Home equity is the portion of the value in your property you genuinely own after deducting any outstanding mortgage or loan amount secured against it. It is a crucial aspect of homeownership in the UK, as it helps homeowners understand their asset's net worth. To calculate home equity, you need to find the difference between your property's current market value and the outstanding balance on any mortgages or secured loans against it.

08/04/2025By Pauzible Team · Editorial Team

Defining Home Equity

Home equity is the portion of the value in your property you genuinely own after deducting any outstanding mortgage or loan amount secured against it. It is a crucial aspect of homeownership in the UK, as it helps homeowners understand their asset's net worth. To calculate home equity, you need to find the difference between your property's current market value and the outstanding balance on any mortgages or secured loans against it. For example, if your home is valued at £250,000, and your outstanding mortgage is £150,000, your home equity is £100,000.

Accessing and Building Home Equity

There are different ways to access the equity in your home, such as equity release or home equity loans, which illustrate how home equity works. It's important to borrow responsibly. You can also increase your equity by making regular mortgage payments, allowing for market appreciation, renovating your home, or overpaying your mortgage. As a homeowner, you have various options to access your equity. You can apply for a home equity loan or engage in equity release, which allows you to borrow against the value of your property.. Remember that borrowing against your home's equity means your home is used as collateral, which means your property could be at risk if you cannot keep up with repayments.

You can build equity in your home by making regular mortgage payments, which decreases the principal balance over time. Additionally, if the value of your property increases due to market conditions or renovations that you make to your home; this can boost your equity. Overpaying on your mortgage, when your financial situation allows, is another way to build equity more quickly, although you should be aware of any potential early repayment charges.

The Benefits and Risks of Leveraging Home Equity

When contemplating borrowing against your home equity, weigh the potential advantages and disadvantages carefully. One of the key benefits of borrowing against your home equity is that it can provide you with a large sum of money. This can be particularly useful if you have significant expenses, such as unexpected medical bills, home repairs, or tuition, showcasing what equity in a home means in practical terms.

In addition to providing access to funds, borrowing against home equity may also offer potential tax benefits. For instance, interest paid on a home equity loan may be tax-deductible, lowering your overall tax burden.

Another potential advantage of borrowing against home equity is consolidating debt. Using the funds to pay off high-interest credit card debt can lower your overall interest rate and save money over time.

However, it's important to note that borrowing against home equity also carries risks. One of the most significant risks is the possibility of repossession if you cannot make your loan payments. Additionally, borrowing against home equity may result in paying more interest over the long run, increasing the total cost of the loan.

To make an informed decision, it's essential to evaluate your situation comprehensively. Consider your financial stability, ability to make loan payments and long-term financial goals. By carefully weighing the pros and cons, you can determine whether borrowing against your home equity is the right choice.

Understanding How Equity Can Become Negative

If the value of your property drops below the amount you owe on your mortgage, you may end up in negative equity. This can create problems when selling or refinancing your home. Negative equity occurs when the market value of your home is less than the outstanding amount on your mortgage. This can happen if property prices fall after you purchase your home, especially if you initially made a small deposit. Being in negative equity may mean you cannot remortgage without putting in more money towards a deposit. It may also mean if you were forced to sell at that point, you may have to dip into your own pocket to pay off a portion of your mortgage and further crystallise your loss.

