Buy-to-let mortgages are typically “interest-only”. Under these, the entire loan amount is repaid in a single instalment at the end of the mortgage term. Interest, however, is paid throughout the life of the mortgage on the entire loan amount. The mortgage rate is typically reset every two or five years.

08/04/2025By Rajesh Pai · Co-Founder

Buy-to-let mortgages are typically “interest-only”. Under these, the entire loan amount is repaid in a single instalment at the end of the mortgage term. Interest, however, is paid throughout the life of the mortgage on the entire loan amount. The mortgage rate is typically reset every two or five years.

“Refinancing” a BTL interest-only mortgage effectively means replacing the current mortgage with a new one from a new lender. This is also known as “remortgaging” and it is usually considered by BTL borrowers if they want to achieve one or more of the following objectives:

Increase the loan amount and release some equity from their BTL property.

Increase the term of their mortgage and push the loan repayment date out further.

Reduce their mortgage rate for the next two- or five-year mortgage rate term.

This article considers the BTL refinancing challenges today, particularly for interest-only mortgages, which are a mainstay in the sector.

LTV

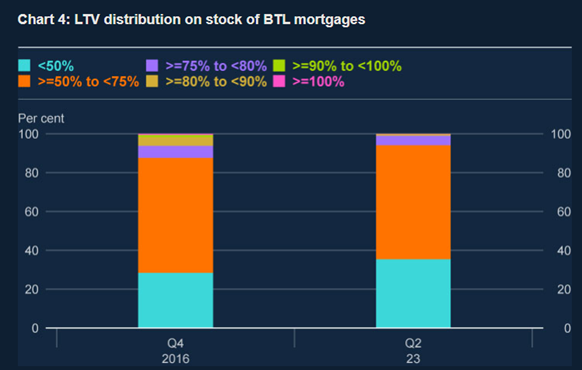

BTL lenders typically do not lend more than 60% - 75% of the value the property being mortgaged. Therefore, if the borrower’s objective is to increase the existing loan amount and release some home equity, the outstanding mortgage loan amount as a proportion of the current value of the property, or the “loan-to-value ratio” or “LTV”, must be significantly less than 60% - 75%.

This could be the case, for example, if, when the current loan was taken out, the LTV was 60% - 75%, but there has been a significant appreciation in the price of the property since then and the current LTV is much lower. This means that a 60% - 75% LTV loan amount today will be higher than the original loan amount and some home equity release will thus be possible.

Even if this is the case, however, it is worth bearing in mind that the new lender will usually allow the proceeds of the equity release from the remortgage to be used only for certain specified purposes, such as making another property investment.

Source: Bank of England¹

Loan affordability checks

In addition, the prospective new lender will want its loan affordability checks to be satisfied.

Mortgage interest affordability check

One of these is to check that the annual rental income from the BTL property exceeds the annual mortgage interest by a certain minimum margin, usually 25%, even if the mortgage rate were to rise by a few percentage points, say 1% - 2%1, above its current level.

2-year fixed BTL mortgage rates today are around 5.99%2. For mortgage interest affordability check purposes, a lender will assume a higher, or “stressed”, mortgage rate of around 8% if the landlord is refinancing. Assuming that the expected mortgage loan amount will be 60% of the current value of the property, the stressed mortgage interest will thus be 4.8% (8% x 60%) of the current value of the property.

Gross rental yield

The annual rental income as a proportion of the current value of the property, or “gross rental yield”, would, therefore, need to be at least 4.8% to satisfy the mortgage interest affordability check. Gross rental yields currently vary widely across the UK, from c. 5% in London to c. 8% in some parts of northern England3.

With an average gross rental yield of 5% in London, for example, many BTL properties would fail the mortgage interest affordability check. To pass this check, all other things being equal, the mortgage loan amount would need to be lower, i.e. the BTL landlord’s equity contribution would need to increase. However, this might mean compromising on a key objective of the remortgage: to increase the loan amount and release some home equity.

Personal income check

Another affordability check is the BTL landlord’s personal income.

While the mortgage interest affordability check may be satisfied, a BTL landlord is still expected to have a minimum personal annual income of c.£25,000 per year.

If the gross rental yield fails the mortgage interest affordability check, however, a personal income affordability check can be applied, if the BTL landlord agrees to it, to see if their personal income would make up for the shortfall in rental income. The personal income affordability check involves a detailed assessment of the borrower’s personal post-tax income and household expenditure.

Means of loan repayment

Even if the mortgage interest and personal income affordability checks are satisfied, as BTL mortgages are usually “interest-only”, BTL lenders will typically also want BTL borrowers to confirm that they will have made arrangements to repay the entire loan amount at the end of the mortgage term by means other than through sale of the mortgaged property. To this extent, it helps if BTL landlords have a liquid investment portfolio of sufficient size.

