Unveiling the Power of Home Equity: A Comparative Analysis of Housing Wealth in the US

Homeownership has long been regarded as a corner stone of the American Dream. Besides providing a place to call home, home ownership also offers the potential for accumulating substantial wealth through the appreciation of property values and the accumulation of home equity. In this blog post, we delve into the topic of home equity, exploring its size in relation to the housing market and other asset classes in the United States.

08/04/2025By Rajesh Pai · Co-Founder

Homeownership has long been regarded as a corner stone of the American Dream. Besides providing a place to call home, home ownership also offers the potential for accumulating substantial wealth through the appreciation of property values and the accumulation of home equity. In this blog post, we delve into the topic of home equity, exploring its size in relation to the housing market and other asset classes in the United States.

Understanding Home Equity:

Before delving into the comparison, let's clarify what home equity represents. Home equity is the difference between the market value of a property and the outstanding balance of the mortgage or other loans secured by the property. Essentially, it is the portion of the home that the owner truly owns outright.

The Size of Home Equity in the US:

To start with, it is important to draw out that the average American homeowner has a mortgage of just 30% of the value of their house. That shows a healthy starting position for the housing market compared to the period just before the Great Financial Crash.

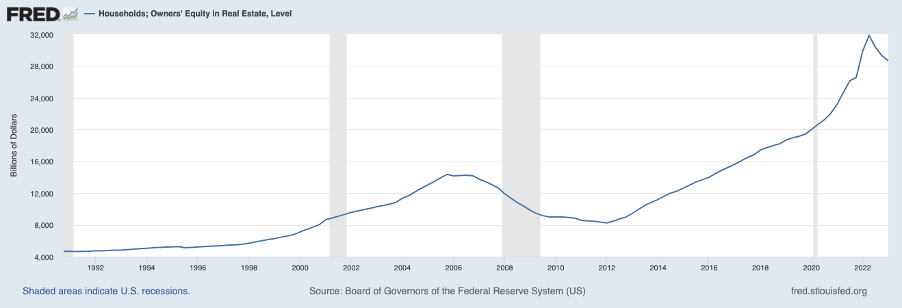

According to the Board of Governors of the Federal Reserve, the total household owners equity in the United States reached an astounding $28 trillion at the end of 2023. There is substantial wealth tied up in residential real estate across the country. To put this into perspective, the combined market value of all the homes in the US was estimated at $36.2 trillion in 2022. Homeowner equity represents a significant portion of the overall housing market.