The Role of Home Equity in Wealth Building

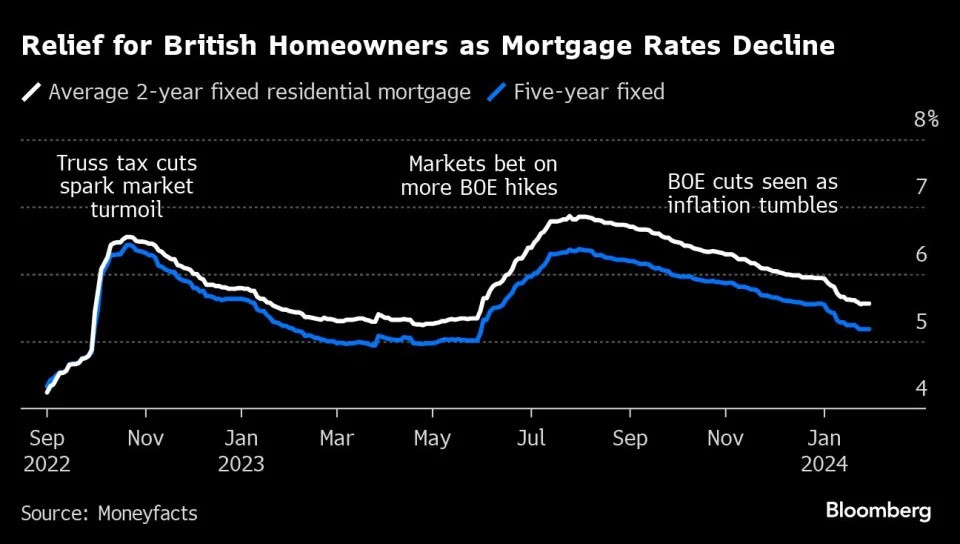

Source: Bloomberg¹

As you pay off your mortgage and the value of your property appreciates over time, you'll accumulate home equity. This equity is essential in building wealth and financial stability in households. It can play a significant role in your overall financial planning, underpinning the importance of equity in property.

For instance, imagine you purchased a home for £300,000 with a 10% down payment and took out a mortgage for £270,000. After some years, if your home is now worth £350,000 and you still owe £220,000 on your mortgage, your home equity is now £130,000. This equity can be used as leverage for future financial endeavours or accessed as needed.

Pauzible and Home Equity

Pauzible can play a transformative role for homeowners looking to leverage their home equity without selling their property or increasing their monthly financial burdens. For those looking to access their home equity for renovations, debt consolidation, or other significant financial ventures, Pauzible provides an innovative alternative.

Homeowners can partner with Pauzible to unlock the value of their property. This is particularly useful in scenarios where there may be better fits than traditional home equity loans or lines of credit due to current financial constraints or the homeowner's preference to avoid additional monthly repayments. Pauzible's model allows for strategic financial planning, offering homeowners a way to tap into their home's equity without deferring mortgage payments.

This approach can be especially beneficial in a market where rising interest rates impact the affordability of traditional borrowing methods. By utilizing Pauzible's services, homeowners can effectively pause making part of their mortgage payments (Pauzible makes up for these payments), thus reducing immediate out-of-pocket expenses. This financial relief could enable homeowners to maintain or improve their lifestyle, invest in their properties, or manage unexpected financial challenges more comfortably.

Pauzible is a financial partner, investing in the property alongside the homeowner. This partnership is designed to support homeowners in realizing their financial goals, whether that's through home improvements that could increase the property's market value or through other wealth-building strategies.

In Summary

Strategic management of home equity can provide you with security today and offer options for leveraging funds in the future. You need to evaluate the risks and benefits thoroughly to achieve optimal outcomes. A comprehensive understanding of home equity and its effective management can become a powerful component of your financial strategy, providing various options to support your current and future financial needs.

FAQs:

Q: What is equity in a house?

A: Equity in a house is the portion of the property's value that the homeowner truly owns outright. It's calculated by taking the house's current market value and subtracting any outstanding mortgage or secured debts against it. If the property value appreciates or the owner makes regular mortgage payments on a repayment mortgage, the owner’s equity increases.

Q: How does house equity work?

A: House equity works as a financial stake in your property. Your equity increases as you repay your mortgage, and your property appreciates in value. This growth in equity reflects your increasing ownership stake in the property.

Q: How do you use equity in your home?

A: You can use the equity in your home by taking out a loan against it, such as a home equity loan . This can provide funds for home improvements, debt consolidation, or other financial needs, using your home as collateral.

Q: How quickly can you build equity in your home?

A: Building equity can be quick with a substantial down payment, consistent mortgage repayments, home improvements, or if the property's market value rises. The quicker you pay down the principal on the mortgage, the faster you build equity.

Q: What are the different ways to access my home equity?

A: You can access your home equity through a home equity loan, or by remortgaging your home with a higher mortgage balance than in the previous mortgage. (i.e.not a like-for-like remortgage) a. Some homeowners may choose to sell their property to access equity or opt for a reverse mortgage if they meet age requirements.

Q: What is a like-for-like remortgage?

A: A like-for-like remortgage is when you remortgage your home or BTL property with exactly the same mortgage balance as the remaining balance on the previous mortgage. You do not extract any additional cash from the property. Lenders may provide more favourable terms for a like-for-like remortgage than otherwise

The Pauzible Team consists of finance professionals and property market specialists dedicated to reinventing home ownership and BTL financing. With deep expertise across UK real estate and innovative financial products like Equity Partnership Agreements, we provide landlords and homeowners with the insights they need to unlock equity, navigate market volatility, and build sustainable wealth through property. Our mission is to make complex property finance simpler, quicker, and more accessible for everyone.

Ready to see what Pauzible could unlock?

Explore how accessing equity from your BTL property could support your business investment plans.

No obligation. Just a clear view of what might be possible.