Explore the intricacies of mortgage securitisation in the UK. Understand the process, benefits, risks, regulatory landscape, and its potential impact on lenders and borrowers.

10/07/2024By Pauzible Team · Editorial Team

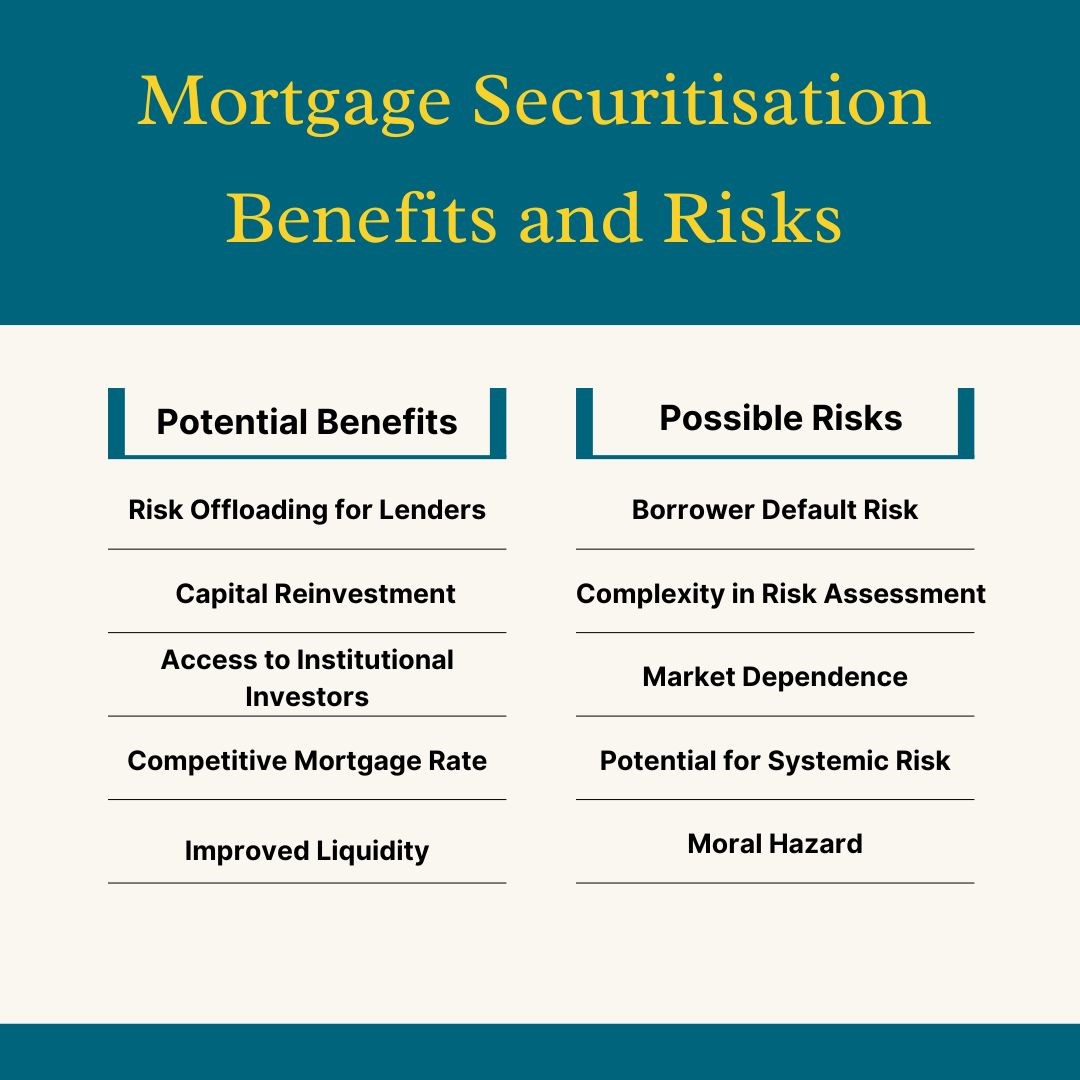

Mortgage securitisation is a financial innovation which has significantly transformed the UK's mortgage lending landscape. Lenders can tap into the capital markets and access competitive funding from institutional investors by pooling together individual mortgage loans and selling securities backed by these. This process allows lenders to free up their balance sheet for further lending, and repackage and disperse mortgage risks to institutional investors.

The Process Explained

The mortgage securitisation process involves several key steps. A lender, or the originator, assembles a pool of mortgage loans with similar characteristics, such as interest rates, maturities and credit quality. These loans are sold to a special purpose vehicle (SPV), a legally separate entity explicitly created for the securitisation transaction.

The SPV issues various tranches of securities to investors to fund its purchase of the loans, with each tranche of securities representing a different level of risk. The senior tranches are considered the least risky, typically receiving higher credit ratings and offering lower interest rates. Conversely, the subordinated tranches, which bear the initial brunt of any mortgage defaults in the underlying loan pool, carry higher risk, receive lower credit ratings or might be unrated and offer higher interest rates.

Benefits and Risks:

Mortgage securitisation offers several benefits to both mortgage lenders and borrowers. It allows lenders to offload mortgage risks from their balance sheets, freeing up capital that can be reinvested into new lending opportunities. Additionally, securitisation enables lenders to tap into a broad institutional investor base, potentially lowering their funding costs and allowing them to offer borrowers more competitive mortgage rates.

However, securitisation has its risks. If borrowers default on their payments with respect to the mortgages in the underlying loan pool, the cash flows to investors in the related mortgage-backed securities could be reduced, leading to losses for investors. Furthermore, some securitisation structures can make it challenging for investors to assess their risk exposure accurately.

