Towards the end of the relevant mortgage rate term, the lender provides the borrower with a new set of two and five year mortgage rates. The borrower selects a new mortgage rate to be applied for the next term of two or five years. This process of selecting a new mortgage rate every two or five years occurs throughout the life of a mortgage is referred to as “rate switching” or “switching rates” or “choosing a deal”.

08/04/2025By Rajesh Pai · Co-Founder

Whilst the duration of a mortgage loan at its outset is usually 25 years (unless the borrower is expected to turn 70 earlier), the mortgage interest rate or “mortgage rate” is usually only set for a relatively short period of just two or five years. Typically, the lender provides the borrower with a choice of two and five year mortgage rates. The borrower selects one of these. The selected mortgage rate is applied by the lender for the relevant mortgage rate term, two or five years.

Towards the end of the relevant mortgage rate term, the lender provides the borrower with a new set of two and five year mortgage rates. The borrower selects a new mortgage rate to be applied for the next term of two or five years. This process of selecting a new mortgage rate every two or five years occurs throughout the life of a mortgage is referred to as “rate switching” or “switching rates” or “choosing a deal”.

If, instead of switching the mortgage rate, the borrower decides to replace the existing mortgage with a new one, this process is referred to as a “remortgage”. A remortgage is usually associated with a new lender and changes to key mortgage terms. Thus, compared to the existing mortgage, a remortgage might allow a borrower to increase the amount of money borrowed, extend the remaining life of the mortgage and obtain a reduction in the next short term mortgage rate.

What does switching a mortgage rate involve?

Typically, towards the end of the current mortgage rate term, usually two or five years, the lender provides the borrower with a choice of new short term mortgage rates. The borrower is asked to select a new mortgage rate to be applied during the next mortgage rate term, again normally two or five years. This new mortgage rate selection process is simple and straightforward, and can usually be completed by the borrower online in just a few minutes. Nevertheless, if the borrower needs the lender’s assistance with completing the rate selection process, this can usually be obtained over the phone or in a branch with prior appointment. If the borrower needs advice regarding rate selection, however, they will need to appoint an independent mortgage broker or financial advisor.

What does a remortgage involve?

A remortgage process is more complex and time consuming. Typically, it involves finding a mortgage broker, instructing a solicitor, completing an application form for a new mortgage, property valuation, mortgage affordability checks, property searches, legal completion and registering a new charge with the Land Registry.

Timing

Lenders usually expect the remortgage process to take 4 – 8 weeks. However, in reality, it can take much longer than this. In particular, responses to local authority searches (carried out by conveyancing solicitors), covering matters such as any planned road, rail and building work around the property, can sometimes take as much as three months or longer.

It is advisable as a borrower, therefore, to start the remortgage ball rolling a few months before the date on which you would like your remortgage to take effect. If you are currently on a two or five year fixed mortgage rate, for example, you will ideally want the remortgage to start immediately after the expiry of your current mortgage rate. An earlier remortgage date will probably trigger an early prepayment charge consisting of a percentage of your existing outstanding mortgage balance. You will want to avoid that. A later remortgage date might involve choosing a variable two year mortgage rate until the remortgage becomes effective. A variable mortgage rate usually does not involve an early prepayment charge but it can be higher than a fixed mortgage rate. You will want to minimise this higher rate mortgage period as much as possible before the remortgage takes effect.

Loan amount

Once you have decided sufficiently in advance when you would like your remortgage to start, you will need to decide how much money you would like to borrow from the new lender. The minimum amount will be the outstanding mortgage balance on your existing mortgage, as you will need to repay that to your existing lender and replace that amount with the new borrowing. It is not uncommon for those remortgaging, however, to want to borrow more than their current outstanding mortgage balance. Typically, this becomes possible because, as a borrower, you will have built up additional equity in your home by having repaid some of the original borrowing on your existing mortgage and the market value of your home will also have increased since you first took out your existing mortgage. The cash realised from releasing some of your home equity through a remortgage can usually be used only for certain purposes, such as making a home improvement or another property investment.

Mortgage length and mortgage rate

As well as deciding how much you would like to borrow, you will also need to decide if you want changes made to any other key mortgage terms when you remortgage. For example, you might want to extend the life of the new mortgage beyond the remaining life of the existing one so that you have a longer period over which to spread out your monthly mortgage repayment instalments. You might also be able to achieve a reduction in your initial short term mortgage rate with the remortgage compared to switching the rate under your current mortgage.

Mortgage affordability and loan-to-value ratio

Once you have decided on the timing of your remortgage and the key outcomes from it that you desire, including additional borrowing, mortgage life extension and mortgage rate reduction, it makes sense to check if you are likely to qualify for a remortgage with those terms.

One set of factors to consider is what you can afford, i.e. your post-tax income (gross salary minus tax, and pension, national insurance and other deductions) and household expenditure (including credit card, student loan, car loan and other loan payments, child and spouse maintenance, childcare costs, school fees, travel costs, utilities, council tax, insurance premia, rent or mortgage payment, and entertainment, leisure, food, grocery, toiletries and holiday costs etc.).

Broadly, a conservative lender might consider lending up to 7 times the figure arrived at after deducting your annual household expenditure from your annual post-tax income. This is to allow for adverse possible future scenarios such as interest rates increasing by 3% or more, or other living costs also increasing more than expected.

Another set of factors to consider is the amount you wish to borrow as a percentage of the current price of your property (referred to as the “loan-to-value ratio” or “LTV”) and the proposed mortgage term (usually 25 years’ long or until you turn 70 if that is expected to happen earlier). Broadly, a conservative lender might not agree to lend more than 60% of the price of your property, even if you can comfortably afford to service and repay a higher mortgage amount.