Increasing the length of mortgage term

As well as increasing the loan amount and releasing some home equity, another common remortgaging objective is to increase the length of the mortgage term. This is usually straightforward if the borrower will not be older than 70 when the mortgage term ends and the total length of the mortgage term will not exceed 25 years. So, for example, if the person who is remortgaging is 45 years old, they will usually be able to get a mortgage with a term of 25 years, but if they are 50 years old, the available term might be reduced to 20 years. However, even this might be advantageous for someone who took out their original BTL interest-only mortgage 20 years ago, when they were, say, 30 years old, for a mortgage term of 25 years. Now they are 50 years old and the remaining term of their mortgage is 5 years. A remortgage could enable them to increase their remaining mortgage term by 15 years to 20 years, i.e. until they turn 70.

Interest rate

As well as increasing the loan amount and releasing some home equity and extending the term of the mortgage, yet another remortgaging objective might be to achieve a reduction in the mortgage rate.

However, whilst a remortgage might offer a better initial 2-year or 5-year rate than that available from refixing the short-term rate on the existing mortgage, this rate is typically unlikely to be significantly better. In any case, the short-term rates offered by the new lender at subsequent refixes might not be very different from those that would have been offered by the existing lender.

Therefore, it is worth considering carefully if abetter initial 2-year or 5-year rate is a good enough reason to remortgage, especially if other key objectives, such as increasing the loan amount and releasing home equity, for example, cannot be met due to affordability check constraints.

It is also worth bearing in mind that a remortgage involves appointing a mortgage broker and solicitor, making a new loan application, an independent valuation of the BTL property, loan affordability checks, property searches, legal completion, and registration of a charge with the Land Registry. Remortgaging is thus a relatively complex and time-consuming process and should not be undertaken lightly.

Here is a table summarising some of the key parameters lenders look at for BTL lending:

Key parameters for remortgaging BTL

Parameter

Constraints

Loan to Value

Typically, less than 60-70%

Monthly Gross Rent

Must exceed monthly mortgage payment by 25%

Personal Income

Exceed £ 25,000 p.a.

Mortgage Term

Borrower should be less than 70 years old at end of mortgage term

Reduction in BTL mortgage lending

In forecast figures published by UK Finance4 for 2024 and 2025, together with projected full year figures for 2023, mortgage lending trends for BTL properties show a marked reduction by c. 50% year-on-year given the stark realities highlighted in this article above. This is a much starker reduction than the figures for owner occupied residential properties, putting the spotlight on the remortgage challenge for BTL landlords.

The Pauzible BTL Solution

For landlords stuck in a negative cash flow situation, Pauzible’s innovative solution offers an alternative. Instead of forking out more money from their own pocket to retain their BTL property or taking on additional personal debt or being forced to sell their property in a down market, Pauzible gives qualifying landlords monthly payments to tide over the effects of increased mortgage costs and gives them breathing space for 5 - 10 years. In the meantime, a combination of mortgage rate cuts, rising house prices and improving rental yields could see their home equity increase significantly and provide them with a better outcome in the long run.

References:

1.The buy-to-let sector and financial stability | Published on: 15 December 2023 | Bank of England |

2.Buy-to-let mortgages rates | Uswitch

3.The highest yielding areas for buy-to-let property in the UK | Published on: 12 December 2023 | Zoopla

4.Mortgage Market Forecasts | Release date: 11 December 2023 | UK Finance

Q. My rental income isn't covering the higher mortgage payments with rising rates. Can I still remortgage?

A: We would urge you to speak to your mortgage advisor to consider your unique circumstances, but in general you will probably find it hard to find a new lender in this situation. You may also be able to consider alternative solutions like Pauzible.

Q. Is it worth fixing my BTL mortgage rate now, or should I wait for rates to stabilize?

A: No one has a crystal ball to predict the future and there are pros and cons for fixing and waiting for rates to stabilize.

Fixing means biting the bullet and securing a rate for 2 or 5 years which gives you certainty. You may however, miss out on any future rate cuts in that period. By staying on a floating rate, you run the risk of making even higher payments if interest rates turn higher in the future – a possibility one cannot rule out. In any case, sticking to a lender’s Standard Variable Rate because your fixed rate deal has ended may be a worse outcome as these typically are way higher than floating rate mortgages such as tracker mortgages.

Q. I'm worried about lower property values. Will I still be able to remortgage and release equity?

A: As long as you qualify based on the lender’s criteria, you can still remortgage and release equity.

However, if your view is that property values will decrease in the long term, you may be better off by selling your property today and repaying your mortgage, rather than holding onto your property and realising a lower value from your property in the future.

Q. Can I use a bridging loan to overcome affordability hurdles and secure a better remortgage deal?

A: Bridging loans typically last12-18 months and the interest rates are higher than a traditional first charge mortgage, and come with a second charge on the property if you meet the bridge lender’s criteria. While this may be a suitable option for some, it still adds on to the debt against the property and the landlord might have to make monthly payments higher than their current mortgage requires.

About the author

Rajesh Pai

Co-Founder

Partner at ASIL, a financial services firm. Previously structurer at Barclays Capital and consultant at Deutsche Bank and UBS. Wide experience in asset classes from mortgage backed securities to liquid currencies

Ready to see what Pauzible could unlock?

Explore how accessing equity from your BTL property could support your business investment plans.

No obligation. Just a clear view of what might be possible.