Impact on Borrowers:

Mortgage securitisation has its pros and cons for borrowers. On the positive side, increased liquidity and competition provided by the market in mortgage-backed securities can lead to a broader range of mortgage product offerings and potentially lower interest rates. However, during periods of economic uncertainty and turbulent markets, the appetite for mortgage-backed securities may diminish, leading to tighter lending standards, higher interest rates and reduced availability of mortgage products.

Borrowers need to understand that their mortgage payments ultimately contribute to the cash flows that service the securities held by investors. As such, their ability to make timely payments or otherwise can have ripple effects throughout the securitisation chain.

Regulation:

The regulation of mortgage securitisation in the UK is critical to maintaining a stable financial system. The Financial Conduct Authority (FCA) and the Prudential Regulation Authority (PRA) play pivotal roles in overseeing the securitisation market and ensuring that firms adhere to rigorous disclosure and risk retention requirements, for example.

In the wake of Brexit, the UK Securitisation Regulation retained EU law in this area. It set forth a comprehensive framework for securitisation practices, including due diligence disclosure and risk retention provisions. On 30 April 2024, the FCA and PRA published their final rules and requirements relating to securitisation to replace the assimilated EU Securitisation Regulation with domestic law. These will come into effect on 1 November 2024, following a six-month transition period. As expected, these rules largely preserve the substance of the regime they are replacing.

Potential Benefits for Lenders and Borrowers:

A well-functioning securitisation market requires a delicate balance of regulatory oversight, investor confidence and responsible lending practices.

Mortgage securitisation has the potential to create a virtuous cycle of benefits for both lenders and borrowers. For lenders, the ability to offload mortgage risks and access broader funding sources can enhance their lending capacity and offer borrowers more competitive rates and products.

From the borrower's perspective, increased competition and liquidity in the mortgage market can translate into more favourable terms, such as lower interest rates. Additionally, the availability of a wider range of mortgage products can better cater to borrowers' diverse needs and circumstances.

However, it is essential to recognize that these potential benefits are not guaranteed and can be influenced by various economic and market factors.

Examples of How Securitisation Might Influence Mortgage Availability:

The influence of securitisation on mortgage availability can manifest in several ways. During periods of economic growth and investor confidence, the demand for mortgage-backed securities may rise, prompting lenders to expand their lending activities and introduce new mortgage products to capitalize on this demand.

Conversely, in times of economic uncertainty or financial market turmoil, the appetite for these securitised products may wane, leading to a contraction in the securitisation market. This, in turn, could result in lenders tightening their lending standards and reducing the availability of mortgage products, particularly for borrowers with less-than-perfect credit profiles.

Furthermore, regulatory changes or shifts in investor preferences can also impact the securitisation landscape. For example, if regulations mandate higher capital requirements or stricter risk retention rules, lenders may become more cautious in their lending and securitisation activities, potentially affecting the availability and pricing of mortgages.

FCA Rules Relating to Securitisation

The FCA’s Policy Statement of 30 April 2024 (PS24/4) contains the final Securitisation Sourcebook. All previous Technical Standards and annexes related to the UK Securitisation Regulation are also set out, to the extent retained, in this final Securitisation Sourcebook as rule requirements.

Some key policy objectives include:

Investor Protection: The FCA’s rules on risk retention seek to align the interests of the manufacturers of securitisation with those of investors in the securities. They seek to balance investor protection with access to investment opportunities by focusing on sufficient and timely disclosures that enable investors to assess risks adequately and make informed investment decisions.

Market Integrity: The rules are designed to strengthen the functioning and integrity of the UK securitisation market. Aligning the FCA’s rule drafting with that of the PRA is aimed at improving the coherence and uniformity of the regulatory regime.

Competition: The FCA believes that a clearer and more proportionate regulatory framework supports competition and that the securitisation rules should facilitate this.

Secondary International Competitiveness and Growth Objective: The FCA’s rules contribute to market stability, protecting investors and consumers, and thus building confidence in UK financial markets and institutions. This, in turn, should lead to increasing investment in the UK, further increasing productivity, market size and depth.

FAQs:

Q. What is mortgage securitisation?

A: Mortgage securitisation is a process whereby individual mortgage loans are bundled together and sold to a special purpose vehicle. This vehicle issues various tranches of securities to investors to fund the purchase of the loans, with each tranche of securities representing a different level of risk and expected return.

Q. Why is mortgage securitisation used?

A: By selling mortgage-backed securities to investors, lenders can access more capital to finance new borrowing and manage their risks. It also creates investment opportunities for investors looking for exposure to the underlying mortgage loan market.

Q. What are the risks of mortgage securitisation?

A: If borrowers default on mortgages in the underlying loan pool, the value of the mortgage-backed securities may decrease, impacting investors. There is also a risk that investors in mortgage-backed securities are sometimes unable to analyse the risks of the mortgages in the underlying loan pool adequately.

Q. How does mortgage securitisation affect borrowers?

A: For borrowers, securitisation can mean more available credit and potentially lower mortgage rates due to increased competition and liquidity in the market. However, the influence of securitisation on mortgage rates and availability can vary with market conditions.

Q. Is mortgage securitisation regulated?

A: Mortgage securitisation is regulated by the Financial Conduct Authority and Prudential Regulation Authority.

The Pauzible Team consists of finance professionals and property market specialists dedicated to reinventing home ownership and BTL financing. With deep expertise across UK real estate and innovative financial products like Equity Partnership Agreements, we provide landlords and homeowners with the insights they need to unlock equity, navigate market volatility, and build sustainable wealth through property. Our mission is to make complex property finance simpler, quicker, and more accessible for everyone.

Ready to see what Pauzible could unlock?

Explore how accessing equity from your BTL property could support your business investment plans.

No obligation. Just a clear view of what might be possible.