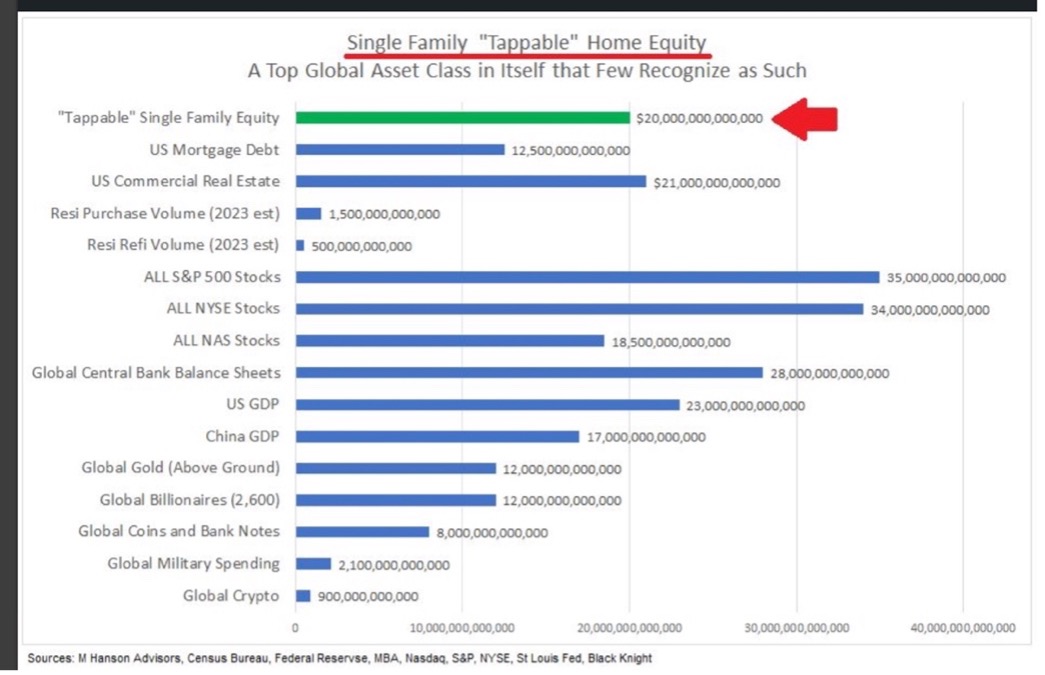

If we assume that a homeowner would be able to refinance their home based on current lending criteria then it gives us a number which is “tappable equity” which Trans union estimate at just under $20 trillion. Although other prominent research outlets suggest numbers lower than this it means that the average homeowner in the United States has $274k of equity in their home (Core Logic Homeowner Equity Report Q1 2023).

Comparing Home Equity to Other Asset Classes:

Now, let's examine how home equity measures up against other popular asset classes in the US.

1. Stocks and Equities:

The US stock market is one of the largest and most dynamic in the world. As of 2022, the total market capitalization of US equities stood at approximately $50trillion. While the size of the stock market exceeds that of home equity, it is important to note that homeownership provides a unique advantage by allowing individuals to build wealth through both housing appreciation and mortgage principal payments.

2. Bonds and Fixed Income:

Fixed-income assets, such as bonds, have long been favored by investors seeking stability and consistent returns. As of 2022, the size of the US bond market was estimated to be around $46 trillion. While bonds offer income and diversification benefits, they lack the potential for long-term capital appreciation that homeownership can provide.

3. Retirement Accounts:

Retirement accounts, such as 401(k)s and IRAs, play a vital role in Americans' financial planning. As of 2022, the total value of retirement assets in the US surpassed $35 trillion. While retirement accounts are crucial for long-term financial security, they are typically less accessible and more restricted than home equity.

4. Other Real Estate Investments:

Beyond primary residences, individuals often invest in additional real estate properties, such as rental properties or commercial real estate. These investments can provide diversification and income opportunities. However, it is worth noting that the value of home equity in the US far surpasses that of other real estate investments, underlining the widespread ownership and wealth accumulation potential tied to homeownership.

Breaking those sectors down further, expanding the analysis to emerging asset classes and introducing other forms of comparison we can see that homeowner equity remains a material asset class and potential opportunity. The caveat is of course there is less liquidity and it has additional obstacles to unlocking.

It is clear that homeowner equity is significant in size and provides a clear backstop for Americans to utilise and take advantage of, if they so choose. More and more options are appearing on how to do this ranging from additional debt, fractional ownership, or shared investment interests. We will look to talk to these in the next set of articles.

Benefits and Considerations of Home Equity:

Home equity offers several advantages as an asset class:

1. Stability and Long-Term Appreciation: Historically, residential real estate has shown resilience and the potential for long-term appreciation, helping homeowners build wealth overtime.

2. Leverage and Access to Capital: Home equity can be leveraged through home equity loans or lines of credit, providing homeowners with access to capital for various purposes, such as home improvements, education, or debt consolidation.

3. Housing Security: Owning a home provides stability and the opportunity to build roots within a community, fostering a sense of belonging and well-being.

However, it is crucial to consider potential risks associated with home equity, such as market volatility, economic downturns, and unexpected maintenance costs. Diversification across multiple asset classes is essential for a well-balanced investment and homeownership is a concentrated position albeit with the provision of other personal utility.

About the author

Rajesh Pai

Co-Founder

Partner at ASIL, a financial services firm. Previously structurer at Barclays Capital and consultant at Deutsche Bank and UBS. Wide experience in asset classes from mortgage backed securities to liquid currencies

Ready to see what Pauzible could unlock?

Explore how accessing equity from your BTL property could support your business investment plans.

No obligation. Just a clear view of what might be possible.