What is Equity Release? A Brief Guide for UK Homeowners

Homeowners realize their home equity when they sell their property. However, some financial products enable homeowners without mortgages or with very small mortgages to obtain cash against the value of their home equity without having to leave their property. These are referred to as “equity release” products.

08/04/2025By Prateek Solapurker · Co-Founder

The estimated value of UK’s home equity is £5.6 trillion 1. This is the value of all privately ownedUK residential property minus the outstanding mortgage balances on those properties. Home equity constitutes the bulk of the wealth of UK households who own their homes. However, despite this wealth, many homeowners struggle to lead comfortable lives.

Typically, homeowners realize their home equity when they sell their property. However, some financial products enable homeowners without mortgages or with very small mortgages to obtain cash against the value of their home equity without having to leave their property. These are referred to as “equity release” products.

The cash receipts from such products can consist of either upfront lump sums or regular payments over years. Equity release products are aimed at older homeowners whose income or pension or cash savings are not enough for them to be able to maintain the lifestyle they desire.

Total value of private property

Total mortgage debt

Net property wealth

Value in Pounds (Trillions, Dec 22)

7.3

1.6

5.6

Source: Equity Release Council ¹

Equity Release products for those who are 55 or over:

Lifetime Mortgage. This is the most common type of equity release product. Under its terms, typically, the homeowner receives a cash lump sum from the lender, which is secured as a loan against the value of the home. Instead of regular mortgage payments made by the borrower to the lender, however, interest accrues on the loan and is added to the outstanding loan amount. Interest then accrues on the increased loan amount and that loan amount thus increases even further. This process is repeated until the end of the mortgage term, which occurs when the borrower dies or moves into a care home. At that point, the outstanding loan amount is repaid from the proceeds of the sale of the mortgaged property.

Minimum Eligible Age: 55 years.

Home Reversion Plan. Under the terms of this type of equity release product, the homeowner sells either a part or the whole of their property to the home reversion plan provider. In return, they receive a cash lump sum or regular cash payments and the right to live in the property as a tenant rent-free until they die or move into a care home.

Minimum Eligible Age: 60 years.

Equity Release for under 55s?

Equity release products are not available to those under 55. The primary reason for this is that younger homeowners often still have substantial traditional first charge mortgages on their properties. Equity release providers consider the risks of being subordinated to first charge mortgage lenders and providing their products against relatively low home equity values as being too high.

Pauzible

Due to a prolonged period of low interest rates (from c. 2009 to 2022), however, many homeowners, including those younger than 55, are sitting on substantial amounts of home equity and at the same time facing financial pressures due a significant recent increase in their mortgage rate, as well as the general cost of living crisis.

Pauzible provides a solution to such struggling households by helping them turn some of their home equity into cash without increasing their debt burden, and giving them time to balance their income and expenditure over a long period, while they continue to gain from an appreciation in the price of their property.

