Fixed vs. Variable: Choosing the Right Mortgage Rate in the UK

A “fixed mortgage rate” is one where the mortgage rate that is fixed at the outset does not change during the relevant fixed mortgage rate period, for example, two or five years. It is not unusual for slightly higher fixed mortgage rates to be offered without the requirement to pay any associated product fees and relatively lower fixed mortgage rates to be offered with a requirement to pay associated product fees.

08/04/2025By Aivanaa Maraea · Co-Founder

The length of a mortgage term in the UK when the mortgage is first taken out is usually about 25 years or until the borrower turns 70 if that is expected to occur earlier. The total amount of money borrowed at the outset usually cannot be increased later. The initial outstanding mortgage balance is repaid by the borrower in monthly instalments over the life of the mortgage. The outstanding mortgage balance thus reduces after each monthly repayment instalment, until the whole of the initial mortgage loan amount is fully repaid by the end of the mortgage term. Mortgage interest is also charged to the borrower every month on the applicable outstanding mortgage balance.

Whilst the mortgage term itself may be 25 years’ long for the purposes of repayment of the initial outstanding mortgage balance, the mortgage interest rate is typically chosen by the borrower for much shorter periods, usually two or five years, from a menu of short term (usually two and five year) mortgage rates offered by the lender. These short-term mortgage rates are sometimes referred to by lenders as “deals”. Typically, as the end of the initial short term mortgage rate period approaches, borrowers are encouraged to choose a new short term mortgage rate from a new menu of short term deals the lender is offering for the next period. This process of choosing a new short term mortgage rate for the next period as each current short term rate period ends is repeated throughout the life of the mortgage.

Fixed vs variable mortgage rates

The menu of short-term deals offered by a lender typically consists of several “fixed” and “variable” two- and five-year mortgage rates.

A “fixed mortgage rate” is one where the mortgage rate that is fixed at the outset does not change during the relevant fixed mortgage rate period, for example, two or five years.

It is not unusual for slightly higher fixed mortgage rates to be offered without the requirement to pay any associated product fees and relatively lower fixed mortgage rates to be offered with a requirement to pay associated product fees. However, once product fees are factored in, seemingly higher and lower fixed mortgage rates should usually be broadly similar for the same fixed mortgage rate period, for example, two or five years.

A typical feature of a short-term fixed mortgage rate is that, if the outstanding mortgage balance is repaid before the fixed mortgage rate period ends, an early prepayment penalty applies on the balance that is prepaid. The penalty rate decreases as one gets closer to the end of the fixed rate period. So for a 5-year deal, penalty would be 5% if one prepaid in year 1, 4% in year 2, 3% in year 3 and so on.

Like a fixed mortgage rate, a “variable mortgage rate” applies only during the relevant short term variable mortgage rate period, for example two or five years. However, it can vary as it is based on the formula consisting of the Bank of England’s base rate (which can vary if the Bank changes its rate) plus a fixed annual rate or “margin”. Variable mortgage rate deals are sometimes referred to as “tracker rates”.

Again, it is not unusual for higher variable (tracker) mortgage rates to be offered without the requirement to pay any associated product fees and lower variable (tracker) mortgage rates to be offered with a requirement to pay associated product fees. However, again, once product fees are factored in, seemingly higher and lower variable (tracker) mortgage rates should usually be broadly similar for the same variable (tracker) mortgage rate period, for example, two or five years.

Unlike with fixed mortgage rates, an early prepayment penalty does not apply if the outstanding mortgage balance is repaid in full before a variable (tracker) mortgage rate period ends.

If a fixed or a variable mortgage rate deal is not chosen by the borrower at the end of the deal, the mortgage rate typically defaults to what is known as the “standard variable mortgage rate”. The Standard Variable Rates (SVR) are determined by the mortgage lender, and while they are likely to be linked to the Bank of England's base rate, they do not necessarily track the base rate. The lender has discretion in determining the SVR unlike a tracker mortgage rate where they have to immediately reflect the changes when the BOE changes its rates.

