Trends and Predictions for UK Mortgage Rates in 2024

Understanding the dynamics of mortgage rates in the UK involves delving into some of the workings of the Bank of England (“the Bank”), as it wields considerable influence on the financial landscape of the country.

08/04/2025By Prateek Solapurker · Co-Founder

Understanding the dynamics of mortgage rates in the UK involves delving into some of the workings of the Bank of England (“the Bank”), as it wields considerable influence on the financial landscape of the country.

The Bank sets monetary policy to achieve the UK Government’s target of keeping inflation at 2%. One of the Bank’s main monetary policy tools is to set the interest rate that it charges for lending money to commercial banks. Formally, this is called the “Bank Rate”, but it is also sometimes referred to as the “Bank of England base rate”, “base rate” or even just “the interest rate”. Before determining the interest rate, the Bank’s Monetary Policy Committee (“MPC”) considers how the economy is working. It can sometimes take around two years for monetary policy to have its full effect on the economy, so the MPC considers what inflation and growth in the economy are likely to be in the next few years. The key determinant of UK mortgage rates is the interest rate set by the Bank of England.

Interest Rates set by the Bank of England and Mortgage Rates

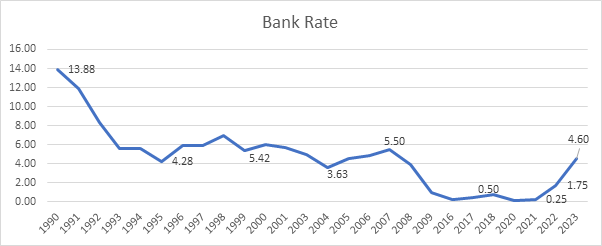

As outlined above, the Bank of England considers inflation levels, unemployment rates and the country’s economic growth when formulating its interest rate, and the rate it sets plays a pivotal role in determining mortgage rates. As inflation tends towards the 2% target level, a stabilization effect occurs, influencing the inclination to maintain rates within a range, which, except for the period after the financial crisis of 2008, has historically been about 4% - 4.5%.

Source: Bank of England 1

Economic Growth Projections and Mortgage Rates

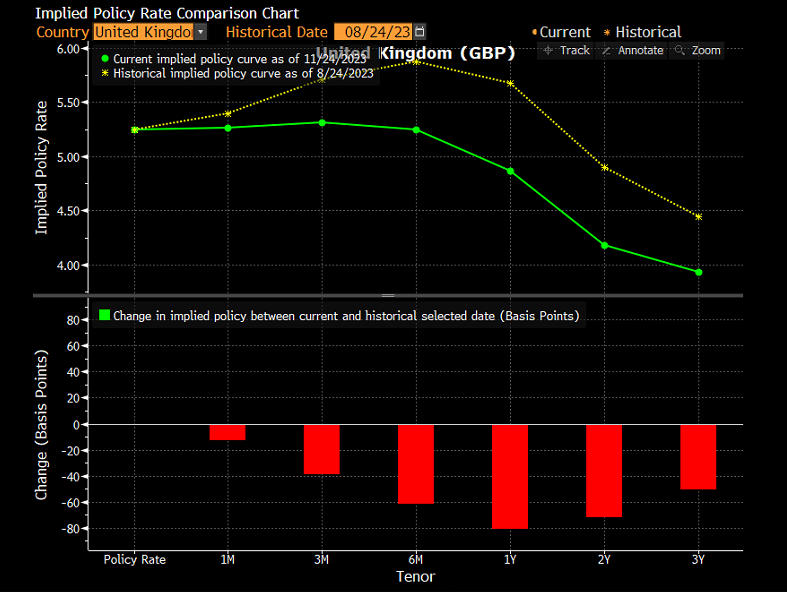

Forecasts for the upcoming year anticipate a muted economic growth trajectory. This scenario, marked by a flattish growth projection, might become a catalyst for the Bank of England to contemplate interest rate adjustments inclining towards potential decreases.

Source: Bloomberg 2

Fixed Mortgage Rates and Future Interest Rate Expectations

Mortgage rates are typically fixed for five years and encapsulate financial market expectations regarding interest rates over the next five years, which are defined by the average interest rate over that period, known as the “swap rate”. The swap rate holds considerable weight in determining the rates at which banks will lend to mortgage borrowers. The anticipation of swap rates also significantly influences banks’ willingness to lend.

Bank Expectations and Mortgage Demand

Banks’ willingness to fulfill mortgage demand is also tied to their expected returns on the mortgage loans they make. Factors affecting returns on loans include the difference between the rates at which banks borrow and lend (net interest income), banks’ operating costs, and the losses experienced on loans due to borrower defaults. Furthermore, if banks forecast a decline in house prices, they might refrain from increasing their lending volumes, which could lead to mortgage rates remaining higher than market expectations despite interest rate reductions.