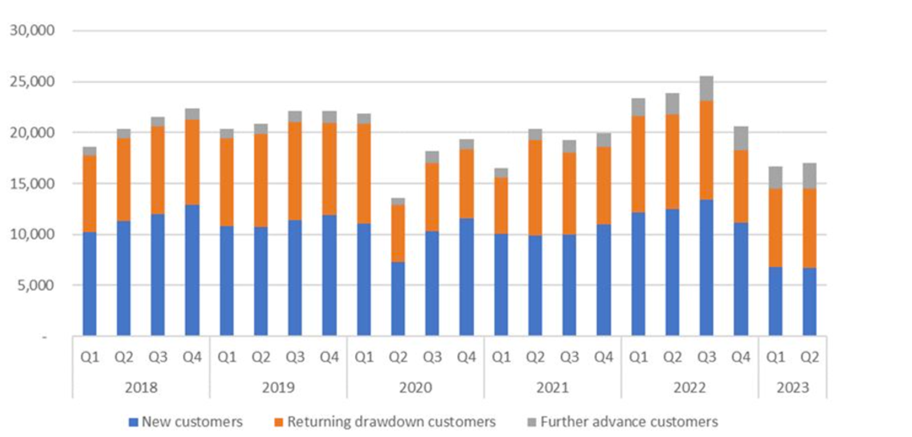

Equity Release Customers by type, Q1 2018 – Q2 2023

Source: Equity Release Council ²

Number of new equity release plans agreed per month, Apr 2020 to Jun 2023

Source: Equity Release Council ²

How does a lifetime mortgage work

A lifetime mortgage is simply a loan that has to be repaid. Like any other loan, the borrower receives the borrowed amount (either as a single lump sum or in the form of regular payments) at an annual interest rate. The only difference is that no payment to the lender occurs until the property is sold, which happens when the borrower dies or moves into a care home. The interest amount is added every month to the borrowed amount; thus, the subsequent month’s borrowed amount increases by the prior month’s interest amount. This process is referred to as the “compounding” of interest and it can rapidly lead to a ballooning of the total loan amount owing to the lender.

Still, lifetime mortgages allow older homeowners to continue to live in their homes until the end of their lives or until they move into a care home, with the borrowed amount being deducted from the proceeds of the sale of their property at that point. Lifetime mortgage lenders usually guarantee that homeowners will not owe an amount larger than the value of the property when it is sold. This is called a “no-negative equity guarantee”. It gives homeowners the comfort that their estate and next of kin are not left with a large debt to repay.

Worked Example

Let us consider a hypothetical worked example:

John Smith is a 65-year-old resident of Devon. John purchased his house for £100,000 in 1993. We are now in 2023. John has repaid his entire mortgage and owns his property outright. It is currently valued at £250,000.

John’s monthly pension is £1,200. However, it is not enough for him to be able to lead the quality of life that he wants. John can opt for an equity release lifetime mortgage with a 7.5% annual interest rate. This will enable him to receive an upfront cash lump sum of £50,000, which will help him boost his spending power, including being able to take the occasional holiday.

In 10 years’ time, John will owe £105,603. His home equity value at that stage will depend on whether house prices have appreciated or remained stagnant. In the event of stagnant property prices, John’s property will still be worth only £250,000, but he will have forfeited c. 40% of the property’s value to the mortgage lender already by then, leaving him with only c. 60% home equity. On the other hand, if house prices increase at an average rate of 4% per year, the value of his property will have soared to £370,061, with his home equity worth £264,458 (c. 71%) at that stage. , so he will have given away only 29% of the property value.

Home Reversion Plans

Under the terms of home reversion plans, homeowners sell a part or the whole of their property today with the ability to live in the property for the rest of their lives or until they move into a care home. They also receive a cash lump sum or regular cash payments. For these reasons, the value of the property is often discounted significantly compared to its market price. The amounts that sellers receive also depends on their age and health, and the condition of their property.

Is Equity Release Suitable for You?

If you are 55 years of age or over, you are likely to be eligible for traditional equity release products.

For those above 70

For those above 70, downsizing and moving to a new location and into a new property they are not familiar with may be daunting. Therefore, downsizing might be an inappropriate option. If they do not have a mortgage or have only a very small one, equity release could be advantageous. A lifetime mortgage might be suitable. The cash provided could be used to finance private healthcare or a holiday, for example. A home reversion plan could also allow for a more comfortable life whilst continuing to live in the familiar home.

If moving to a new location and property is feasible, however, selling one’s property at fair market value, downsizing and investing the remaining proceeds in a safe income producing deposit could be a better alternative to a relatively more expensive lifetime mortgage or home reversion plan.

For those above 55 but below 70

For those above 55 but below 70, downsizing is worth considering. However, a lifetime mortgage may still make sense for some if they choose to take regular payments over a period of years instead of an upfront lump sum and this additional income helps improve their everyday life significantly. They would also benefit from a long term appreciation in the value of their property.

