortgage payments, Pauzible emerges as a beacon of hope, guiding homeowners to safer shores while ensuring they continue to live in the homes they so cherish and love.

FAQs:

Q: What is fractional selling?

A: Fractional selling, as we see it, is an efficient way to encash some of your locked home equity when you need it most – whether to pay for increased mortgage costs or increased cost of living. You can achieve this by entering into an agreement with Pauzible to receive monthly payments for 2 - 5 years. Pauzible’s share of the value of your home will typically be less than a fifth and you as the owner will remain the sole titleholder.

Q: How much home equity do I need for fractional selling?

A: Ideally you need at least 35% home equity for this product to be suitable for you, although, depending on your circumstances, we could even consider cases with around 30% home equity.

Q: What happens after the 5 or 10-year term with Pauzible?

A: The agreement is structured as a forward sale of the property, with completion scheduled at the end of 5 years or 10 years, as agreed. The owner has the full duration of the agreement to buy back Pauzible’s share, unless they sell or remortgage the house earlier. If the owner decides not to buy back Pauzible’s share by the end of the agreement term, Pauzible has the right to buy the owner’s share of the property (typically 85%). Even then owners would have retained most of the appreciation in the value of their property.

Q: How do I compare Pauzible with other downsizing options?

A: Typical downsizing options involve selling the property and buying a smaller house or a house in a less desirable location. There are significant costs involved, such as estate agent fees and the price appreciation potential you will forego by selling in the currently distressed property market. Any new mortgage on the new property, to the extent that one is needed, will also involve paying the current high mortgage rates.

Q: What happens if the property value decreases?

A: Pauzible receives a fair share of the sale or market price of the home. If the value goes up, you make more and we make more. If the value doesn’t go up, we make less.

References:

1. Article: How increases in housing costs impact households | Released On: 9 January 2023 | ONS (ons.gov.uk)

About the author

Rajesh Pai

Co-Founder

Partner at ASIL, a financial services firm. Previously structurer at Barclays Capital and consultant at Deutsche Bank and UBS. Wide experience in asset classes from mortgage backed securities to liquid currencies

Ready to see what Pauzible could unlock?

Explore how accessing equity from your BTL property could support your business investment plans.

No obligation. Just a clear view of what might be possible.