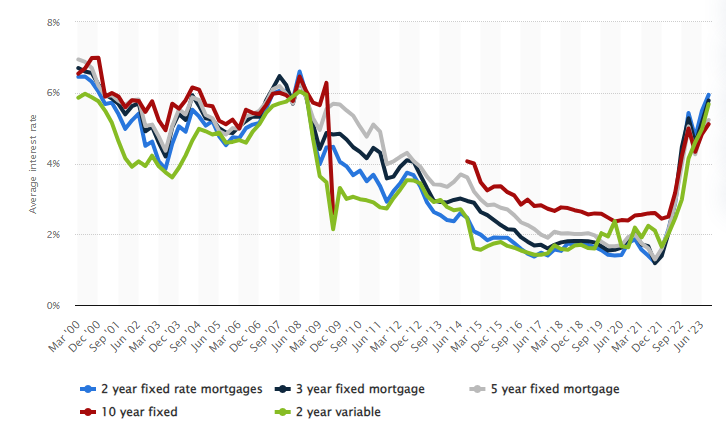

Source: Statista¹

What factors influence mortgage rates

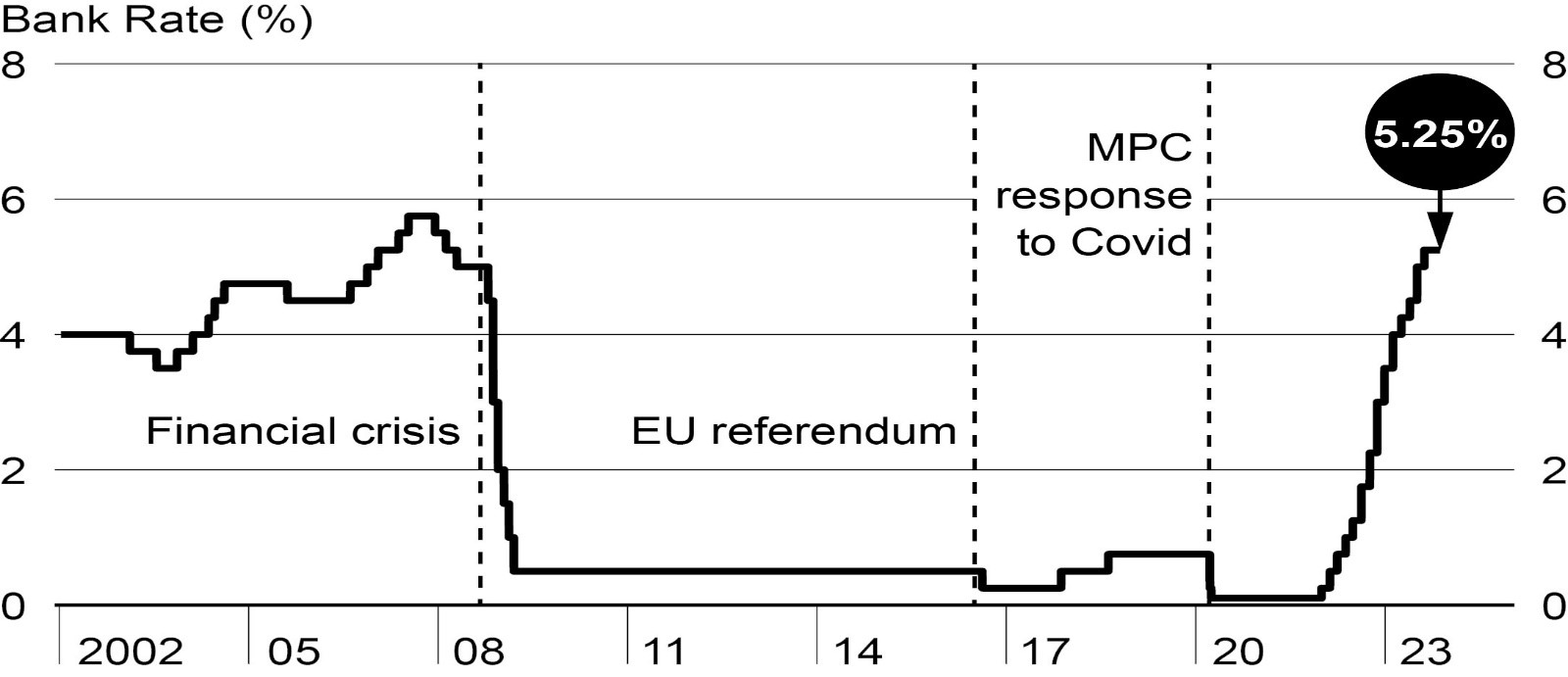

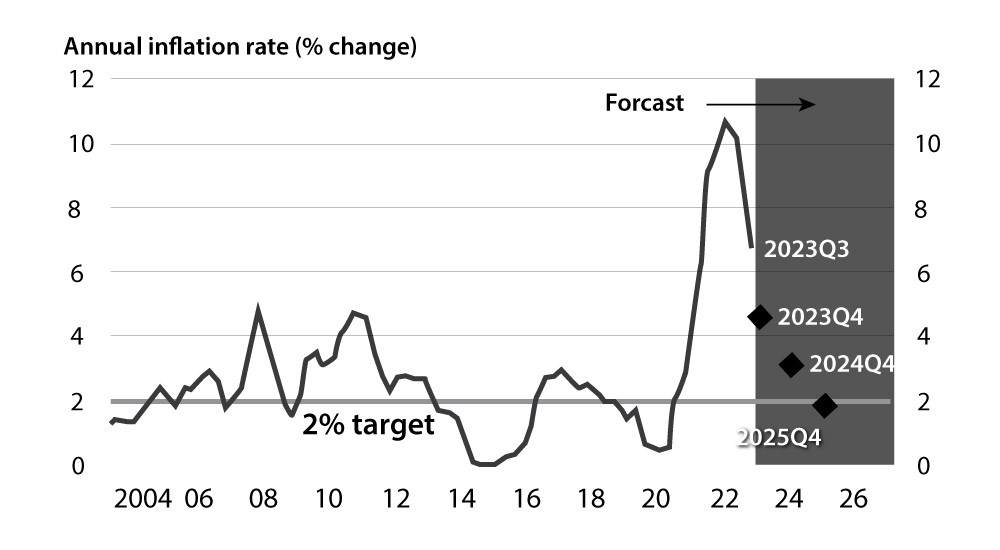

The key determinant of fixed or variable mortgage rates is the “Bank Rate” set by the Bank of England. This is sometimes also referred to as the “Bank of England base rate”, “base rate” or “interest rate”. It is the rate that the Bank charges for lending money to commercial banks. This is the Bank’s main monetary policy tool to achieve the target of keeping inflation at 2% and it is set after considering what inflation and growth in the economy are likely to be in the next few years. The Bank of England’s increased its base rate from just 0.10% in November 2021 to 5.25% on 3 August 2023, following an unprecedented 14 successive increases over the relatively short intervening three-and-a-half year period.