Under 55s

Traditional equity release products are not available to those under 55. Sometimes, younger homeowners have no choice but to take out second charge mortgages (with the consent of the first charge lender) to pay for unexpected expenses or repay other debts they have incurred. However, such a course of action could result in a significant negative debt spiral which may be hard to get out of.

Pauzible provides an alternative approach, whereby homeowners receive monthly cash payments for up to five years without incurring additional debt or the relatively high home equity cost of traditional equity release products.

Advantages

You can access Pauzible even if you have an existing mortgage, provided you have at least 30% home equity.

You can receive monthly payments for an agreed period of up to five years.

You do not add to your existing debt burden.

You give away only a small share of your home, typically less than 20%.

You can repurchase that share within 10 years.

You continue to benefit from an increase in the value of your property.

Disadvantages

Pauzible cannot yet provide a large upfront lump sum and is not suitable if that is what you want.

You can buy back Pauzible’s share in the value of your home anytime within 10 years, but, if you do not, Pauzible has the right to sell your property with vacant possession thereafter (albeit you will still benefit from house price appreciation).

References:

1.Equity Release Council Analysis of data from BoE, HM Land Registry and ONS | Released On: Spring 2023

2.Newsletter Q2 2023 Market data | Released On: 15 August 2023 | Equity Release Council

Rising Rates Got You Stuck? Unlock home Equity

Pauzible offers a smart alternative to selling or remortgaging. Access your home's equity safely and securely, even in volatile markets. Regain control and build financial freedom.

A: Equity release is a way to unlock cash from your home.

Q. How does equity release actually work?

A: There are two main types: Lifetime Mortgages provide you with a lump sum or regular payments. The principal and interest are repaid only when you sell your home or die or move into a care home. Under Home Reversion Plans, you sell part or all of your home for a lump sum or regular payments and remain as a tenant until you die or move into a care home.

Q. Am I eligible for an equity release product?

A: You must be at least 55 years old and own your home outright or have a small mortgage remaining. Check with providers. Age requirements and minimum property value may vary depending on the provider.

Q. How much money can I get from equity release?

A: Several factors determine the outcome, including your age, health, property value, desired equity release amount, chosen product and lender. Use online calculators or consult a financial advisor for an estimated range.

Q. Will equity release leave me with nothing to pass on to my family after my death?

A: Not necessarily! You can choose guaranteed inheritance plans. They ensure a certain amount remains for you to will to your beneficiaries. Explore the possibilities with a qualified financial advisor with expertise in the sector. If you select a home reversion plan, you can choose the fraction of your home you sell to the plan provider, so the rest can be set aside for inheritance purposes.

Q. Is equity release a good idea for everyone?

A: It is not a universal solution. Consider the pros and cons carefully. For example, think about potentially increasing debt and reducing what you bequeath. Always seek independent professional financial advice from equity release qualified financial advisors.

Q. What are the hidden costs of lifetime mortgages?

A: Be aware of setup fees, ongoing interest charges and early repayment penalties. Compare different lenders and understand the total cost before making a decision.

Q. Is equity release better than downsizing?

A: It depends! Equity release lets you stay put while accessing cash, but you could leave less to your family due to the cost of accessing that cash. On the other hand, downsizing means less space and frictional costs, including estate agent’s fees, conveyancing costs and stamp duty. But, you could be leaving more to your family. Analyse your needs and consult a qualified, independent financial advisor.

Q. Can I release equity if I already have a mortgage?

A: The devil is in the detail. If your mortgage balance is low compared to your property value, some lenders offer "second charge" equity release plans. Consult a specialist to assess your options.

About the author

Prateek Solapurker

Co-Founder

Previously Illiquid credit trader at HSBC. Also, Co-Head of Credit Products and Hybrids Trading, EMEA, focused on structured credit financing, risk management and structuring at HSBC, and Project Engineer at Unilever

Ready to see what Pauzible could unlock?

Explore how accessing equity from your BTL property could support your business investment plans.

No obligation. Just a clear view of what might be possible.