Mortgage broker

If after considering factors such as affordability and LTV, you are still confident that you will qualify for a remortgage with the terms you desire (including additional borrowing, mortgage life extension and mortgage rate reduction), it is worth appointing a mortgage broker to help find a lender with the right remortgage product for your needs. Ideally, the mortgage broker should be a “whole of market” broker. You should also be clear as to whether or not the mortgage broker will expect a fee from you, a commission from the lender or both, and the amounts involved.

Your mortgage broker and the lender to whom they will eventually apply on your behalf will expect to see evidence of your income and expenditure, and identity, so it is also worth starting to put this together early on, including three months of payslips and bank statements, recent utility bills and credit card statements, passport or driving licence etc.

Mortgage application

If your mortgage broker also thinks that you will qualify for a remortgage with the terms that you desire, they will help you apply to a potential lender with a good fit. You should be able to obtain a non-binding offer of a “mortgage in principle” reasonably quickly. It is best to make an application for a binding offer as soon as possible after that. This will involve more comprehensive information and evidence about your finances, credit history and property.

Valuation

The lender will also organise an independent valuation of your property. Sometimes, the lender will pay the surveyor’s fees, but not always.

Remortgage offer and conveyancing

Assuming all goes according to plan, you should receive a remortgage offer within eight weeks. However, as outlined above, this process can take longer, especially if response times to local authority searches take longer than expected.

You will need to appoint a solicitor to do all the conveyancing work associated with completing the remortgage. Again, the lender will sometimes pay the legal fees, but not always. Solicitors will also incur other costs, such as those associated with searches and the Land Registry.

Should one switch rate or remortgage?

A remortgage is a fairly complex process, can take quite long and might involve additional costs if its effective date is delayed beyond the expiry of your current mortgage rate term. It is, therefore, only worth considering a remortgage if you are seeking meaningful changes to key mortgage terms compared with your existing mortgage, such as significant additional borrowing, mortgage life extension and mortgage rate reduction. If this is not the case, it is best to stick to switching rates under your existing mortgage.

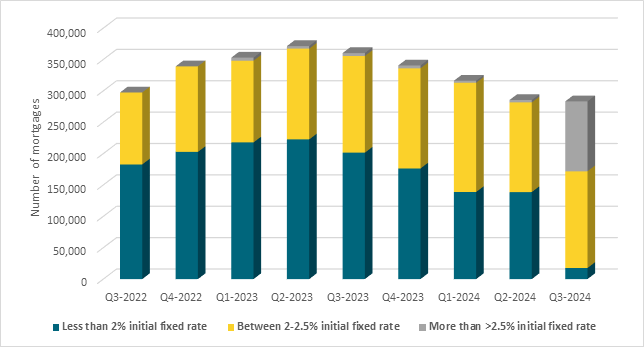

Regardless of whether you are switching rates or remortgaging, like many others at present, you might be experiencing considerable financial pressure, as mortgage rates have increased dramatically from c. 2% in November 2021 to c. 6% today and this situation has been further exacerbated by the cost of living crisis.

Pauzible may be able to help you.

Pauzible provides you with the opportunity to freeze your monthly mortgage payments at the same level as before the increase in your mortgage rate for a period of up to five years, thereby helping you protect your home. In return, Pauzible receives a fair share in the value of your home proportionate to its contribution. The Pauzible solution may suit you if you intend to own and remain in your home for at least three years and have sufficient equity in your home. To find out if you qualify, please visit and Get started.

Reference :

1.How increases in housing costs impact households | Released on: 9 January 2023 | ONS

Can't pay mortgage payment hikes?

Don’t let mortgage rate rises stress you out. Pauzible can help.

Q. I am nearing the end of my current fixed mortgage rate term. Should I switch my mortgage rate with my existing lender or remortgage?

A. It is worth considering a remortgage if you are seeking meaningful changes to key mortgage terms compared with your existing mortgage, such as significant additional borrowing, mortgage life extension and mortgage rate reduction.

If this is not the case or if you think you might not meet the affordability criteria for a remortgage with the new terms you desire, it may be best to switch rate under your existing mortgage rather than seek to remortgage.

Q. I am worried about an early repayment charge if I remortgage before the end of my fixed mortgage rate term. Can I avoid this?

A. A remortgage date before the expiry of your current fixed rate mortgage term will probably trigger an early prepayment charge consisting of a percentage of your existing outstanding mortgage balance. As you will want to avoid this, you will want your remortgage to start immediately after the expiry of your current mortgage rate.

If you think the remortgage date is likely to slip, however, it might be best to choose a tracker (not fixed) two year mortgage rate under your existing mortgage until your remortgage becomes effective. A tracker mortgage rate usually does not involve an early prepayment charge, but the rate itself can be higher than a fixed mortgage rate. You will want to try and minimise this higher rate mortgage period with your existing lender as much as possible before the remortgage takes effect.

Q. How much equity do I need in my home to be able to remortgage?

A. A conservative remortgage lender might require 40% home equity, but there may be others who might be satisfied with 20% - 25% home equity, although the latter’s mortgage rates are also likely to be higher.

In any case, any lender will consider your post-tax income and household expenditure carefully to determine if you can afford the remortgage, including under stressed conditions, such as a 3% increase in the mortgage rate.

About the author

Rajesh Pai

Co-Founder

Partner at ASIL, a financial services firm. Previously structurer at Barclays Capital and consultant at Deutsche Bank and UBS. Wide experience in asset classes from mortgage backed securities to liquid currencies

Ready to see what Pauzible could unlock?

Explore how accessing equity from your BTL property could support your business investment plans.

No obligation. Just a clear view of what might be possible.