Source: Bank of England²

Source: Bank of England²

Financial market expectations regarding interest rates over the next five years are encapsulated in the average rate for those five years, known as the “swap rate”. Swap rates also influence the short term fixed or variable mortgage rates offered by banks to borrowers.

Other factors that influence the menu of “fixed” and “variable” two- and five-year mortgage rates that a lender offers to its borrowers include the interest rates at which the bank borrows and lends money (net interest income), the lender’s operating costs, its loan loss experience due to borrower defaults and its expectations about future house prices. Average two-year fixed mortgage rates have increased from c. 1.7% in November 2021 to c. 6% in December 2023.

How to choose a mortgage rate

A typical menu of short-term mortgage rates that a borrower might get could be as follows:

2-year fixed mortgage rate with prepayment penalties

2-year fixed mortgage rate with product fees and prepayment penalties

2-year variable (tracker) mortgage rate

2-year variable (tracker) mortgage rate with product fees

5-year fixed mortgage rate with prepayment penalties

5-year fixed mortgage rate with product fees and prepayment penalties

5-year variable (tracker) mortgage rate

5-year variable (tracker) mortgage rate with product fees

Should I choose between a fee saver and a fee-paying mortgage?

If your mortgage balance is smaller than an average mortgage balance it might make sense to choose the fee saver mortgage product. Conversely, if your mortgage balance is larger than an average mortgage it might make economic sense to choose the normal fee-paying mortgage.

For example: if the 2-year fixed fee saver is 5.04% and your balance is £500,000, the interest charge for 2 years on this is approximately going to be £50,400. If you chose the fee-paying mortgage of 4.84% with a £1,000 product fee instead, you would pay £48,400 in interest. So you would pay £2,000 extra interest on the fee saver product but would have saved only £1,000 in product fees and would be £1,000 worse off. Of course, you may decide to choose the fee saver to avoid paying fees upfront.

Assuming you have a small mortgage balance and that the product fees are factored in, the menu from which to choose could be shortened as follows:

2-year fixed mortgage rate with prepayment penalties

2-year variable (tracker) mortgage rate

5-year fixed mortgage rate with prepayment penalties

5-year variable (tracker) mortgage rate

So, what is the best mortgage rate for the borrower? A two or five year fixed or variable mortgage rate?

If, for example, the borrower believes that interest rates are likely to remain stable for the next year or two and fall significantly thereafter, it might be worth considering the 2-year fixed mortgage rate with prepayment penalties or 2-year variable (tracker) mortgage rate. If, furthermore, the borrower wants to retain the flexibility of being able to repay the outstanding mortgage balance in full within the next two years, a 2-year variable (tracker) mortgage rate might make more sense. This rate might also make sense if the borrower believes that interest rates will start falling significantly after the next one year or so. Nevertheless, the borrower might prefer the 2-year fixed mortgage rate if they want predictability in their monthly mortgage payments.

On the other hand, if the borrower believes that interest rates are likely to remain stable for the next five years or even rise slightly during that period, it might be worth considering the 5-year fixed mortgage rate with prepayment penalties or 5-year variable (tracker) mortgage rate. If, furthermore, the borrower wants to retain the flexibility of being able to repay the outstanding mortgage balance in full within the next five years, a 5-year variable (tracker) mortgage rate without prepayment penalties might make more sense. This rate might also make sense if the borrower believes that interest rates will start falling significantly after the next two years or so. Nevertheless, the borrower might prefer the 5-year fixed mortgage rate if they want predictability in their monthly mortgage payments.

In conclusion, the rate that is right for a borrower depends on their interest rate expectations, the flexibility they might want as to the timing of repaying their outstanding mortgage balance in full and the predictability they might want as to the amount of their monthly mortgage payments.

References:

1.Average interest rates for mortgages in the United Kingdom (UK) from March 2000 to September 2023, by type of mortgage | Released On: 04-Dec-2023 | Statista Research Department

2.Monetary Policy Report: November 2023 | Published on : 02-Nov-2023 | Bank of England

About the author

Aivanaa Maraea

Co-Founder

Trader at ASIL, a financial services firm. Provided broad advisory services for a Fixed Income mandate including investments in US RMBS, Trups CDOs etc. Previous experience as client relationship manager, and sales

Ready to see what Pauzible could unlock?

Explore how accessing equity from your BTL property could support your business investment plans.

No obligation. Just a clear view of what might be possible.