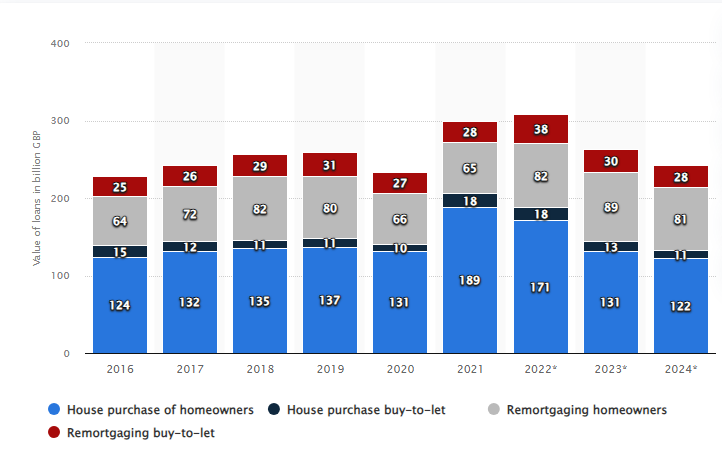

Value of mortgage lending in the United Kingdom (UK) from 2016 to 2021 and forecast until 2024, by loan purpose (in billion GBP)

Source: Statista 3

Projections for Mortgage Rates in 2024

Based on the various factors considered above, we expect five year fixed mortgage rates of between 4.25% and 4.75% for the better part of 2024. The driving force behind this range is the slight lowering in the five year average interest rate or swap rate projected in the financial markets. However, the limited demand from banks to issue more mortgages due to anticipated lower house prices contributes to sustaining these rates.

Recommendations for Borrowers

Individual borrowers face the dilemma of having to opt for a single rate from a menu of two and five year fixed and tracker rates that are typically offered to them when they are required to choose a new rate on their existing mortgage or when they remortgage. We strongly recommend speaking to your mortgage advisor on finding the right mortgage that suits your individual circumstances. Nonetheless, here we present our view on mortgage rates that might suit borrowers on low LTVs. Forecasts point to the cheapest 5-year fixed mortgage rates of 4.5% and we lean towards securing a 5-year fixed mortgage rate within the available market range, particularly if it is lower than 4.75%. Those with a different view can choose a 2-year fixed or 10-year fixed rate if they find that more attractive. Alternatively, they can choose a tracker rate if they believe that interest rates will fall in 2024 and beyond.

For those facing a significant increase in monthly mortgage payments compared to what they used to pay, regardless of which new rate they choose, and wondering how to make ends meet despite having significant wealth locked up in their home equity, Pauzible offers an alternative solution that provides mortgage payment top ups for up to five years in exchange for a fair share in the value of their property.

In conclusion, navigating the landscape of remortgaging in 2024 demands a prudent evaluation of prevailing market conditions, long term projections and individual financial circumstances. Striking a balance between seizing the most favorable rates available and ensuring personal financial stability remains pivotal in making informed decisions regarding mortgages.

References :

1.Official Bank Rate history from 1990 until 2023 | Released on: 03-Aug-2023 | Bank of England Database

2.Projections for UK Interest Rates various economists | Published on: 24-Nov-2023 | Bloomberg

3.Value of mortgage lending in the UK from 2016 to 2021 and forecast until 2024 | Published on: 13-Jul-2023 | Statista

Can't pay mortgage payment hikes?

Don’t let mortgage rate rises stress you out. Pauzible can help.

Q. When will mortgage rates in the UK start to come down?

A. Predicting exactly when mortgage rates in the UK will begin to fall is challenging. However, the consensus among many experts is that rates are likely to stay fairly consistent throughout 2024. Some specialists anticipate a potential reduction in rates during the latter half of next year, whereas others suggest that the current rate levels might persist into 2025. In any event, it is reasonable to conclude that the low mortgage rates we experienced as a result of quantitative easing following the 2008 financial crisis can now be considered as part of history.

Q. What factors will influence mortgage rates in the UK in 2024?

A. Various factors will influence the Bank of England's base rate and consequently impact UK mortgage rates in 2024, such as the prevailing inflation rate, unemployment rates and economic growth forecasts for the country. In addition, the balance of demand and supply in the mortgage market, influenced by factors such as lenders’ expectations regarding future house prices, borrower defaults and profitability, will also have an effect on mortgage rates.

Q. What can I do to protect myself from rising mortgage rates?

A. To safeguard against rising mortgage rates, consider these strategies:

Secure a fixed mortgage rate at a level and for a duration that suits you.

Make additional payments on your mortgage to lower the remaining balance.

Consult with a reputable licensed mortgage broker who can offer a tailored advice, particularly if your fixed rate period is nearing its end.

Q. How can Pauzible help?

A. If you are facing the challenge of refinancing your mortgage at a significantly higher rate than what you paid before and this is causing financial strain, Pauzible offers an innovative solution. We can cover the difference between your new and old monthly mortgage payments for up to five years in return for a fair share in the value of your property. To explore this opportunity and see if it makes sense for you, we invite you to speak with a member of our team. Take the first step towards mortgage help by booking a consultation with us.

About the author

Prateek Solapurker

Co-Founder

Previously Illiquid credit trader at HSBC. Also, Co-Head of Credit Products and Hybrids Trading, EMEA, focused on structured credit financing, risk management and structuring at HSBC, and Project Engineer at Unilever

Ready to see what Pauzible could unlock?

Explore how accessing equity from your BTL property could support your business investment plans.

No obligation. Just a clear view of what might be possible.